- Introduction

- Options and financial strategies

- Option valuation

- Pricing by arbitrage

- An introduction to the economic analysis of asset markets

- Choice under uncertainty

- Demand for risk

- Risk sharing and insurance

- Mean variance analysis

- CAPM

- Risk sharing and asset prices in a market equilibrium

Suggested readings:

- Investments, Z. Bodie, A. Kane and A. Marcus, Fifth Edition, Parts IV and VI, for lectures 1 and 2 (later editions areavailable).

- Finance and the Economics of Uncertainty by G. Demange and G. Laroque, for the rest of the course.

0.1 Introduction - The Fama-Schiller controversy

In 2013, Eugene Fama, Bob Shiller and Lars Hansen jointly received the Novel Prize in economics for their economic analysis of asset prices but, ironically, Fama and Shiller represent a interesting and controversial case for the subject.

Eugene Fama is most often considered as the father of the Efficient Market Hypotesis (EFH) which supports the Capital Asset Pricing Model (CAPM), which states that stock's returns over time should be commensurate with its riskiness in relation to the overall market.

In formulas: :

Where is the risk-free rate, (Beta) the sensitivity of the asset to market, the risk-premium (the extra return investors demand for picking risky assets over the risk-free).

Moreover, Fama argued that any test of EMH is actually testing two things at once:

- That the market is efficient.

- That the model is a correct way to measure risk.

Bob Shiller, on the other hand, published in 1981 the paper Do stock prices move too much to be justified by subsequent changed in dividends? that, answering Yes! to the question, claims that the EMH was one of the remarkable errors in the history of economics.

Regarding Fama's theories, Shiller opinion was something like...

- I think that maybe he has a cognitive dissonance

- It's like being a Catholic priest and then discovering that God doesn't exist [...], you can't deal with that, you've got to somehow rationalise it.

In particular, Shiller’s empirical result is that stock prices move way more than the dividends.

If a stock price is truly the "discounted value of all future dividends", it should be stable because dividends don't change that much, but Shille showed the opposite using the Cyclically Adjusted Price-to-Earnings(CAPE) ratio.

In the following yeats, empirical data gave credit to Shiller's critic.

But what does the CAPM actually say?

- how the market should price financial assets in function of the risk

- it shows that a complete market (perfect information and full pricing) will lead to a market equilibrium with optimal risk allocation

However, the CAPM relies on very heavy and simplifying assumptions, some are technical and could be relaxed, others are foundamental and not often realistic:

- the complete market assumption:

- it would require infinitely many assets

- it would require complex products (derivatives)

- complexity implies expertise and potential moral hazard

- other assumptions are unrealistic:

- investors can lend and borrown unlimited money under risk free rates

- all assets are divisible and liquid

- all agents have identical beliefs

So, was Fama simply wrong?

- Not really, he didn't give up and he refined the model, abandoning CAPM and replacing it with a multi-factor risk model

- Even Shiller still endorses a loose verion of it.

- For Shiller, asset prices can overshoot in the short term (due to emotion and irrationality), but they show reversion to the mean in the long period.

- Additionally, according to Shiller markets are still the best tools we have for aggregating information.

To sum up, the Fama-Shiller case is typical from a social science and economics: two theories can contradict each other and still retain intellectual value.

"All Models are wrong, but some are usesul" applies perfectly here: Fama gave an excellent structure to think the financial markets and, even if its work is imperfect, it's yet a solid starting point.

0.2 Introduction to finance and investment planning

A financial system is a set of institutions and markets that have the primary purpose of allowing the desynchronization of income and consumptio.

A financial system allows to match different financial needs of different agents in two dimensions:

- Time (borrow and save):

- wish of continuousu consumption vs discrete income stram

- smooth consumption of time/the life-cycle

- Risk (diversify, insure, hedge):

- smooth consumption across state of nature and possible market scenarios.

Asset: something valuable with well-defined property rights (a contract, a good).

Real Asset: something that has an intrinsic value due to its substance and properties.

Financial Asset: something that has NO intrinsitic material value but which can be traded.

_(Note that the distinction between financial and non-financial asset is not binary and well defined: for example, is gold a financial or physical/real asset?)

Financial assets can be caterogized as follows:

- Riskless assets: assets whose future values can be known with certainty (a government bond that yields 100 CHF in 5 years, assuming no default)

- Risky assets: assets whose future value may depend on some events _(insurance, stocks, options)_blank

- Derivatives are risky assets whose future values depend on the price of other assets.

A bond is often considered a riskless asset (depending on the issuer).

A zero-coupon (ZC) bond with maturity yields no payment before period and pays in period .

They can vary only in terms of maturity.

Denote by the price of a ZC bond with maturity at time (usually the first subscript is current time, the second the maturity). In absence of arbitrage, we have:

where is the discrete per period forward interest rate between and . By iterationm we have:

In relation to this, we can distinguish:

- Discounting: the process of determining the prevent valiue of a future payment at time :

- Compounding: the process of determining the current value at time (in the future) of a monetary amount invested at

The discrete sport interest rate , for a zerou coupon bond with maturity such that:

Or, in other words, the spot rate is the geometric average of the per period forward rate of interest:

We now consider a bond with price in that yields a series of positive coupon payments until the maturity date, so for , plus the final payment of par vaue in .

Its yield to maturity(YTM) is the unique rate for which the present value of these payments is equal to :

The same analysis can be formulated in continuous time, in this case the instantaneous forward interest rate is:

or, equivalently:

By integration, we get:

This interest rate is called "instantanenous" since it represents the evolution of the bond's price process for a infinitesimally small period of time .

Moreover, in continuous time we can define:

The continuously compounended forward interest rate between , denoted by is defined as:

The continuously compounded spot interest rate for a bond with maturity $$ is:

which is the arithmetic average of the instantaneous forward interest rates between .

The function provides the yield curve.

We now consider risky assets. To evalute an uncertain stream of future payments, we still used an additive process:

where the second formulation is needed if we want risk to be taken into account, and we write , where is the risk-free rate and the risk premium.

1. Options and financial strategies

Derivatives are assets whose values mechanically depend on the values of other financial assets (the underlying).

For example:

- Forward contracts: OBLIGATION to purchase (long position) or sell (short position) the underlying at a specified future price at a specified delivery date.

- Options contracts: RIGHT to purchase or sell a specified amount of the underlying at a specified exercise price at or before a specified expiration date.

Options offer an advantage: the transaction does not have to occur if it not profitable for the owner of the option. This advantage comes at a price:

- Forwards are entered at NO cost

- Options are purchased or sold at positive price that the represents the cost of the right to buy/sell.

- Selling (or writing) an option implies an obligation (if the option is exericed, the seller must sell or buy the stock and incurs a loss) \to the seller receives a compensation.

Derivatives can help shaping the risk exposure:

- Hedging means insuring against market price volatility

- Speculation means expoiting market price volatility

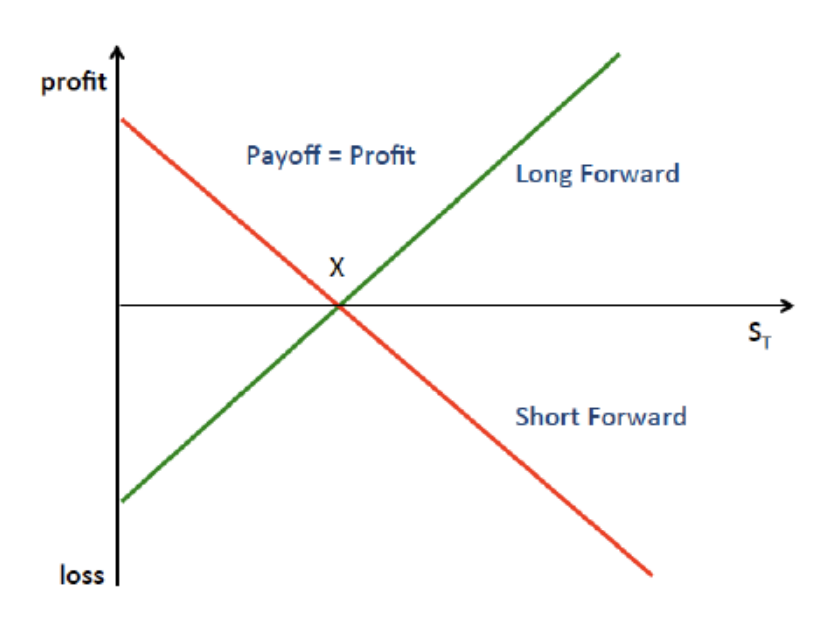

Forward Contract Payoff

- agree delivery price

- spot market prie of the underlying at maturity

Profits at maturity are:

- Payoff long position

- Payoff short position

For this reason, forwards are great for speculation. At a goiven time , an unerlying has a price , with no clear evolution for the future. If a speculator expectes:

- long forward with

- short forward with

On the other hand, forwards are used in hedging to avoid risks.

.

Suppore, for example, that Giacomo's GmbH needs to sell an activity (example: some running shoes) at maturity , with value at given time .

Giacomo faces then a risk management problem: how can he insure against price fluctuations of the running shoes?

Solution: use the forward contract to construct a hedged portfolio that fixes the profits from the furue sale at a desired level :

To fix the profits at , Giacomo can open a short position on the forward contract with delivery price .

(The opposite - long forward contract - applies if you need to buy and you want to avoid risk).

Options Payoff

An options is a right to purchase/sell a certain amount of the underlying at/before future expiration at exercise price (strike) .

Options differ by:

- Position

- Long: option holder (right to exercise)

- Short: option writer (obligation to facilitate the option's exercise)

- Type of right:

- Put: long position has the right to sell an asset for

- Call: long position has the right to purchase an asset for

- Possibility of early exercise:

- American option: exercise at or before expiration

- European option: exercise only at expiration.

Consider now:

- exericse price of an option

- market price of the underlying at expiration

- Premium: purchase price of an option (market value):

- : premium for a call at

- : premium for a put at .

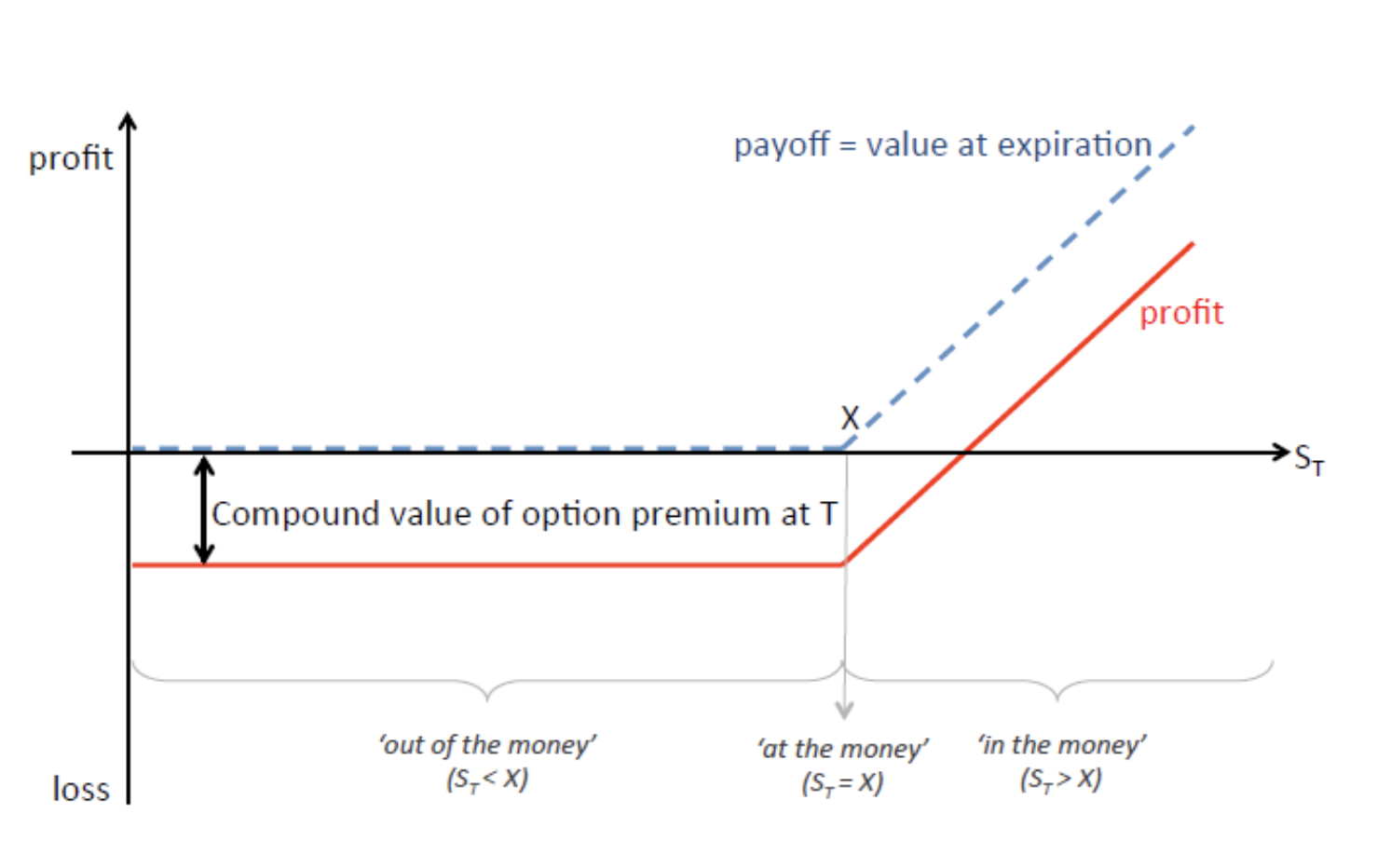

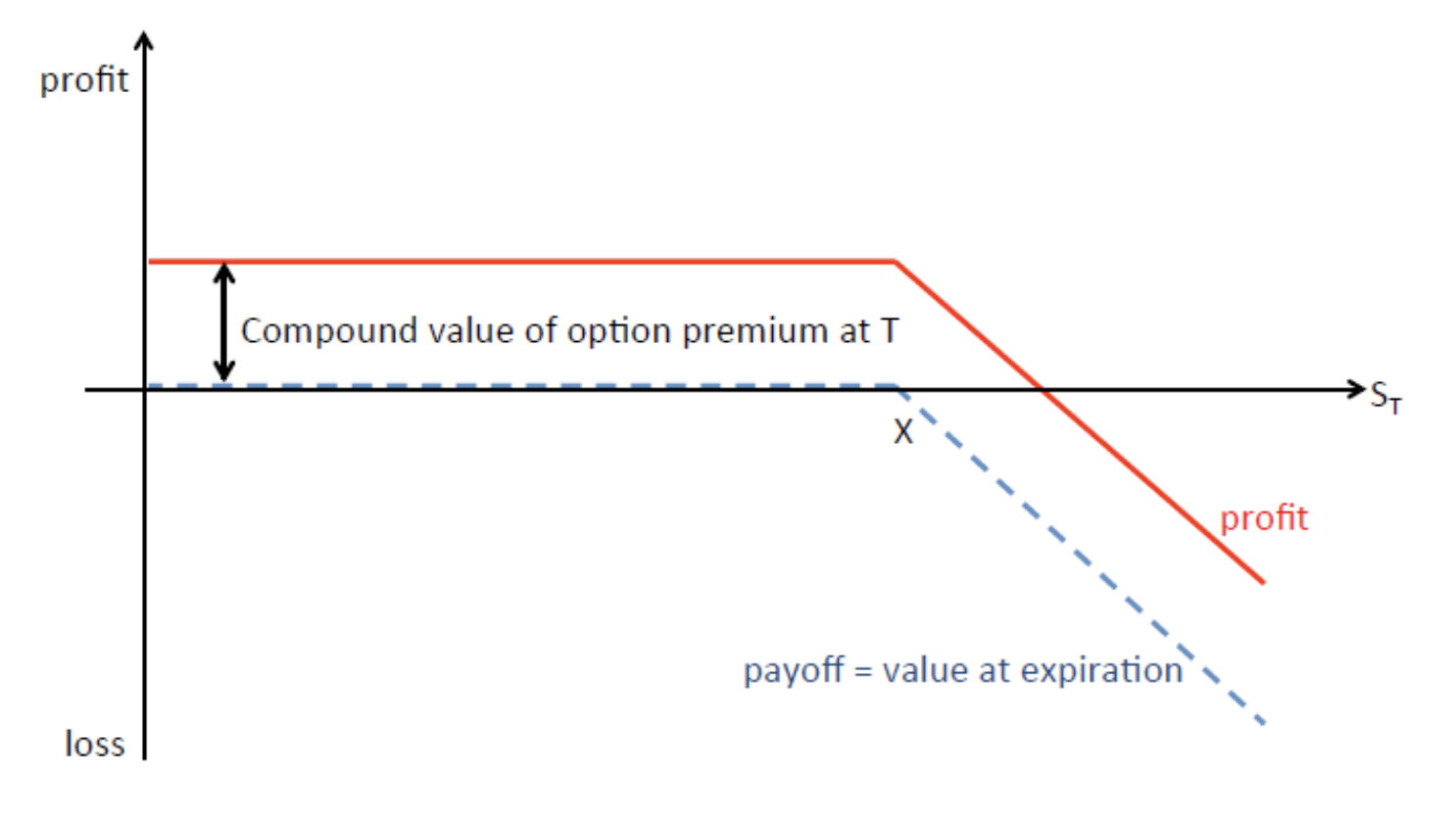

Payoff/value at expiration:

| Condition | Call: Long Position | Call: Short Position | Put: Long Position | Put: Short Position |

|---|---|---|---|---|

| 0 | 0 | |||

| 0 | 0 |

Profits are then given by:

- Long position:

- Short position:

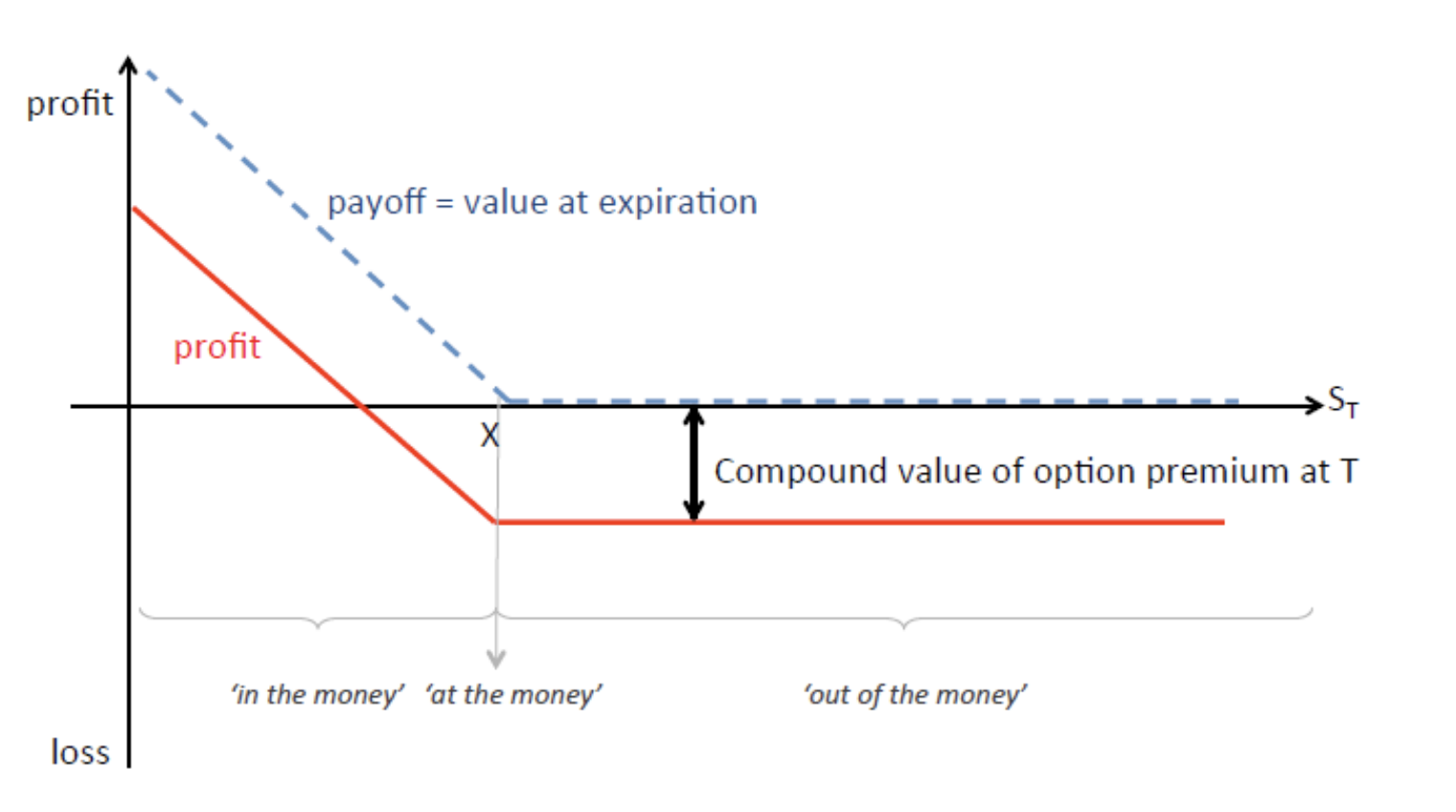

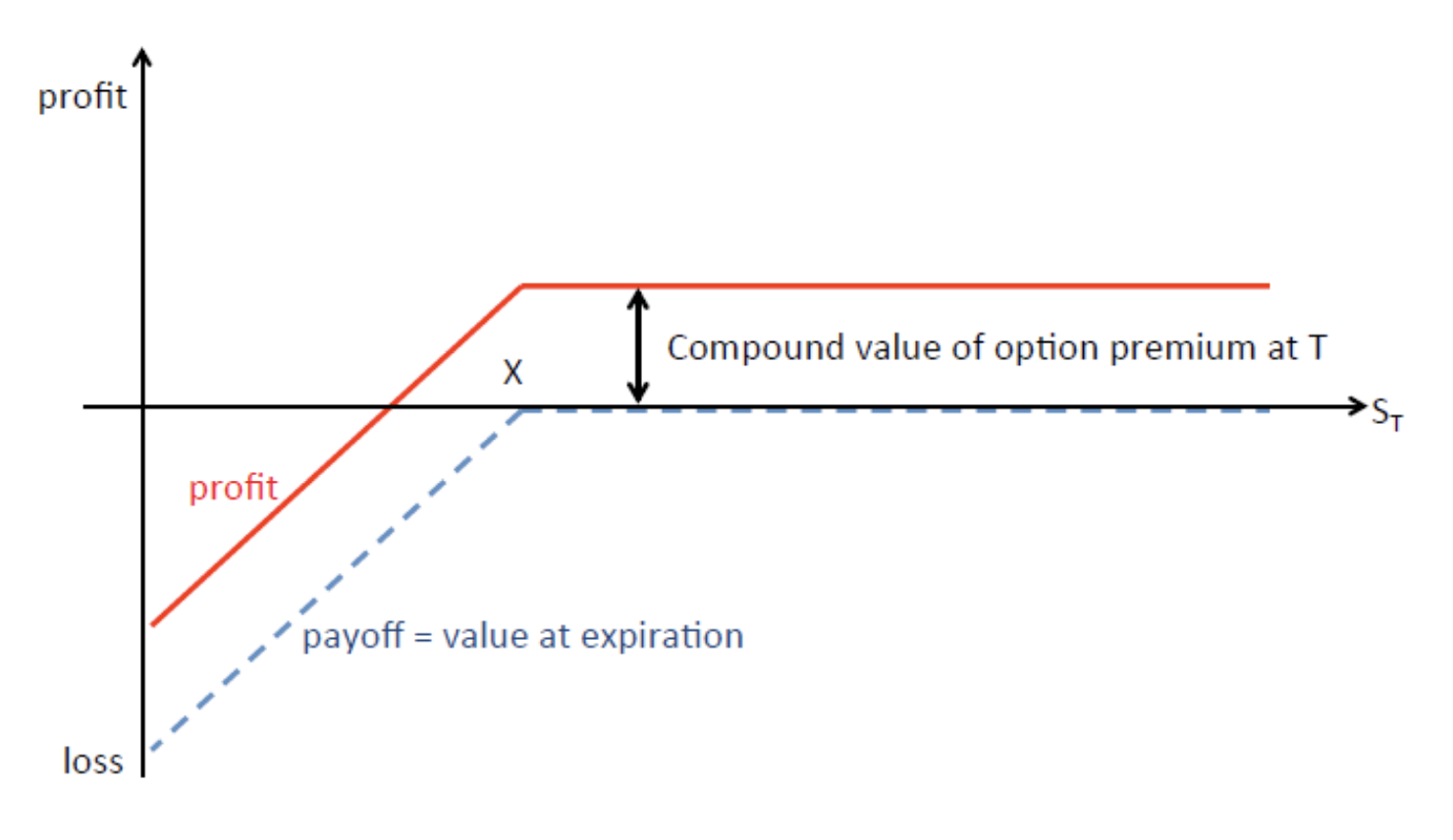

Long Call

Short Call

Long Put

Short Put

Option Strategies

If the agent as an expectaction about the price development of the underlying:

- Bullish strategies: generate a profit when the underlying's price increases

- Bearich strategies: generate a profit when the underlying's price decreases

- Non-directional strategies: generate a profit depending on the underlying's actual volatility.

But... what are the reasons for trading in options rather than trading in the underlying directly?

- Leverage effect: option values respond more tham proportionately to changes in the underlying's value.

- Tailoring risk exposure of investment: optinos can be less risky due to limitation of the downside risk.

- Portfolio insurance: it can be insured by long on a put for that stock.

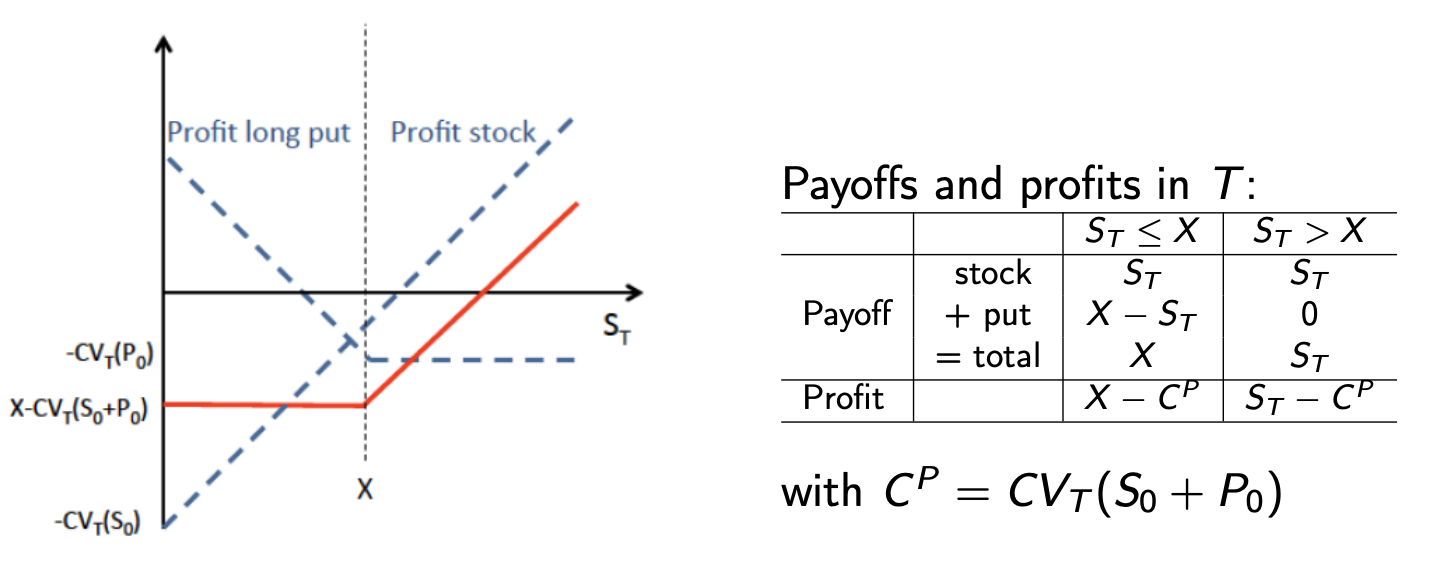

Option strategies: Protective Put

Consider an agent that:

- invest in a stock with price

- wants to insure against potential declines in the stock price

long put on the stock (exercise price in with premium )

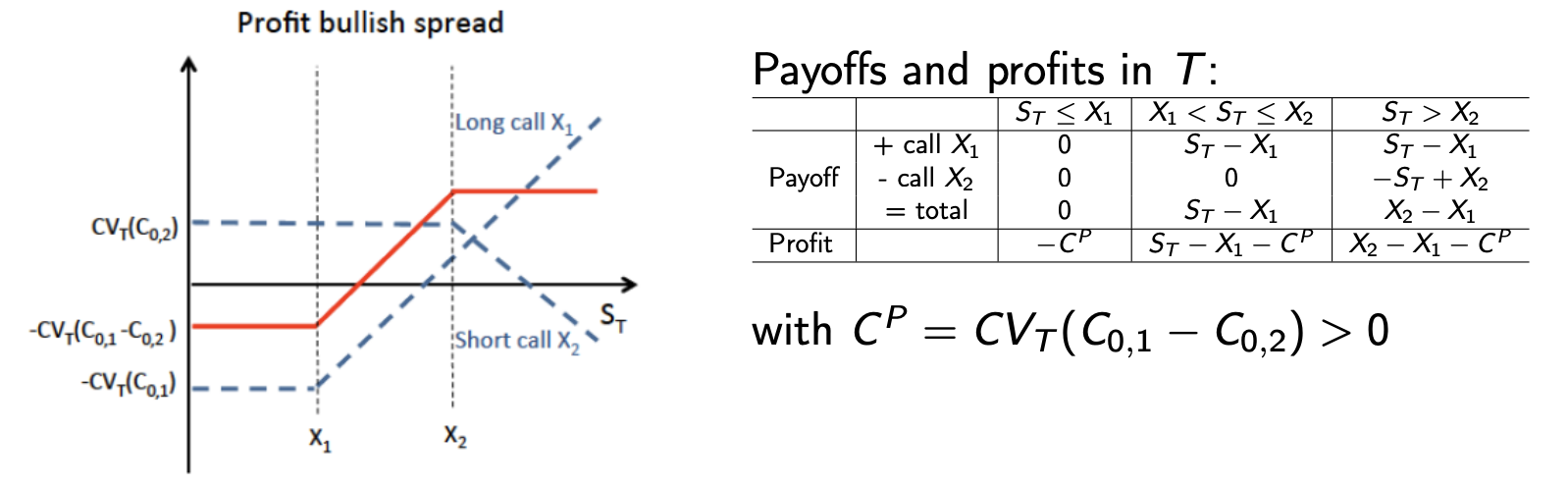

Option strategies: spreads (I)

Consider an agent that wants to take advange of higher future price of the underlying.

He could buy the stock, buy a call or short a put, or as an alternative, construct a portfolio that allows to reduce the risk at the cost of _givin up part of the profits:

This is called Bull spread strategy:

- 1 long call with strike and premium

- 1 short call with strike and premium

Option strategies: Spreads (II)

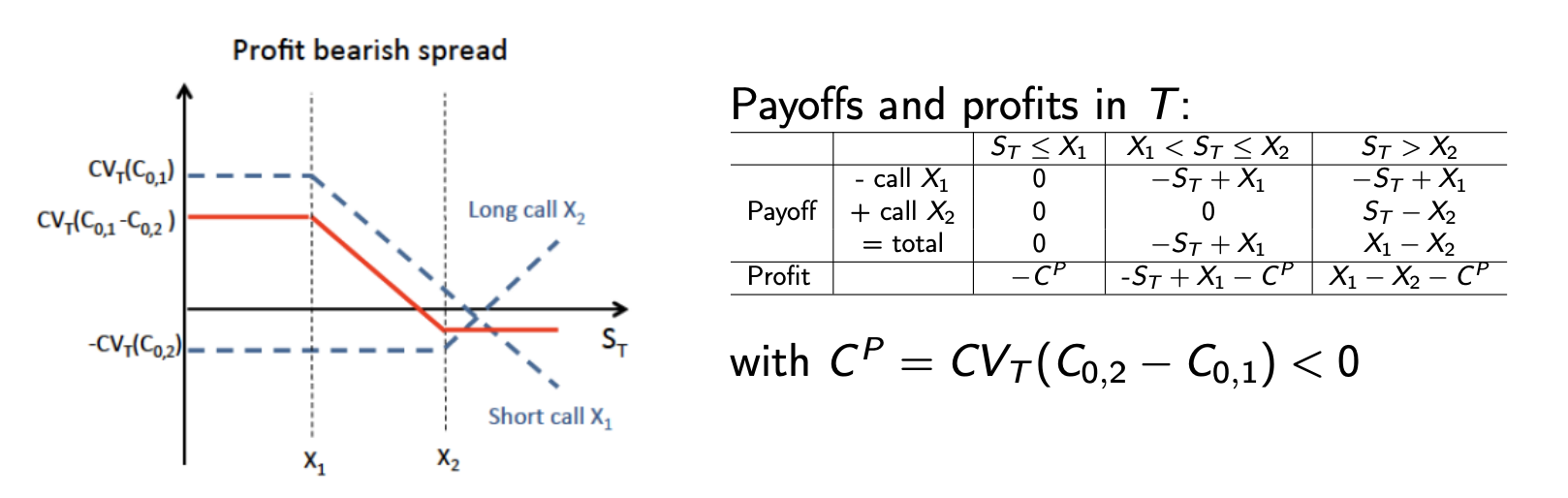

The opposite also applies, i.e. consider an agent that wants to take advantage of lower future price of the underlying.

Bear spread strategy- 1 long short call with strike and premium

- 1 long call with strike and premium

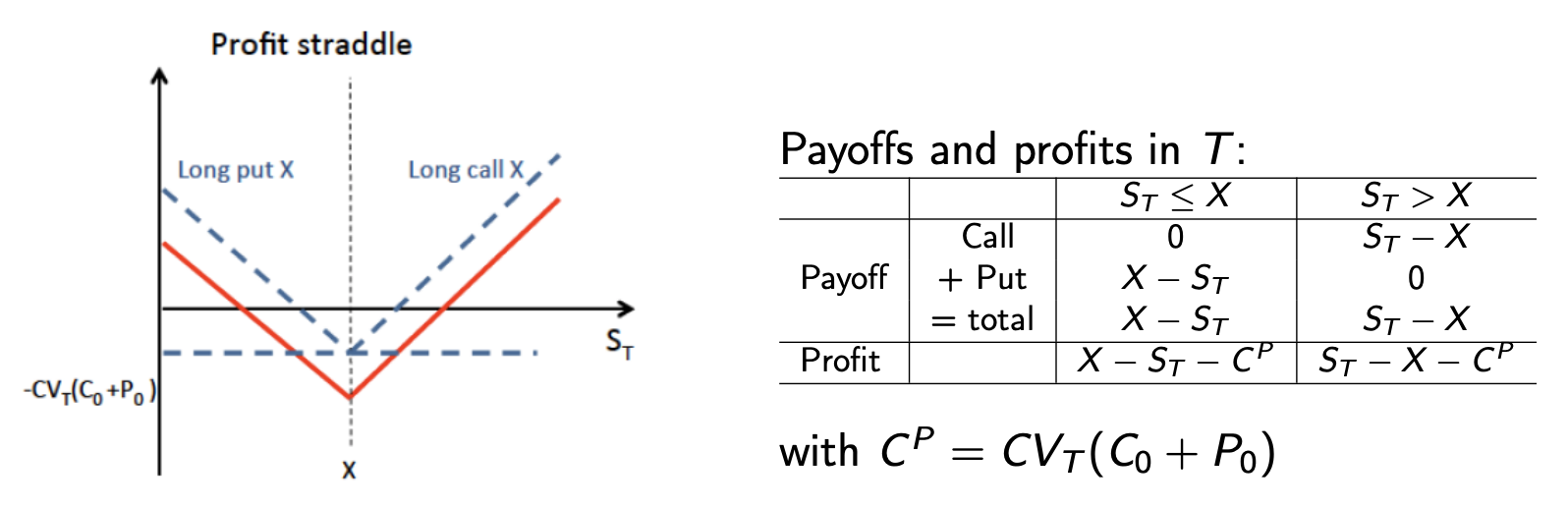

Option strategies: Straddle

Consider an agent that expect large move in the stock's price but he's uncertain about the direction.

Straddle Strategy:

- 1 long call with strike and premium

- 1 long put woth with strike $$ and premium

Moreover, if he thinks:

- the movement will be more likely bullish: buy to 2 calls (strap)

- the movement will be more likely bearish: buy to 2 puts (strap)