Index

- Introduction

- Normal form games and Nash equilibrium

- Nash equilibrium with mixed strategies

- Applications to market competition

- Extensive form games and backward induction

- Subgame Perfect equilibrium (SPE)

- Applications to vertical relations and mergers

- Applications to innovation and R&D

- Infinitely repeated games

- Applications to collusion and cartels

Introduction

Game Theory: analyzing strategic interactions between agents where the outcome depends on the decisions of other agents.

The key assumptions is that agents act "rationally", meaning that:

- agents choose actions that they believe is best for them while taking into account information available to them.

- agents anticipate that other agents will also act rationally/strategically.

But what is rationality?

- Rationality does NOT preclude the possibility of mistakes, errors, non-material values, altruistic or social preferences, social norms and cultures.

There are several ways to describe what an economic model is.

- The Standard one: an economic model is a simplied (usually mathematical) description of reality, designed to yield hypotheses about economic behavior that can be tested.

- The Fable one: economic theory formulates thoughts via "models". The word model sounds more scientific that the word fable or tale, but I think we are talking about the same thing. (Rubinstein, 2009)

In Game Theory, the approach lies between these 2 views:

- we will develop and analyze simplified models that are certainly "fictional" (often with unrealistic assumptoins)

- in most cases, predictions are consistent with intuitions under real-world policy and competition law.

Generally speaking, we can say that "all modelrs are wrong, but some are useful".

- all models are abstractions, i.e. intentionally neglet or simplify some aspects

- a model is good if it has the right level of abstraction for a specific goal.

Indeed, unrealistic assumptionsallow a theory to focus only on the crucial and relevant elements required to obtaina prediction.

- some research suggests that over-simplified assumptions (parsimonious economic models) deliver better predictions than black box algorithms _(random forest and kernel regressions) when moving across different contexts.

Oversimplified models are often superior, source: The transfer performance of economic models, 2022.

Normal form games and Nash equilibrium

Each game theory's game requires:

- 2 or more individuals (players, agents)

- players interascting by making choices that jointly determine an outcome

- (usually) every player can affect the outcome but no player has full control of the outocme

A solution is a set of reccomendations about how to play the game, such taht no player will have an incentive to not follow the recomendation.

Let's try to formalize it: Formal Form Games with pure strategies

An -player normal form game consists in:

- for each player , a set of strategies

- for each player , a utility function that, for each strategy profile specify a real number: .

We denote the game by .

A Nash Equilibrium is a strategy profile such that no player has an incentive to unilaterally deviate from their corresponding strategy.

Let be the set of strategy profiles, i.e. .

Given a -player normal form game , a strategy profile is a Nash Equilibrium of if for each player :

- The asterisk is often used to denote an equilibrium profile rather than a generic profile.

- When strategy , it is called "unilateral deviation" from .

An alternative definition of Nash Equilibrium is: a strategy profile ) is NOT a Nash Equilibrium if at least one player has an incentive to unilaterally deviate.

We now consider a -player normal form game and a strategy profile .

Definitin: Best response in pure strategiesThe set of player 's best responses against is the set of player's strategies that solve:

We denote as the set of player 's best responses against .

Theorem: Nash Equilibrium in pure strategiesA strategy profile is a Nash Equilibrium , we have:

In mathematics, we would call this a fixed point.

When we are analyzing the strategic interactions in both theoretical and real-world settings, we are often interested in "efficiency".

- Altought there are many different definition for it, the most standard one is called "Pareto-efficiency".

An outocome is Pareto-efficient if there is an outcome that makes an individual better off without making another individual worse off. In other words:

Definition: Pareto EfficiencyA strategy profile is Pareto inefficient if there is a strategy profile such that:

- all agents are weakly better off: for sall AND

- at least one agent is strictly better off: .

An outcome that is not pareto inefficient is Pareto efficient.

Nash equilibrium with mixed strategies

So far, we assumed that players only choose "pure" strategies (non-random or deterministic). But, more generally, we could consider mixed (random) strategies , to ensure that a Nash Equilibrium exists for a broder class of games.

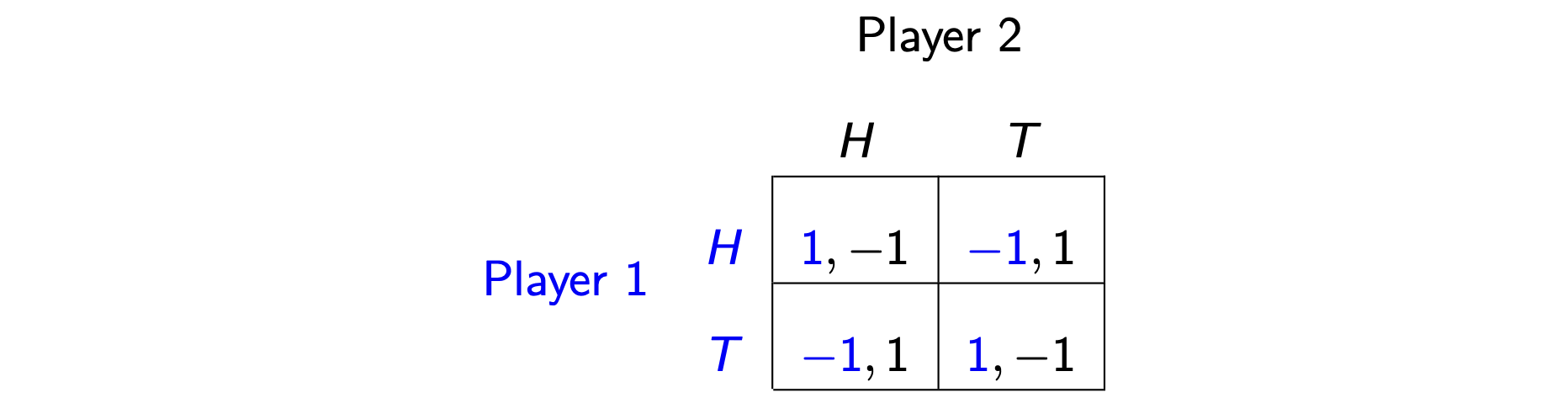

Consider for example the following example. Two players can choose between , and obtain the respect payoff.

It can be shown that there's no Nash Equilibrium with pure strategies.

So let's suppose that player chooses with probability and with probability . The same applies for player : he chosses with probability , with probability .

We want to find such that it is a Nash Equilibrium.

Given that player chooses with probabilkty , Player's payoffs are:

Player stricly prefers if:

We can write Player choices in a more compact way:

Simirarly, given that Player chooses with probability , we can write:

A Nash equilibrium occurs when the strategy profile is such every player is playing a best response to the other player’s strategy.

In other words, we have to find such that:

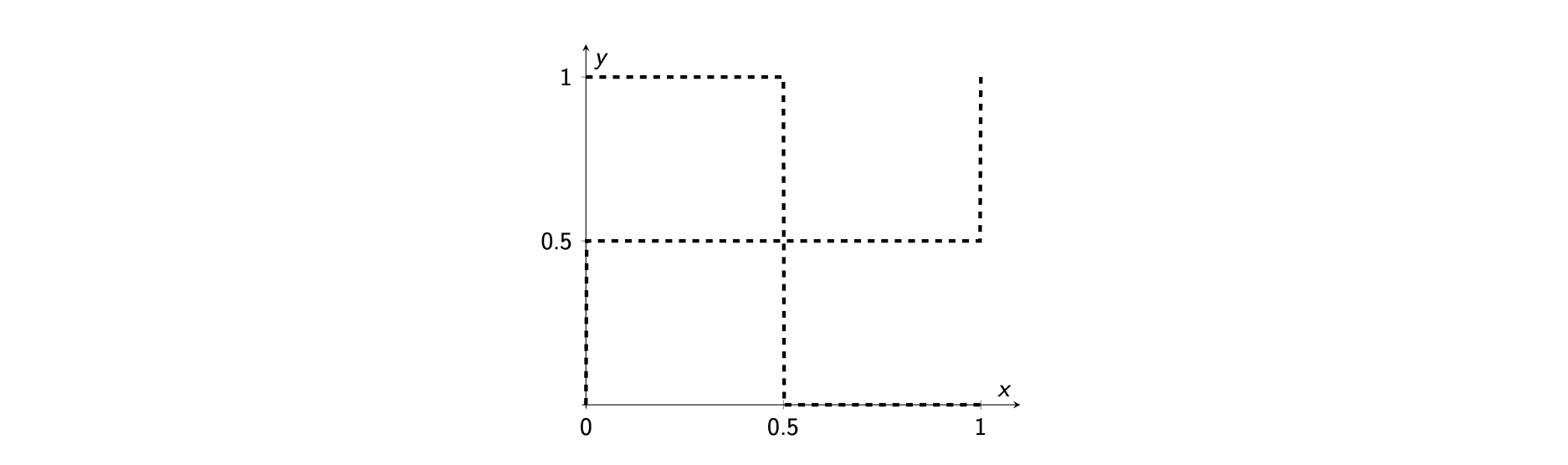

By plotting, we can easily identify them:

The Nash Equilibrium is then .

Mixed Strategies: formal definition

A mixed strategy for a player is a probability distribution over their set of pure strategies.

The set of all the pure strategies is denoted by .

In general, there's NO always a Nash Equilibrium with mixed strategies but, for a broad class of games, there's always a Nash Equilibrium.

This result was proven by John F. Nash, Jr. in his seminal 1950 paper “Equilibrium points in -person games”. Nash was awarded 1994 Nobel Prize in Economics for this and other contributions to game theory.

Theorem (Nash, 1950)

Consider then a -player normal form game , with finite number and finite for every .

The game as at least one Nash equilibrium, possibly involving mixed strategies.

A couple of funny notes:

- The paper is extremley short, just 3 pages!

- There is a book and film about Nash’s life “A Beautiful Mind”

Important result #1: When checking for profitable unilaterally decisions, it is necessary and sufficient to look only at pure strategy decisions , i.e. is a Nash Equilibrium only if:

for every pure strategy .

Important result #2: Suppose is Nash Equilibrium. If players other than play according to , then player is indifferent between any two pure strategies that they play with strictly positive probability in .

Best response: formal definition

The set of player 's best responses against is the set of strategies that solve:

We denote by the set of best responses against .

Theorem (N.E. characterization via best responses)A strategy profile is a Nash Equilibrium if and only if, , we have:

Intuition:

- when looking for Nash Equilibrium:

- we calculate the player's best response functions

- find the intersection(s) of all players' best response functions

- translate the response functions into strategies.

Formal definition: strictly dominated strategies

Given a game , the mixed strategy is strictly dominated by if, for every pure strategy profile of the other players, we have:

If a player has a stricly dominated strategy, he will never use it in a Nash Equilibrium.

Theorem: (Iterated deletion of strictly dominated strategies)Let G be an -player normal form game such that player has a strictly dominated strategy in . Let be the -player normal form game that is obtained from by removing such a strictly dominated pure strategy.

Then and have the same set of Nash equilibria.

Formal definition: weakly dominated strategiesInstead of writing the full strategy profile of the other players as , it is convenient to write as .

Given a game , the mixed strategy is weakly dominated by if, for every pure strategy profile of the other players , we have:

and there exists at least one pure strategy profile such that:

Applications to market competition

We now spend some time to analyze two models of duopoly market competitions:

- Cournout competition: firms compete by choosing to supplky different quantities of the same good

- Betrand competition: firms compete by choosing to set different prices

A funny example of Bertrand competition: In a Manhattan Pizza War, price of slice keeps dropping (NY Times - 2012).

Cournot Model of Duopoly Competition

We start with the following assumptions:

- there are two firms competing in a duopolistic market

- the firms produce an identical good and choose quantities to produce

- producing units of the good costs and the same applies for 0 < c < 1$.

- the market clearing per-unit price when is defined by the total amount of goods:

We can now model the game:

- strategy ser for firm : any number , i.e

- strategy ser for firm : any number , i.e

The corresponding payoff are:

Definition: Nash Equilibrium for Cournot ModelA strategy profile iff$:

To find the Nash Equilibrium, we start looking at best responses: we fix firm's 2 strategy at some and then we model the best response for firm 1.

Indeed, firm 1 chooses that maximizes:

We proceed with First Order Condition (FOC) since we are maximizing a concave-down quadratic function:

we now remember that , so is feasible if . In this case, firm 1's best response is:

If we use the same steps, we can also show that firm's 2 best response function is:

Intuition: the firms are identical:

- they share the same marginal cost and profit function

- if any of the above were NOT the same, then we should suspect that the best response fuctions will be different!

To find the Nash Equilibrium, we look at the intersection of the best response functions.

We assume and , then we equal:

Note that the assumptions remain both valid at this solution!

The equilibrium total quantity is then:

The equilibrium price is then:

The equilbrium profits, given are:

The Nash Equilibrium is inefficient from firm's perspective:

Both firms can do strictly better by colluding to act together as one profit-maximizing firm and splitting the total profits but:

- as the model stands, doing so it NOT an equilibrium

- fundamentally, it's a similar game to the Prisoner's dilemma!

To see this, suppose the firms cooperate and choose to supply a lower quantity: .

This would lead to:

Note that correspons to what a monopolist would do, therefore corresponds to splitting the optimal monopoly quantity equally.

We now analyze why does collusion allow the firmst to do strictly better.

If firm 1 is the merged monopolist (i.e. obtains the profit from both ), they solve:

The derivative with respect to leads to three effects:

The optimal solution is obtained setting the previous to . Increasing has 3 effects:

- sales effect: move revnue from selling more

- price effect: more means lower price

- cost of production equal to

In, on the other hand, firm 1 is not merged, they solve:

Increasing has the same 3 effects but the (negative) price effect is smaller in magnitude:

- increasing reduces the price for both sales

- _unlike the monopoly case, firm 1 doesn't care about sales!

- firm's 1 doesn't internalize the price externality on firm 2

$$\impliesq_1$ relative to a monopoly benchmmark.

Important result from this model:

- Monopoly markets lead to a lower quantity and higher prices than a duopoly ( bad for consumers!)

- duopolist have incentives to collude and act like a monopoly!

- however, collusion is hard to sustain!

- firms might also seek to formally combine their companies in a merger

For these reasons, policymakers are often concerned about monopoly markets. In practise however, mergers are NOT always rejected since there could be some efficiency fains from merging than benefit consumers even if a monopoly forms.

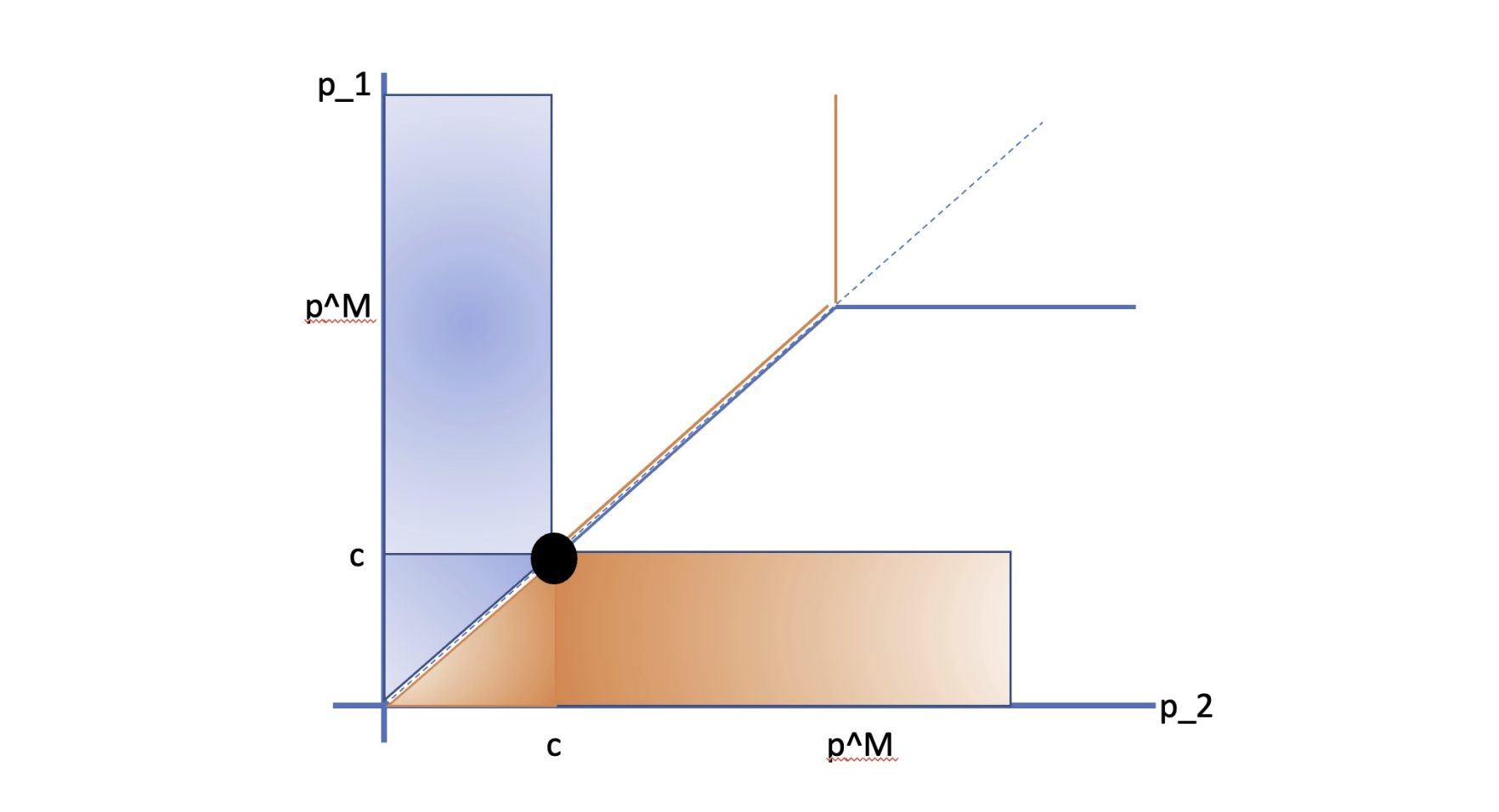

Policy ImplicationsWe now try to incorporate efficiency gains into our model, indeed we modify the m,odel so that after a merger the marginal cost decreases to , with .

At this point, there's a minimum level of efficiency gain so that the monopoly price is lower than the monopoly price:

Variations of the Cournot Models

- The model can be generalized with more than firms. In this case, we see that competition is good for consumers and that equilibrium price is decreasing in and in the limit, as , we get a "perfectly competitive market" where the marginal cost equals the price.

- We can consider a market with two goods are complements and we can arrive at a different conclusion: merging 2 firms can be better for both firms and consumers.

- We can extend the analysis in a multi-stage interagion, showing that it is possible to sustain collusive relationships between firms.

Bertrand Model of Duopoly Competition

In this model firmst compete by setting prices, i.e. each firm chooses a price , for .

Products are identical and hence conusmers always buy from the cheapest firm. The demand functions are then:

Each firm wants to maximize profits:

where is the marginal cost, .

Nash Equilibrium of Bertrand ModelA strategy profile is Nash equilibrium if:

As before, we find the Nash Equilibrium by looking at the best responses.

We fix firm's 2 strategy and we look at firm's 1 best response that maximizes:

In this case, the objective function we want to maximize is not continuous or differentiable anywhere and we cannot apply FOC:

Let's then proceed with some intuition. What would happen if we had the monopoly problem and firm 2 does not exist?

In this case, the firm's 1 problem rewrites as:

The objective function is concave-down quandatric, so we can apply FOC as:

We then know that, in absence of competition, firm 1 would like to choose like in the monopolist scenario.

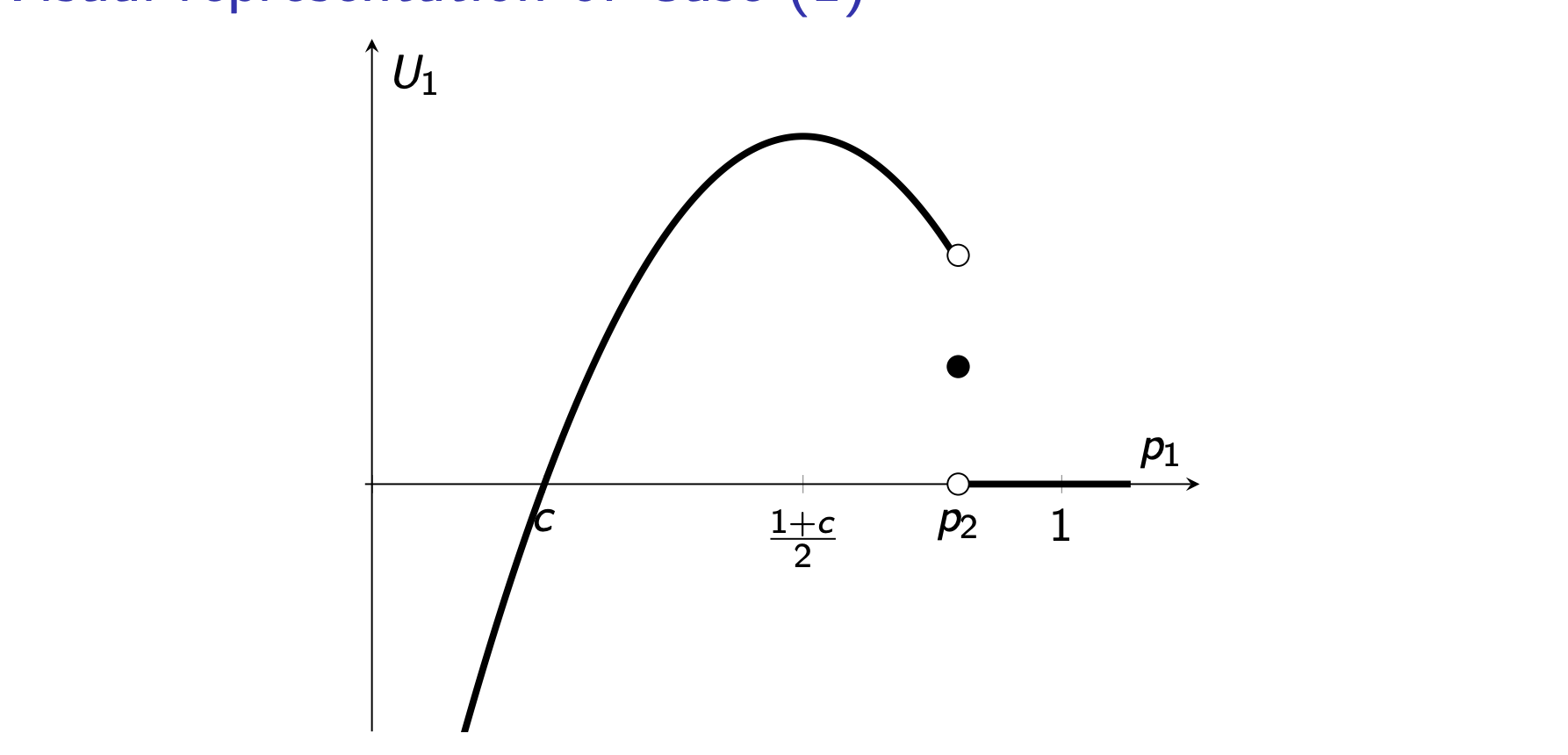

We now analyze 3 different sets of values and firm's 1 best response.

- Suppose : in this case, firm's 1 best response would still be: because we would still have and firm 1 obtains the best-case monopoly outcome.

Mathematically, we have:

- Suppose : for firm 1, choosing ensures and so the firms gets the whole market, but it also obtains no profit since the price equals the marginal cost:

On the other hand, suppose that firm 1 "undercuts" firm's2 price by a tiny amount , in this case we would have:

that, for , is slighly less but close to and, because , we get .

This is better than and , so it is firm's 1 best response:

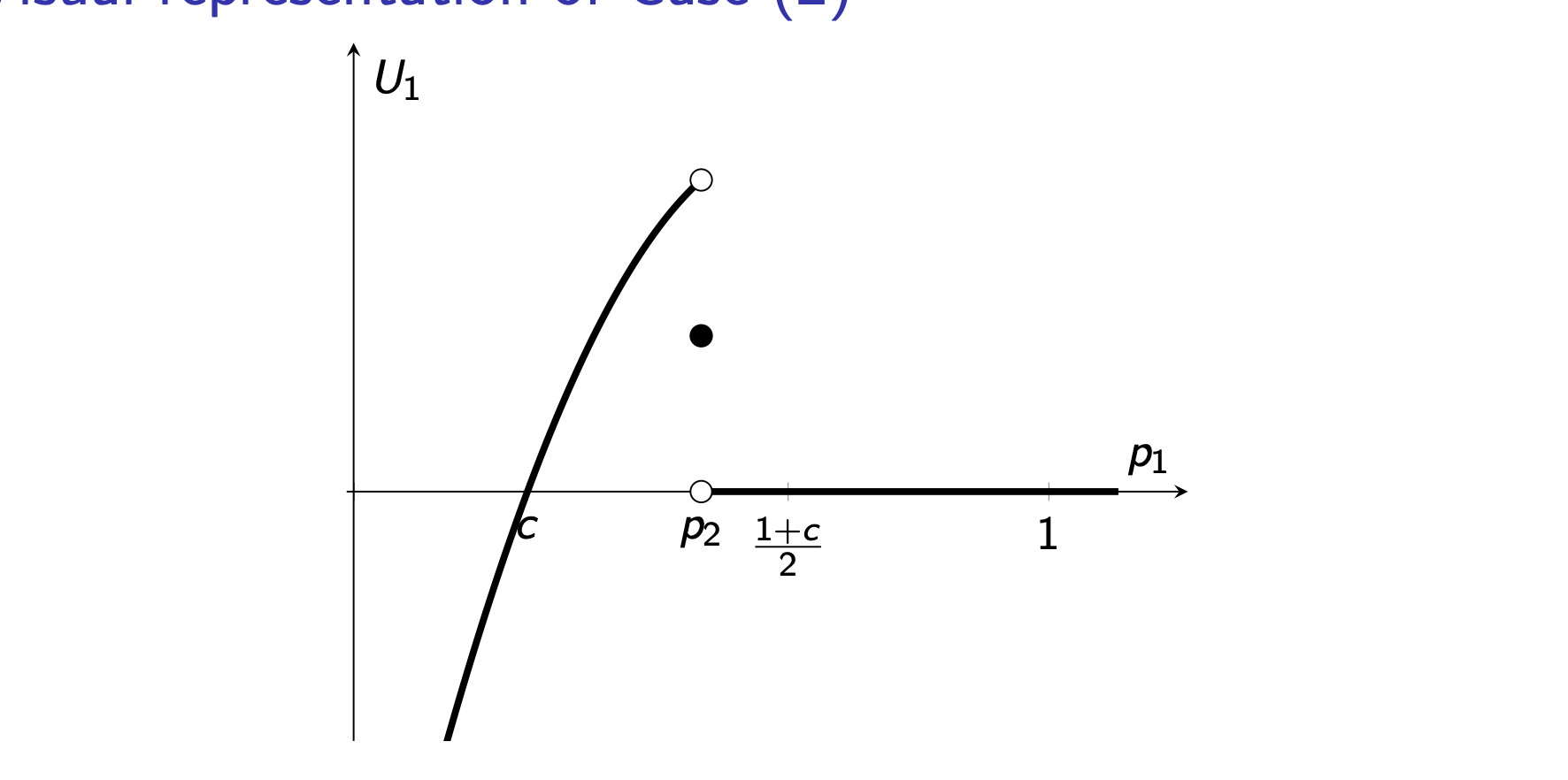

- Suppose . In this case, firm 1 cannot undercut by a tiny amount because profits would be negative, so the firm can do better by not entering the market.

If , firm 1 is indifferent between and .

So, if we want to summarize firm 1's best responses, we get:

where are very small.

The Nash Equilibrium is and lies at the intersection:

Equilibrium outcomes:

- rach firm chooses price equal to marginal cost and sells units

- firms earn zero profits

- equilibrium output equals

Bertrand Paradox

With just 2 firms, we can have a "perfectly competitive" market outcome where price equals marginal cost. Increasing competition beyod 2 firms has NO effects on outcomes, differing drammatically from the Cournot Model.

The paradox can be solved adding more realism to the model:

- relax implicit assuptions (add capacity constraints or a integer-pricing)

- one of the firms may be more productive

- product differentiation or geographic differentiation

- dynamic competition or imperfect information

Extensive form games and backward induction

In simple terms, in a extensive form game players choose actions sequentially, observe each other's actions and know each other's payoffs. In this way, we can model more realistic scenarios: market comptition, political competition, countries responding to conflict since it can be misleading to study sequential interacions using a simultaneous move.

Extensive-form games with perfect informationAn extensive-form game can be represented with a game tree

- The open circle is the initial node (where the game begins)

- Black circles and open circles are decision nodes - are choices (actions)

- are the players

- we specify the payoff vector at eat final, terminal node.

In thi scenario, we can distinguish between 3 different concepts of strategies:

- Pure strategies: a complete contingency plan of action (for every possible sequence of events, an action needs to be specified regardless of the sequence)

- Mixed strategies: a probability distribution function over a player's pure strategies

- Behavioral strategies: at each decision node, a probability distribution over their possible actions must be specified.

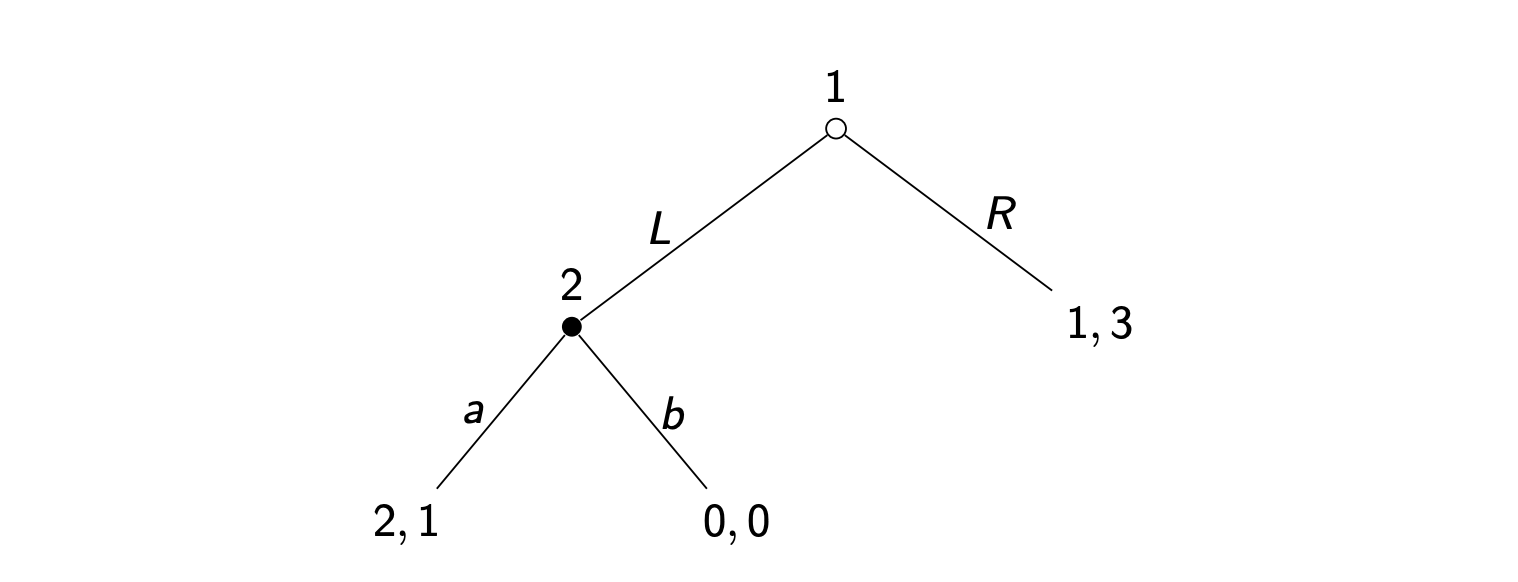

For example, in the three below, the set of behavioral strategies is:

where .

Given an extensive form game, using pure strategies, we can write down the normal-form representation.

The Nash Equilibrium of an extensive form game is the Nash Equilbrium of its normal form representation.

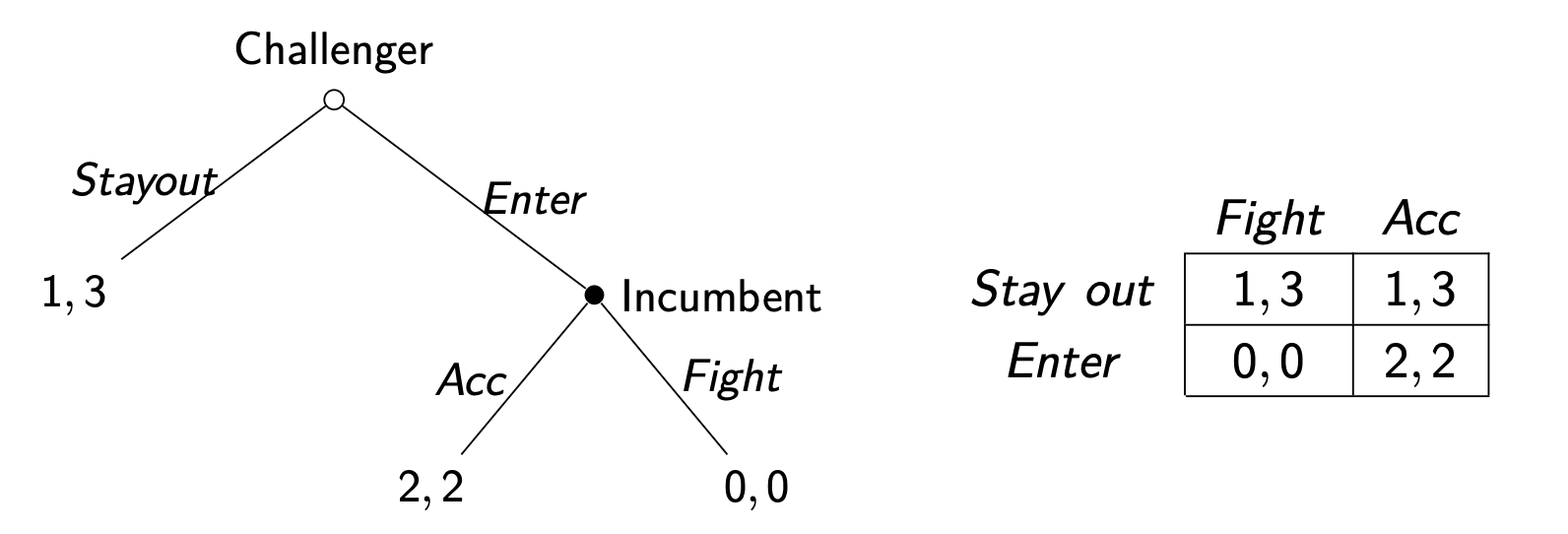

However, Nash Equilibria of extensive form games can be "unreasonable" and rely on non-credible threats.

For this issue, a simple method to find N.E. that avoids this issue is called Backwards induction.

Backward Induction

The Backward induction algorithm is composed by three main steps:

- start by determining the optimal actions at the final optimal node

- Proceed to the next to last decision node and determine actions by players who correctly anticipate optimal actions in the final node

- Repeat until you reach the initial node.

Generally speaking, with backward induction we end up with the following results:

- it can always be applied to extensive-form games so far

- it produces (at least one) strategy profile

- any strategy profile obtained with it is a N.E. (it will also be a "Subgame Perfect Equilibrium, coming soon).

Note that, in some cases the strategy profile found with the backward induction includes actions that never actually occur (because the othe player choose the opposide branch). Nonetheless, we MUST specify these actions to correctly define a strategy profile.

In real life, even people try to anticipate their opponents, they rarely backward induct:

- individuals in the lab typicall fail to backward induct

- many possible explanations: lack of ratinality, altruistic preferences or social preferences aren't captured by the model.

However, deviations from theoretical predictions are rarer when:

- individuals are experienced and sophisticated

- when indvidiauls interact with others who they expect to be sophisticated

In general, the main assumption for the backward induction is that everyone is rartional, everyone know that everyone is rational, everyone knows that everyone knows that everyone is rational and so on.

A new model of market competition: the Stackelberg model for duopoly

Main intuition of this model: in major industries there's always a "market leader".

We consider then 2 firms producing exactly the same good (perfect subsitutes) competing by choosing how much to produce.

Firm choose their quantities sequentially:

- Firm (Leader) chooses

- Firm (Follower) observes and then chooses .

We model the price with the inverse demand function:

The unit cost of production for both firms is costant and equal to , with .

Therefore each firm has payoff given by:

We now solve the model with backward induction looking for a strategy profile such that at every decision node each player chooses an optimal action.

Recall that this strategy prpfile will also be a N.E. that avoidds the credibility issue.

Suppose that firm chose .

Firm observes this and wants to choose to maximize his profits:

The FOC gives:

Since we need , we also need , so we end up with:

q_2^*(q_1) = \begin{cases} \frac{1}{2}(1-c-q_1) \quad \text{if}q_1 \le 1 - c\\ 0 \quad \quad \text{otherwise} end{cases}We now go back at the first stage of the game. Firm chooses to maximize his payoff. However, firm will know what firm will do for every choice of .

So firm wants to choose to maximize .

- Case : if Firm chooses , then and we have:

but this is negative if and thus cannot be optimal.

- Case : if firm chooses such that , then and so firm can maximize:

In this case, FOC gives:

Therefore, anticipating firm 1$ optimal choise is:

Thus, the equilibrium outocme is:

The equilibrium price is then:

In this game, who is better off?

- Firm (Leader) payoff:

- Firm (Follower) payoff:

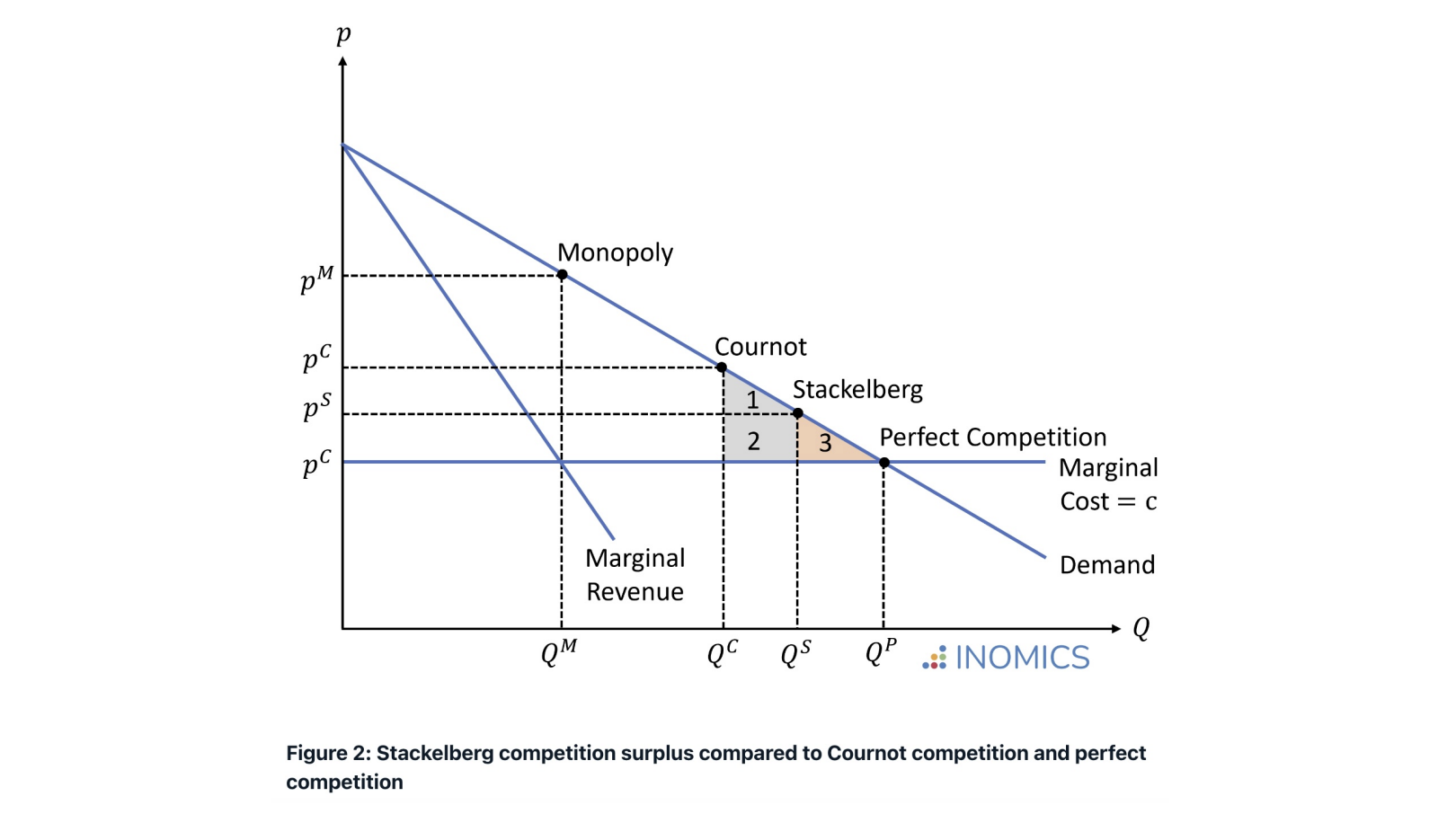

Comparing models of competition

If we compare Stackelberg and Cournot competition, we can clearly see that:

- The Market leader in Stackelberg competition does better that they would do in Cournot model (the opposite applies for the follower).

- Equilibrium price is higher in Cournot thatin Stackelberg:

Intuition: leaders always must do better in Stackelberg competition, otherwise they could choose not to anticipate and choose the Cournot output.

Mechanism that underlines this result is called Commitment Power:

- once the leader chooses an output, it is fixed and cannot be re-adjusted in the current period... even if the leader would like to, which is the case in Stackelberg competition.

- paradoxicaly, if the leader had more flexibility to re-adjust output, this would hurt them (the follower would anticipate it and produce higher output reducing the leader's firm profits).

- It can be surprising that equilibrium price is lower (better for consumers) with Stackelberg competition compared to Cournot.

- This is common in markets with a large firm and a small firm (with respect to quantities produced).

In general, we should think markets as Stackelberg:

- there are often market leaders with products and pricing decisions

- markets may have firms enter in sequence because some entrants become aware of opportunities

Note that Stackelberg model can be seen as a sequential version of Cournot. In contrast, Sequential Bertrnand leads to an identical equilibrium outocome to the standard simultaneous-move Bertrand model with and zero profits.