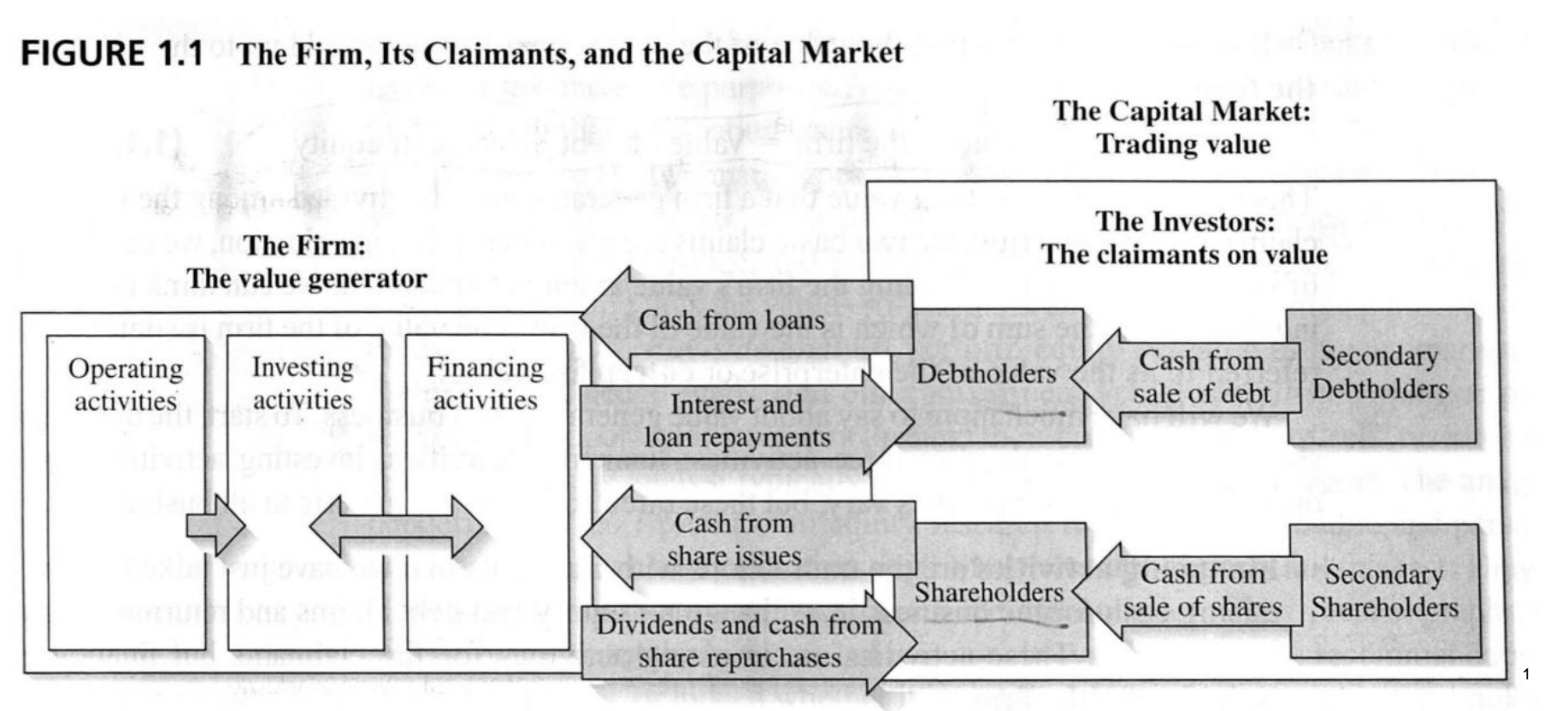

- Introduction

- Agency Problems and Corporate Governance

- Stakeholder Capitalism and Responsible Business

- Credit Risk and the Value of Corporate Debt

- The Many Different Kinds of Debt

- Leasing

- Managing Risk, Options

- International Financial Management

- Financial Analysis

- Financial Planning, Working Capital Management

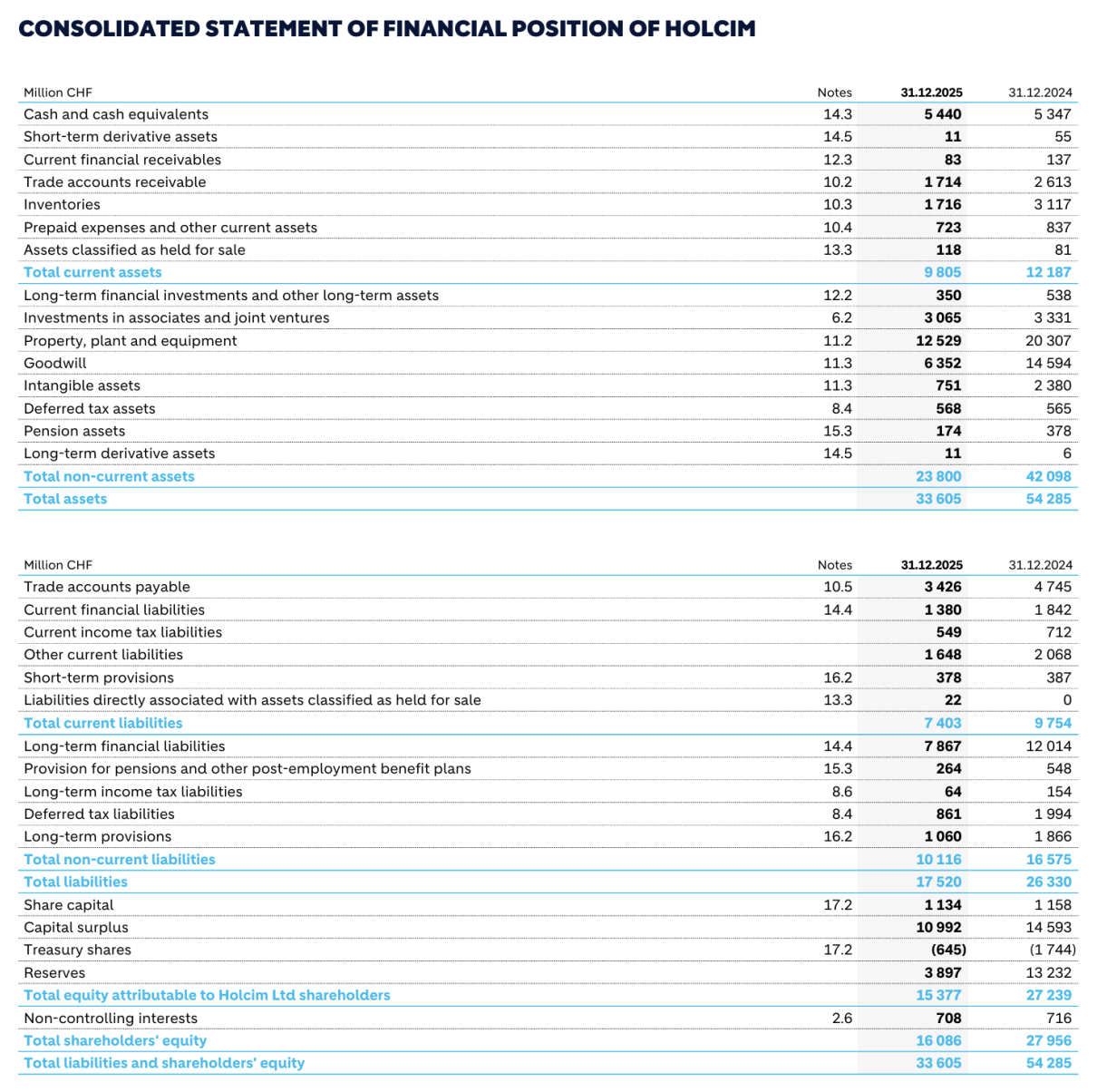

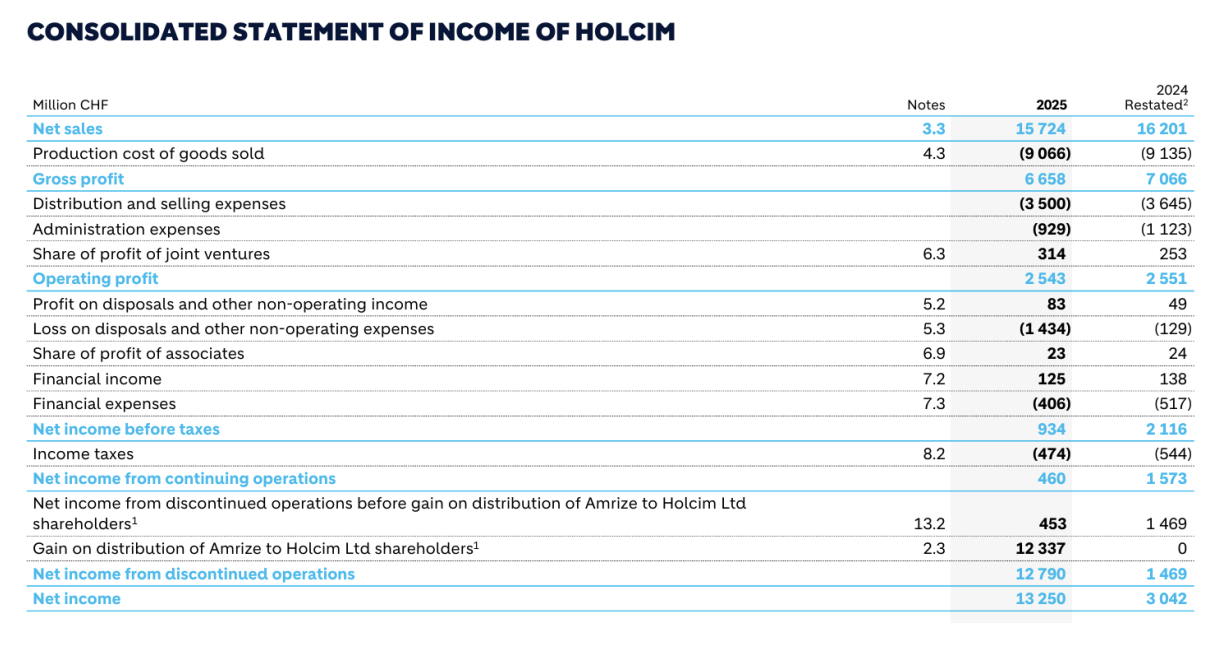

- Treasury at Holcim / Amrize Case

- Mergers

- Corporate Restructuring

- Financial Crises and Regulatory

- Debt Restructuring

Introduction

“Every decision made in a business has financial implications, and any decision that involves the use of money is a corporate financial decision. Defined broadly, everything that a business does fits under the rubric of corporate finance. It is, in fact, unfortunate that we even call the subject corporate finance, because it suggests to many observers a focus on how large corporations make financial decisions and seems to exclude small and private businesses from its purview. A more appropriate title for this discipline would be Business Finance, because the basic principles remain the same, whether one looks at large, publicly traded firms or small, privately run businesses. All businesses have to invest their resources wisely, find the right kind and mix of financing to fund these investments, and return cash to the owners if there are not enough good investments.”

(Damodaran, 2025)

It's worth spending some time on Damodaran's website: a lot of (free) lectures, books and papers!.

First Principles - maximizing the value of a business-

The investment Decision

- the hurdle rate (minimum rate of return a company or investor requires to approve an investment) should reflect the riskiness of the investment

- the return should reflect the magnitude and the timing of the cash flows

-

The Financing Decision

- the optimal mix of debt and equity that maximizes firm's value

- the right kind of debt matches the tenor of the firm's assets

- The Dividend Decision (if the firm cannot find a investment that meets its minimum acceptance rate, return the cash to the owners)

- How much cash you can return depends on the current and potential opportunities

- How you choose to return the cash to the owners will depend on whether they prefer dividends or buybacks

Corporate Finance is not a perfect science!

It applies mathematical models and statistics but interprets and tests them in a real-world economic and behavioral contexts.

Recall that the finance goals of the corporation are, from the stockholders' point of view:

- maximize current wealth

- transform wealth into most desirable time pattern of consumption

- manage risk characteristics of the chosen consumption plan

But... how does cash flow between financial markets and the firm's operations?

Recall that, in presence of such cash-flows, the Net Present Value (NPV) is defined as:

- depends only on the forecasted cash flows and the opportunity cost of capital

1. Agency Problems and Corporate Governance

The agency problem is defined as a conflict of interest inherent in any relationship when one party is expected to act in another's best interests.

In particular, the principal-agent problem is a conflict of interest that occurs when an agent (manager) authorized to act on behalf of a principal (owner) pursues their own self-interests rather than maximizing the principal's goals

Agency costs reduce firm value due to agency problems:

- value lost because managers do not maximize the value of the firm

- costs of monitoring managers and intervening when problems arise.

Principals agency problems come from:

- not put in sufficient efforts

- use cash on perks and private benefits

- over-invest in search of power and prestige

- be reluctant to take risks or take too many risks

- focus on short-term results at the expense of long-term value

In the corporate world, Boards of Directors exist to solve this problem.

In particular, in the US and the UK, boards are composed as follows:

- One single board with outside non-executive directors and inside executive directors (CEO, CFO) to provide the board with necessary expertise and information about the firm.

- The majority of the directors has to be independent according to NYSE and NASDAQ (in practise, around 85% are independent) to ensure that the people monitoring the managers aren't also friends with them or financially dependent on them.

- It should not be too big to generate a free-rider problem (when those who benefit from resources, public goods and common pool resources do not pay for them)

- It should not be too small to be unable to handle the complexities.

- Directors should not serve too many boards.

- Annual elections are done for a share of the board, some directors are not changed yearly.

On the other hand, shareholders can also play a strong role in monitoring the firm with three by:

-

Voting

- Binding versus Advisory votes

- Promoting proxy fight (aggressive move where an activist shareholder tries to replace the current board by persuading other shareholders to use their "proxy" votes and vote on behalf of another.)

- Dual-Class Equity (when some shares, usually held by founders, have more voting power (example: 10x, 100x) of "normal" shares).

- Engagement

- Governance through exit from the company

Auditors monitor the firm ensuring consistency with generally accepted accounting principles (GAAP):

- in case of no problems: document certifying that the financial statements fairly represent the company's financial conditions

- in case of problems:

- Qualified opinion: accounts have not fully acted according to GAAP

- Adverse opinion: accounts violate many GAAP rules.

More on the adverse opinion [Investopedia]

Moreover, lenders usually track company's asset. Takeover involves funding the acquisition of a target company, typically through cash, debt, equity issuance, or a mix of these methods when assets are not being used efficiently.

2. Stakeholder Capitalism and Responsible Business

Stakeholders are individuals, groups, or organizations with a vested interest in, or who are affected by, the actions, decisions, and success of a project, company, or organization

- employees

- customers

- suppliers

- local and regional communities

- the environment

- the government

The Case for Shareholder Capitalism

Milton Friedman in 1970 with his article "The Social Responsibility of Business is to increase its profits" rejected stakeholder capitalism and argued that a company’s only responsibility is to its shareholders:

“.....there is one and only one social responsibility of business—to use its resources and engage in activities designed to increase its profits so long as it stays within the rules of the game, which is to say, engages in open and free competition without deception or fraud.”

Friedman's argument is based on three points:

- maximizing shareholder value requires investing in stakeholders and taking them seriously

- government policies ensure companies will engage in socially responsible behavior

- maximizing shareholder value gives shareholders maximum freedom to support the social objectives they care about.

The discussions of the “social responsibilities of business” are notable for their analytical looseness and lack of rigor. What does it mean to say that “business” has responsibilities? Only people can have responsibilities. A corporation is an artificial person and in this sense may have artificial responsibilities, but “business” as a whole cannot be said to have responsibilities, even in this vague sense. The first step toward clarity in examining the doctrine of the social responsibility of business is to ask precisely what it implies for whom.

(quote from the article)

With that, Friedman also pointed out that it is in the companies' self interest to invest in their local community and proposed that all future cash flows should be included into the NPV calculation, including those arising through stakeholders.

According to this view, since prosperity depends on profits and externalities and externalities are usually addressed by laws and government, the market cannot police itself regarding social harm that is the job of the state.

In other words, the government sets the "rules of the game.", then the company plays to win (maximize profit) within those rules.

By contrast, "Enlightened Shareholder Value" (ESV) is a managerial objective phrase used, for example, in the UK Companies Act 2006. Under ESV directors are required to promote the success of the company for the benefit of its members (shareholders) while considering a list of factors (long-term consequences, employees, suppliers, customers, community, environment, and the company's ability to innovate).

ESV therefore treats stakeholder and sustainability considerations as factors that can affect long-term shareholder value and so deserve attention in management decisions.

Practical implications:

- ESV keeps a clear, shareholder-centred objective (promote the company's success) but recognises that long-run shareholder value can be improved by attending to stakeholder interests and environmental risks.

- Economic tools (NPV, risk-adjusted discounting) are central for investment valuation, but under ESV managers should also incorporate longer horizons, material non-market impacts and risk mitigation benefits that affect expected shareholder returns.

- ESV helps justify some social and environmental investments when they are expected to preserve/increase long-term value

The Case for Stakeholder Capitalism

Violations of Friedman's assumptions may justify stakeholder capitalism:

- Assumption 1: well functioning governments

- government may be influenced by lobbying

- elections are not very frequent

- regulation cannot regulate qualitative issues effectively (negative externalities are not priced!)

- Assumption 2: companies have no comparative advantage in serving society

- companies have comparative advantages in activities they control

- companies have comparative advantages in expertise

- Assumption 3: investing in stakeholders is instrumental and functional to increase profits

- it's impossible to calculate the return of investing in stakeholders

In reality, investing in stakeholders splits the pie in short-term but grows it in the long-term in ways that could not be predicted (uncertainty, NPV calculation,..) and, at the end, both shareholders and stakeholders are better off than before.

The potential advantage of stakeholder capitalism is that it allows managers to pursue stakeholder interest even if doing so can't be justified by an NPV calculation.

However, this causes:

- no clear rule to replace NPV

- accountability to everyone means accountability to no one.

Moreover, there's arbitrariness at least regarding two dimensions:

- weighting: how much shareholders vs stakeholders value

- comparability: how to measure shareholder value (USD) vs stakeholder value (salary, happiness, environment etc...)

Responsible Business

Responsible business lies at the middle between shareholder and stakeholder capitalism.

- It creates value for shareholders by creating value for society (with an explicit duty to shareholders)

- While Corporate Social Responsibility relates to non-core activities (donations, philanthropy), responsible business is about the core activities of a firm.

- Guiding Principle: create value for society and at least don't reduce shareholder value significantly.

- Principle of Multiplication: does an investment in a stakeholder generate a greater benefit?

- Principle of Comparative Advantage: can the company deliver more value through an activity than others?

- Principle of Materiality: are the stakeholders an objective of the company's business?

Generally speaking, some firms tie CEO and management's pay to ESG targets, so the company is more aligned and motivated to hit them. (In 2023, 76% of S&P500 firms linked executive pay to at least one ESG target).

However, the CEO may focus only on the metric and miss the point. Secondly, it's an extrinsic, not intrinsic, motivation: CEOs focus on ESG target because they earn a bonus, rather than care really about the environment.

To ensure that companies are being run responsibly, ESG rating agencies provide an overall assessment of a company's ESG performance, similar to how credit agencies apply a rating on creditworthiness, however:

- ESG ratings are inconsistent. The correlation between ratings of two different agencies are, on average, 0.28-0.71; compare do 0.9 for credit ratings.

- 38% is caused by the use of different attributes

- 56% is due to measurement

- 6% is due to weight: different providers place different importance on individual indexes/components of the rating.

ESG rating disagreement: Implications and aggregation approaches (paper)

3. Credit Risk and the Value of Corporate Debt

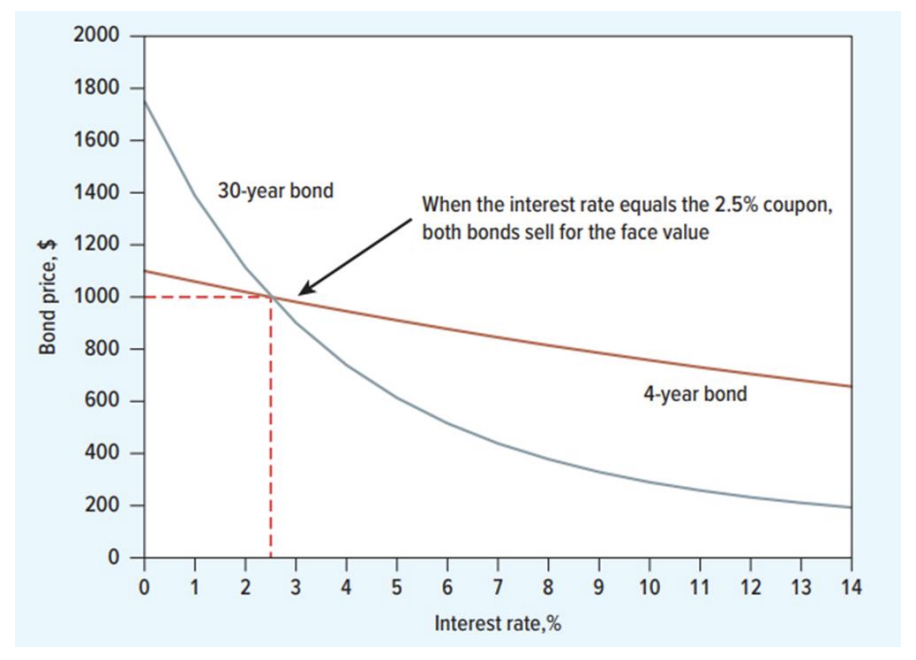

The price of a bond s the present value of all cash flows generated by the bond (coupons and face value at maturity ) discounted at the required rate of return .

Note that the price of long-term bonds is more sensitive to changes in the interest rate than the price of short-term bonds.

However, it is very important to distinguish between promised and expected yields.

Suppose Giacomo GmbH offers a 5% 1-year note, issued at par (), with a risk-free rate .

Consider also that, unfortunately, Giacomo has a chance of default and only pay .

The Present Value of the Note is then:

However, considering the risk of default, we can calculate the expected payoff of the note as:

We then discount the expected payoff to obtain the present value of the bond:

If we consider the face value promised by Giacomo (hence excluding the possibility of default), we obtain the Promised Yield:

Note that, even if the promised yield is so high, the expected yield is always 5%:

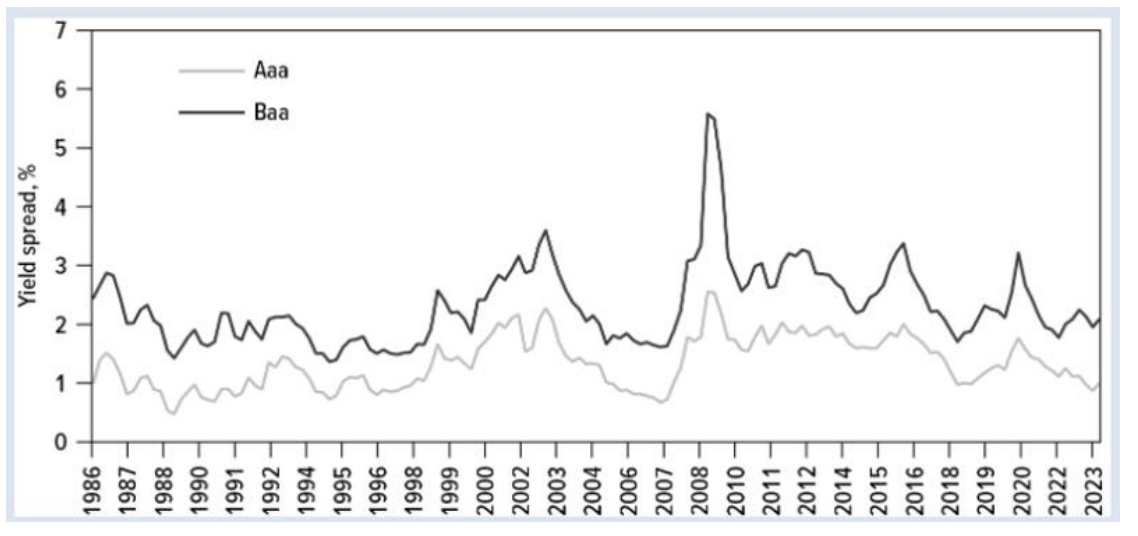

bonds by Moody's are the highest-grade bonds and are issued only by a few blue-chips companies.

Historically, the promised yield on these bonds has been about higher than the yield on 10-Year Treasuries.

On the other hand, bonds are rated three so called notches lower, and the yield is historically higher.

The total return on a bond investment over a specific period, accounting for both the coupons received and the change in the bond's market price.

Yield to Maturity (YTM)YTM is the internal rate of return (IRR) earned by an investor who buys the bond today at the market price and holds it until maturity, assuming that all coupons are reinvested at the same rate.

Macaulay DurationDuration is the weighted average of the times to each of the cash payments. It is the primary tool for estimating a bond's sensitivity to interest rate changes.

Often we use Modified Duration to calculate the actual percentage change in price for a 1% change in yield ():

ConvexityDuration is a linear approximation of the interest rate and the price, convexity takes into account the second order relation, especially important for bigger interest rate changes.

Intuition: A bond with higher convexity drops less when rates rise and gains more when rates fall compared to a bond with lower convexity.

Credit Default Swaps

It is possible to insure corporate bonds with financial instrument called Credit Default Swap (CDS) (Warren Buffet call them "financial weapons of mass destruction")

CDS are financial derivatives acting as an insurance against the risk of a borrower defaulting on debt (bonds). The buyer makes regular premium payments to a seller, who agrees to compensate them if a specific credit event, like bankruptcy or insolvency, occurs.

CDS are traded over-the-counter (OTC) and their premiums are quoted in basis points, reflecting the market’s view on the risk of default.

Note that a buyer does not have to own the underlying (the debt, bonds), he can just buy a CDS simply betting that the borrower’s credit health will decline or that they will default (speculation). In this case, they are called "naked" Credit Default Swaps.

Regarding naked CDS, especially after 2008-crisis, CDS are heavily regulated. For example, in the EU, buying naked CDS on government bonds is NOT allowed to avoid speculation attacks on countries.

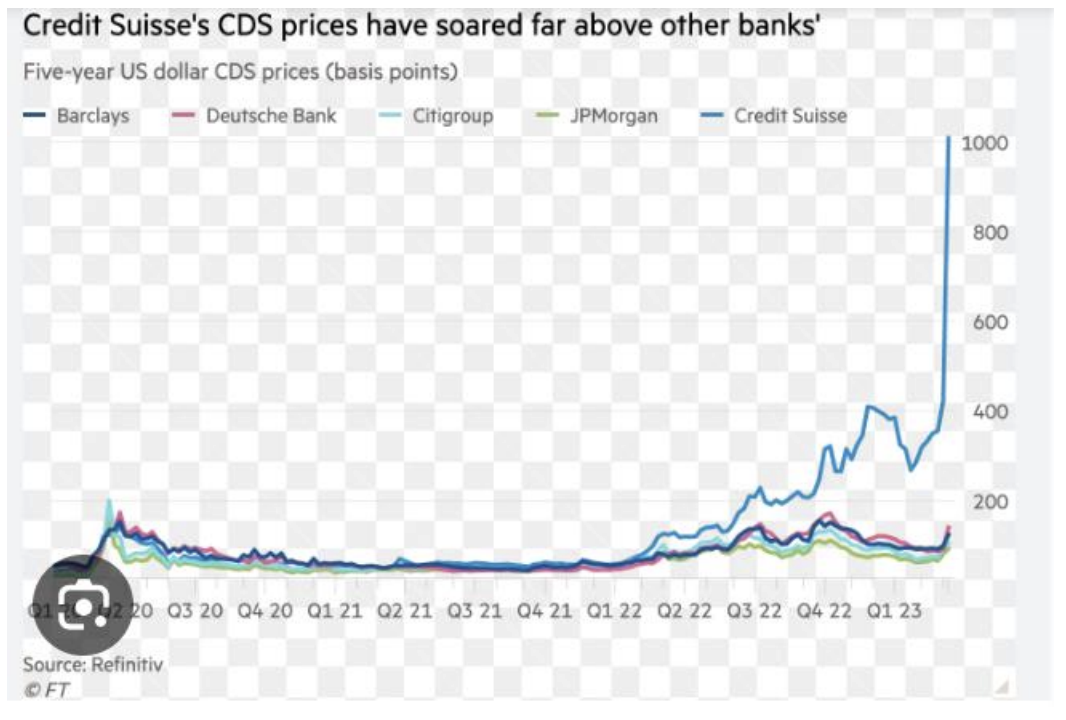

Example during the Credit Suisse Crisis, CDS of that bank went incredibly high.

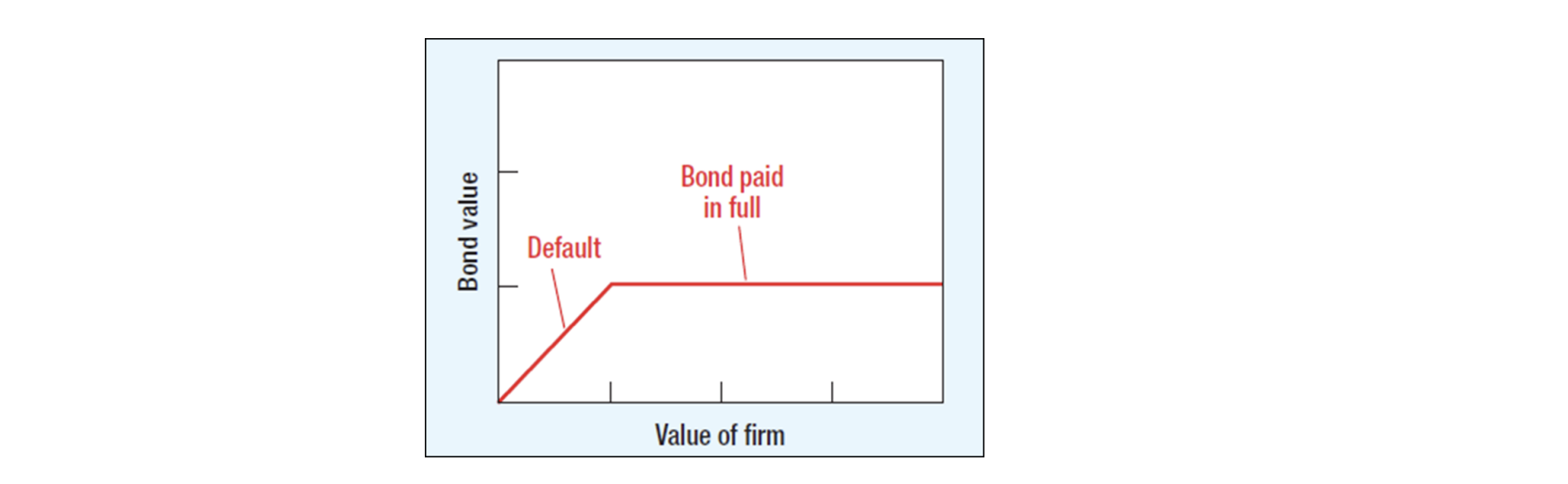

The main difference between corporate and treasury bonds is that the company has the option to default, whereas the government supposedly doesn't.

Consider the following example:

Giacomo's GmbH borrowed per share but then the firm faced hard times and market value of its assets fell to .

Giacomo's Bond and stock prices fell respectively to and .

If Giacomo's debt were due and payable now, the firm could not pay the originally borrowed, it would default leaving bondholders with assets worth USD 30 and shareholders with nothing.

However... the reason the stock has a market value of $3 CHF£ is that the debt is NOT due immediately, but one year from now.

But, Giacomo is not compelled to repay the debt at maturity, why?

- If the value of assets : the value of the assets is less than it owes to the bondholders. Therefore, it will exercise its option to default on the debt and the debtholders will receive the assets.

So, Giacomo's GmbH issued a safe bond, but at the same time acquired an option to sell the firm’s assets to the bondholders for the amount of the debt. The exercise price is for this bond, e.g., the face value of the bond

- If the value of assets : Giacomo will not exercise the option to default.

In general terms, we can say:

Intuition: the Default Put represents the value of the "limited liability" granted to the company's owners.

For example, if we assume returns on firm's assets , risk free-rate and a current value of assets , exercise price of default option , we get:

From the Black Scholes model, we get that the value of the default put is and:

In, general, we can incurr in the following scenarios:

| If there's an increase in... | Value of default put |

|---|---|

| Value of company's assets | Declines |

| Standard deviation of asset value (risk) | Rises |

| Amount of outstanding debt | Rises |

| Debt maturity | Rises |

| Default-free interest rate | Dceclines |

| Dividend payments | Rises |

Ratings

Ratings are given by ratings agencies (S&P, Moody's, Fitch, AM Best etc etc...).

The highest quality bonds are rated triple-A ().

- Investment-grade bonds are the equivalent of or higher

- Below that, they are called junk bonds (or NON-investment-grade).

Based on the financial ratios, this is an overview of the median rations for U.S. nonfinancial firms.

| Ratio | Aa | A | Baa | Ba | B | Caa-C |

|---|---|---|---|---|---|---|

| Operating margin (%) | 15.2 | 9.1 | 9.3 | 9.7 | 7.7 | -0.4 |

| Pre-tax return on assets (%) | 10.7 | 7.0 | 6.1 | 6.1 | 5.6 | 0.8 |

| Long- plus short-term debt ratio (%) | 41.5 | 46.7 | 48.4 | 55.9 | 68.1 | 94.4 |

| Interest coverage | 20.8 | 10.3 | 6.2 | 3.7 | 1.8 | 0.2 |

Instead of comparing different ratio, a common way of evaluating the possibility of default is merging them in a single index: The Altman's Z Score, computed as:

where:

- working capital / total assets

- retained earnigs / total assets

- EBIT / total assets

- market value of equity / total liabilities

- sales / total assets

Common interpretations:

- : safe zone

- : grey zone

- : red zone

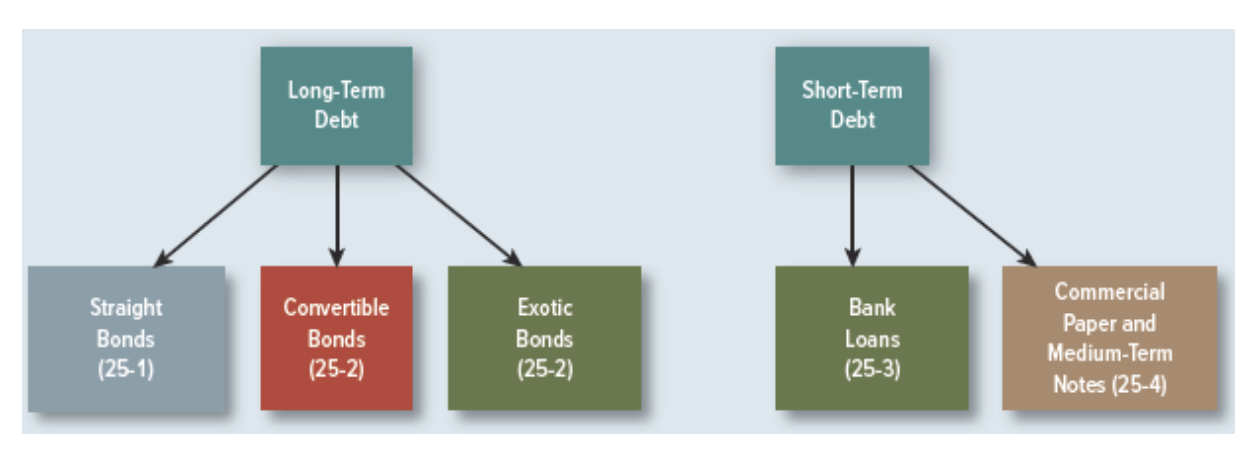

4. The Many Different Kinds of Debt

Before we start, some bond terminology:

- indenture/trust deed: between the company and a trustee that represents the bond-holders. The trustee must see that the terms of the indenture are respected and look after the bond-holders in case of default. (usually a big commercial bank that monitors and acts in case of default)

- registered bond: the company keeps records of the owners, interest and principal are paid directly to the bondholders (the big majority of bonds traded today)

- bearer bond: the company doesn't keep records of the owners, who have to physically cut off a coupon and present it to a bank to receive the interest payment

- accrued interest: amount of accumulated interest since the last coupon payment

- coupon: annual/semi-annual interest paid on a bond

- debentures (=bonds): long term unsecured issues on debt

- mortgage bonds: long term secured debt, often containing claims against a specific property

- collateral trust bonds: bonds secured by common stocks of other securities from the borrower

- equipment trust certificate: secured debt generally used to finance railroad equipment

- asset-backed securities (ABS): sale of cash-flows derived directly from a set of bundled assets

- mortgage-backed securities: set of mortgage loans sold, owners receive a portion of mortgage payments (off-balance sheet).

- foreign bond: bonds sold to local investors in another country's bond market

- yankee bond: bonds sold publicly by a foreign company in the US

- samurai: bonds sold by a foreign firm in Japan

- bulldog: bonds sold by a foreign firm in the UK

- eurobond: bond denominated in one country's currency but marketed internationally

- global bonds: very large bond issues marketed internationally and on individual domestic markets.

A callable bond allows the issuer to call back (repay) the debt before maturity, valuable to reduce the company's leverage, it often happens when interest rates fall.

A puttable (retractable) bond allows the investor to be repaid for the debt, it is a protective covenant for the investor, it often happens when interest rates increase.

A sinking fund is a fund established to retire debt before maturity.

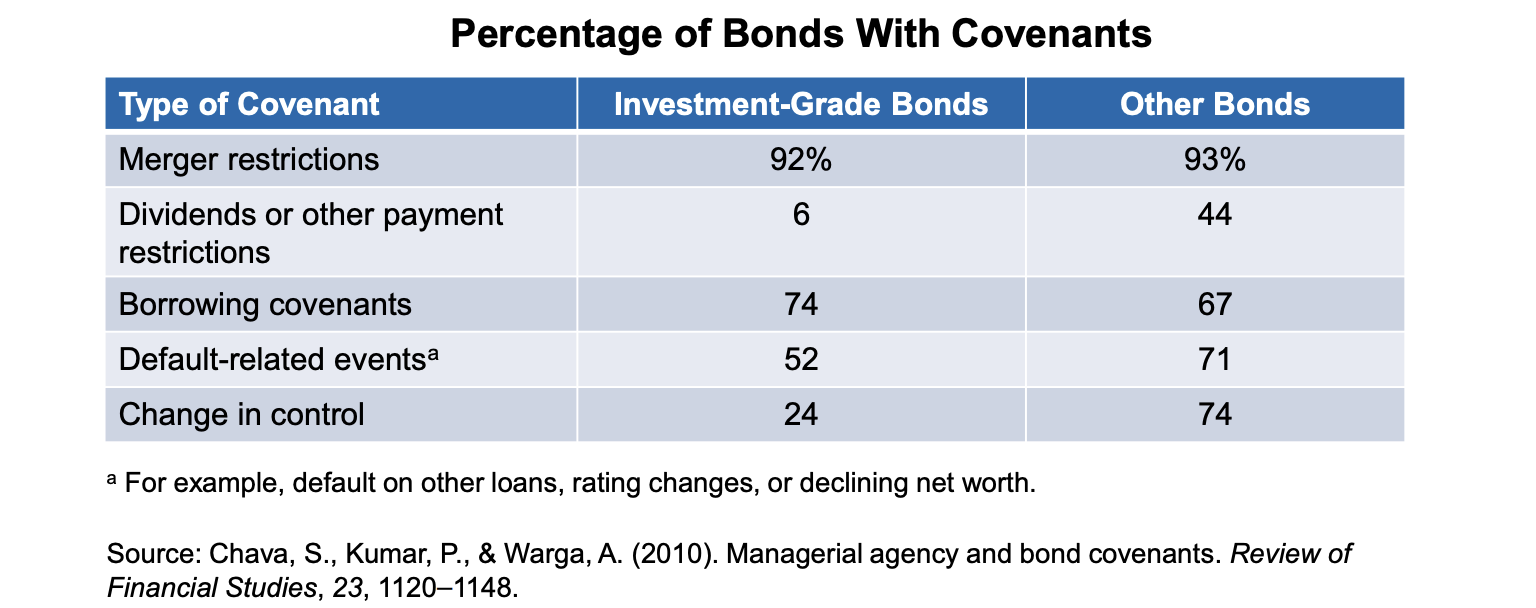

Bond covenantsSince investors know that there's risk of default, covenants are used to limit the company default position, for example by:

- debt ratios: limits of further borrowing (senior debt limits senior borrowing, junior debt limits senior and junior borrowing).

- Security: negative pledge: the company promises not to give any of its assets to create a security interest for other lenders, unless the current bondholders are given an equal share of that security.

- Leasing (similar to secured borrowing)

- Dividends

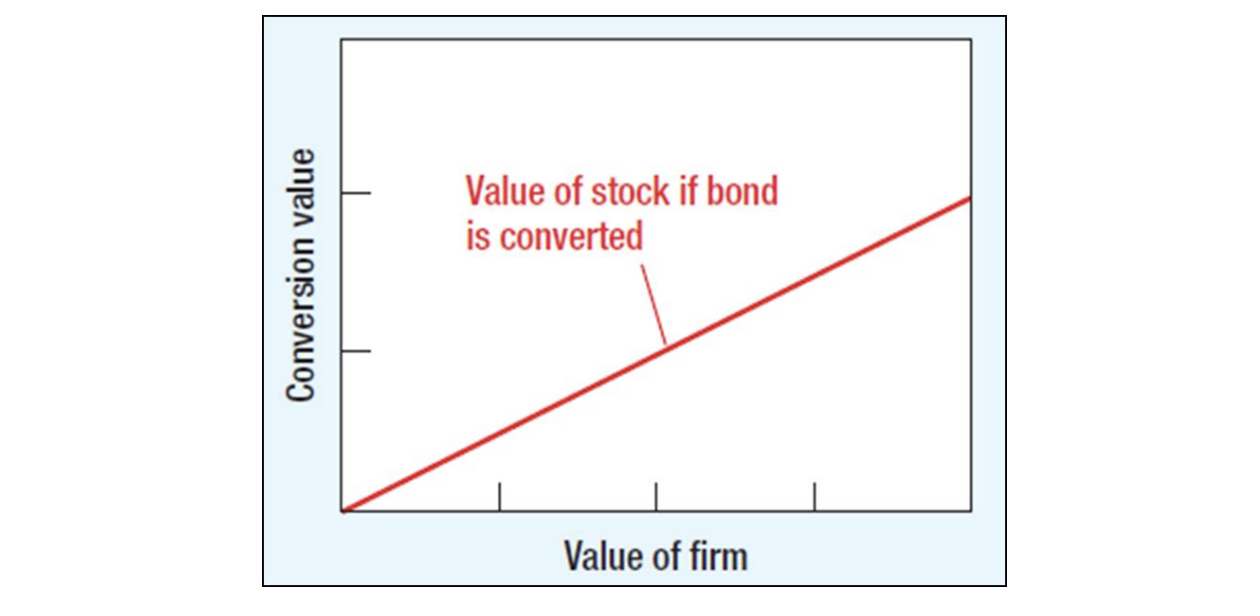

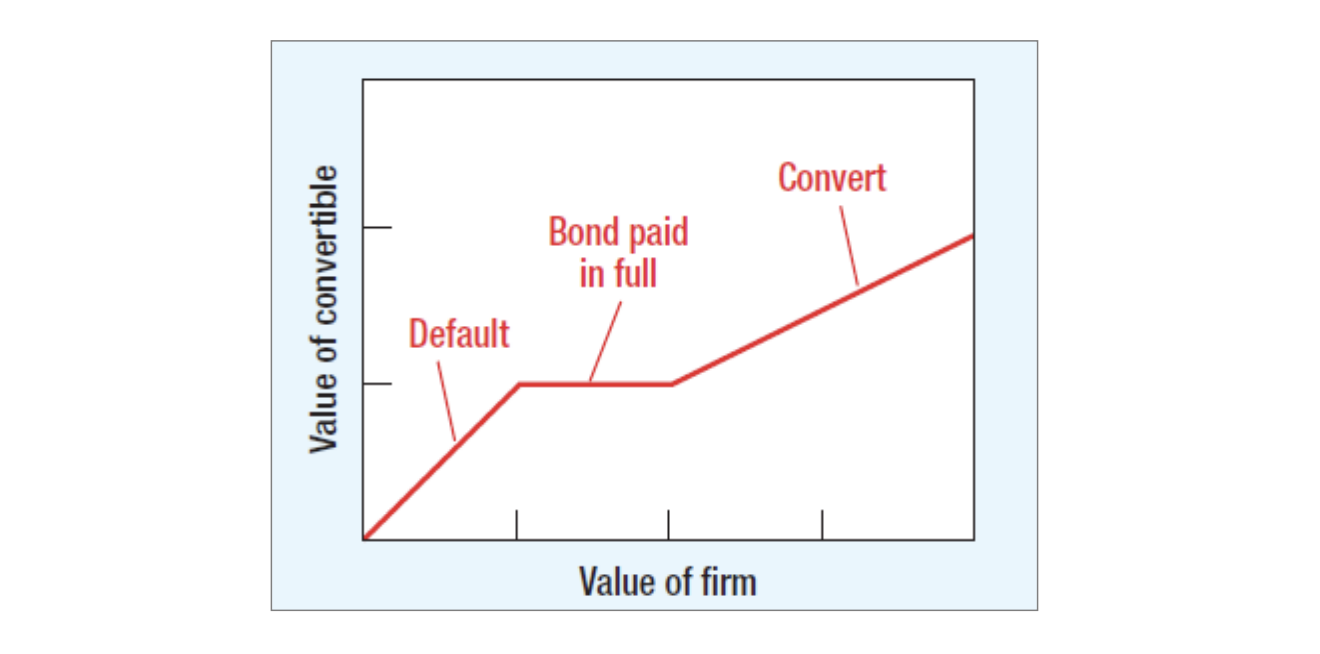

A convertible security can change during its life: it starts as a bond, but it can be subsequently turned into equity.

- Value of the plain bond (if not converted), think of this value as a lower bound of the price of the convertible bond:

- Value of the converted bond/stock if the bond is converted:

- At maturity, the bondholder can choose to receive the payment of the bond or convert it into common stock:

Instead of selling convertible bonds, firms sometimes sell a package of straight bonds and warrants. Warrants are simply long-term call options that give the investor the right to buy equity.

Warrants are usually issued privately, can be detached, exercised for cash and are usually taxed differently. Note also that warrants can be issued on their own.

Bond innovations

- Catastrophe (CAT) bonds: payments are reduced in the event of a specified natural disaster

- Contingent convertibles (CoCos): bonds that convert automatically into equity as the value of the company falls

- Equity-linked bonds: payments are linked to the performance of a stock market index

- Longevity bonds: payments are reduced or eliminated if there's a fall in mortality rates

- Mortality bonds: payments are reduced or eliminated if there's a jump in mortality rates

- Pay-in-kind bonds (PKIs): issuer can choose to make interest payments in cash or in more bonds with same face value

- Credit-linked bonds: coupon rate changes with the company's rating

- Reverse floaters (yield-curve notes): floating-rate bonds that pay a higher rate of interest when other interest rates fall (and a lower rate when other rates rise)

- Set-up bonds: coupon payments increase over time.

Bank Loans

Commitment:

- Revolving credit: maximum amount a company can borrow, repay, and re-borrow as needed during the period.

- Evergreen credit: revolving credit without a fixed maturity that automatically renews.

Maturity

- Bridge loan: short-term loan between permanent financing or important debt events

- Self-liquidating: loan designed to be repaid by the asset it was used to purchase.

- Term loans: standard loans for a specific amount that are repaid over a set period (usually 1–10 years)

In a Syndicated Loan, a group of banks (the syndicate) works together to provide the funds.

- Lead Bank: Arranges the deal and does the heavy lifting.

- Participants

LIBOR: it was the interbank offered rate, commonly used as the reference for loans. The financial crisis undercut confidence in LIBOR, now it is no longer used.

SOFR (SECURED OVERNIGHT FINANCING RATE): designed to replace LIBOR, it is the average interest rates on overnight Treasury repo transactions (the main difference is that SOFR is transaction-based, not banker-estimated based as the LIBOR).

In an overnight repo transaction, one party sells a security (usually a US Treasury Bond) to another party with a simultaneous agreement to buy it back the very next day at a slightly higher price.

5. Leasing

A lease is a rental agreement that involves a series of fixed payments from the lessee (user) to the lessor (owner).

- Operating lease: short-term, cancelable. (Historically, these were "off-balance sheet," but modern accounting standards (like IFRS 16) now require to be recognized as liabilities.)

- Financial lease: long-term, non cancelable. (Often, at the end of the term, the lessee often has the option to buy the asset).

Some more possibilities in leasing include:

- Rental lease (full service): the lessor handles everything, including maintenance, insurance and taxes.

- Net lease: the opposite of full service.

- Direct lease: arrangement where the lessee identifies an asset, and the lessor (often a bank or leasing company) buys it from the manufacturer just to lease it to the lessee.

- Sale and leaseback: A company sells an asset they already own (like a headquarters building) to a buyer and immediately leases it back in order to unlock some capital (liquidity) while still using the asset.

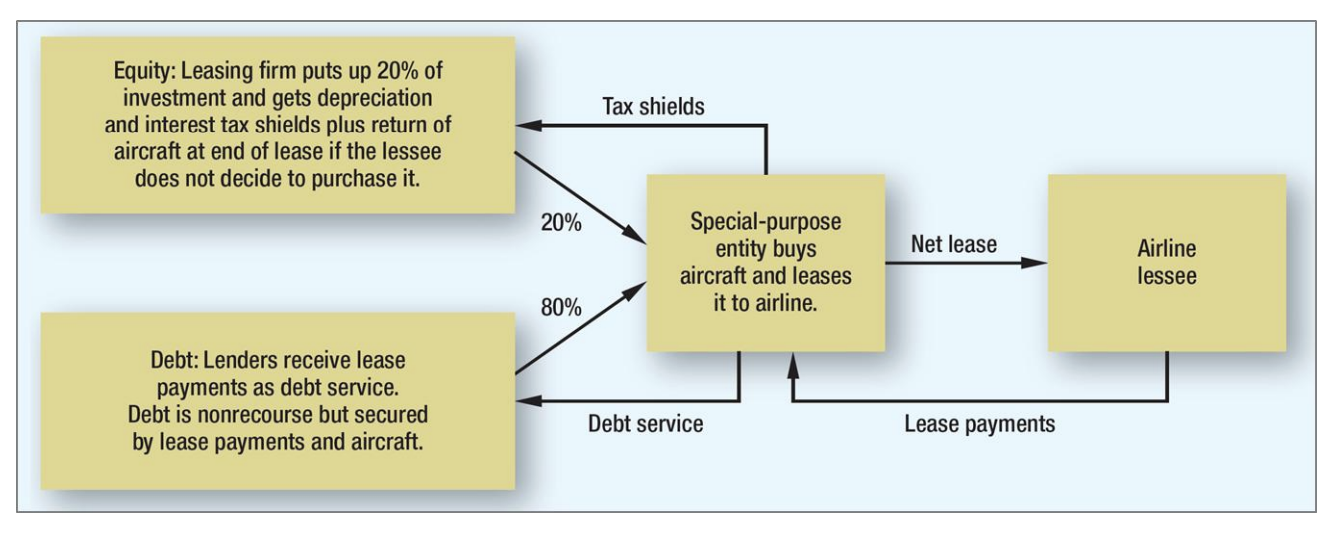

- Leveraged lease: a three-party transaction involving a lessee, a lessor, and a lender. The lessor borrows a significant portion of the asset's cost (usually to ) to purchase it.

PROs of leasing:

- short-term leases are often convenient

- maintenance is provided

- standardization leads to lower costs

- tax shields/advantages can be used

- leasing preserves capital

CONs of leasing:

- leasing avoids capital expenditures control

- leases may be off-balance sheet financing

What happens if a bankrupt lessee takes a lease? What happens if the lease is rejected?

If the lease is confirmed, the lessee continues to use the asset and must sustain the payments. If the lease is rejected, the asset is returned to the lessor.

If the value of the returned asset is not enough to cover the remaining payments, the lessor's loss becomes an unsecured claim on the bankrupt firm.

Operating Leases

The Equivalent Annual Cost of an asset is the rental payment sufficient to cover the present value of all the costs of owning and operating an asset. The rental payments are hypothetical, (just a way of converting a present value to an annual cost). In the leasing business the payments are real.

If a business/firm needs an asset:

- buy it if the equivalent annual cost of ownership and operating is less than the best lease rate

- if it plans to use it for extended period, usually annual cost of ownership and operating is less than the leasing rate. There are two corner cases here operating lease make even sense despite the higher cost:

- the lessor is able to manage the asset more efficiently/at less expense than the lessee

- operating leases often contain useful options

As mentioned before, historically, operating leases have been off-balance sheet. Consider then the following scenario.

Suppose that, in the past (when leaes were off-balance sheet), a company needed one asset. It has two main options:

- borrow the capital and buy the asset the debt shows up under the liabilities, the bought asset under assets.

- lease the asset the lease rate shows up under expenses in the income statement, no impact on the Balance Sheet.

Companies usually preferred the second option because, by keeping the new need off the balance sheet, they showed stronger financial metrics:

- Lower Leverage: Debt-to-Equity ratios look lower

- Higher ROA: Return on Assets () looks higher because the "Total Assets" denominator is smaller.

According to actual accounting standards however, most leases (even operating ones) must now be recorded on the balance sheet as a Right-of-Use (ROU) Asset and a corresponding Lease Liability.

Suppose then the following example.

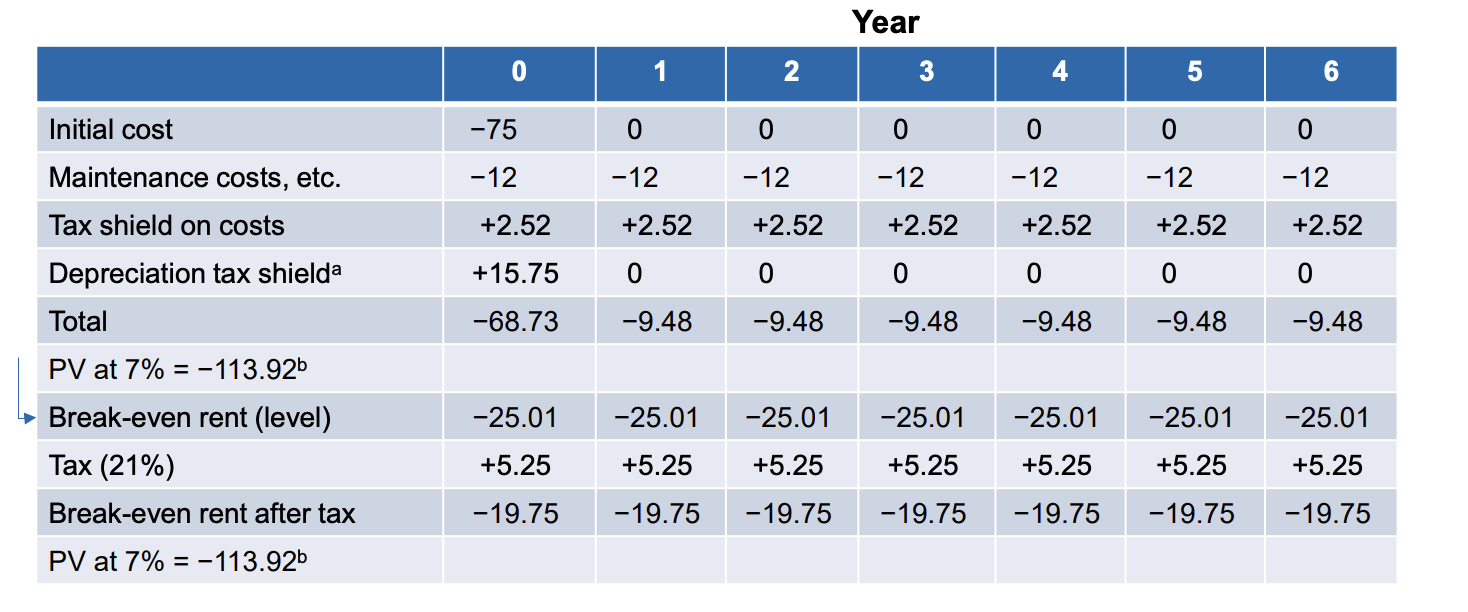

Giacomo's GmbH needs to buy a camper-van and asks for a 1-year lease to RoadSurfer GmBh. How much should RoadSurfer charge for that lease?

Knowing all its costs (initial cost, maintenance, tax shields, depreciation) RoadSurfer can then calculate it's break-even rent.

Financial Leases

Consider now the following example. Giacomo GmBh is again considering to buy a camper-van worth with a 8 years life. Roadsurfer offers the 8 years loan at per year, but Giacomo remains responsible for maintenance, insurance and operating expenses.

To calculate the Net Present Value of the lease, we have to value the incremental cash flows from the lease and discount them at the after-tax interest rate.

Another financing options would be represented by loan. To compare leasing and loans, we can compare a lease to a loan that has the same impact on future cash flow.

- The lease requires paying /year for 7 years.

- We create a hypothetical loan that also requires paying /year _("Net cash flow of equivalent loan" row):.

Considering the same interest rate, we then see which one brings the bigger amount of money at time 0:

- The loan gives you today in exchange for those future 12.80 payments.

- The lease gives you (the value of the asset you get to use) for the same future payments.

Leveraged Lease

6. Managing Risk, Options

Why manage riskReason why risk reduction does NOT add value:

- hedging is a zero sum game

- investors can hedge themself they have a do-it yourself alternative

Insurance

Most businesses face the risk of events that can cause financial stress to them (both financial or business-related risks). The cost and risk of a loss can be shared by others who share the same risk the firm can transfer the risk to an insurance company.

Catastrophe bonds (CAT bonds) allow insurers to transfer risk to bondholders by selling bonds whose cash flow payments depend on the level of insurable losses NOT occurring.

More on CAT bonds here [Investopedia].

- on some CAT bonds (Indemnity Trigger), payments are reduced if claims against the issuer exceed a limit the problem is that the insurance company, knowing this, may try to underwrite more counterparties to gain additional premia, therefore creating a problem of moral hazard for the insurance company (since it has less incentives to be careful)

- in some other cases (Index Trigger), payments are reduced if claims against the entire industry exceed a limit partial solution to the moral hazard problem

Understanding options: terminology

- Derivatives: any financial contract derived from another

- Option: gives the holder the right to buy/sell a security in the future at specified price

- Option Premium: price paid for the option above the price of the underlying

- Intrinsic Value: difference between the strike price and the security price

- Time Premium: value of the option above the intrinsic value

- Exercise Price (Strike): price at which the underlying can be bought/sold

- Expiration Date (Maturity): last date on which the option can be exercised

- American Option: can be exercised any time

- European Option: can be exercised only on the expiration

The Put-Call Parity

- a call option gives the right to buy the underlying.

- a put option gives the right to sell the underlying.

For an European Option:

- : premium of the call option

- premium of the put option

- : present value of the strike price

- : underlying price

The idea behind the put-call parity equation is that the two following portfolio must have the same value, otherwise we end up with an arbitrage opportunity:

- Portfolio 1:

- Portfolio 2:

In case this equation doesn't hold, there's of course an arbitrage opportunity and, to capture a profit, the following strategies can be used:

-

:

- Reversal (the Call is overpriced):

- The "synthetic" stock position (the call and the cash) is worth more than the actual stock and the put.

- Strategy Sell the Call, Borrow the present value of the strike price, Buy the Put, and Buy the Stock.

-

:

- Conversion (the Put is overpriced):

- Strategy: Buy the Call, Lend (invest) the present value of the strike price, Sell the Put (Write it), and Short the Stock.

Intuition: given the put-call parity formula we short the "cheapest" side and we go long on the "expensive" one.

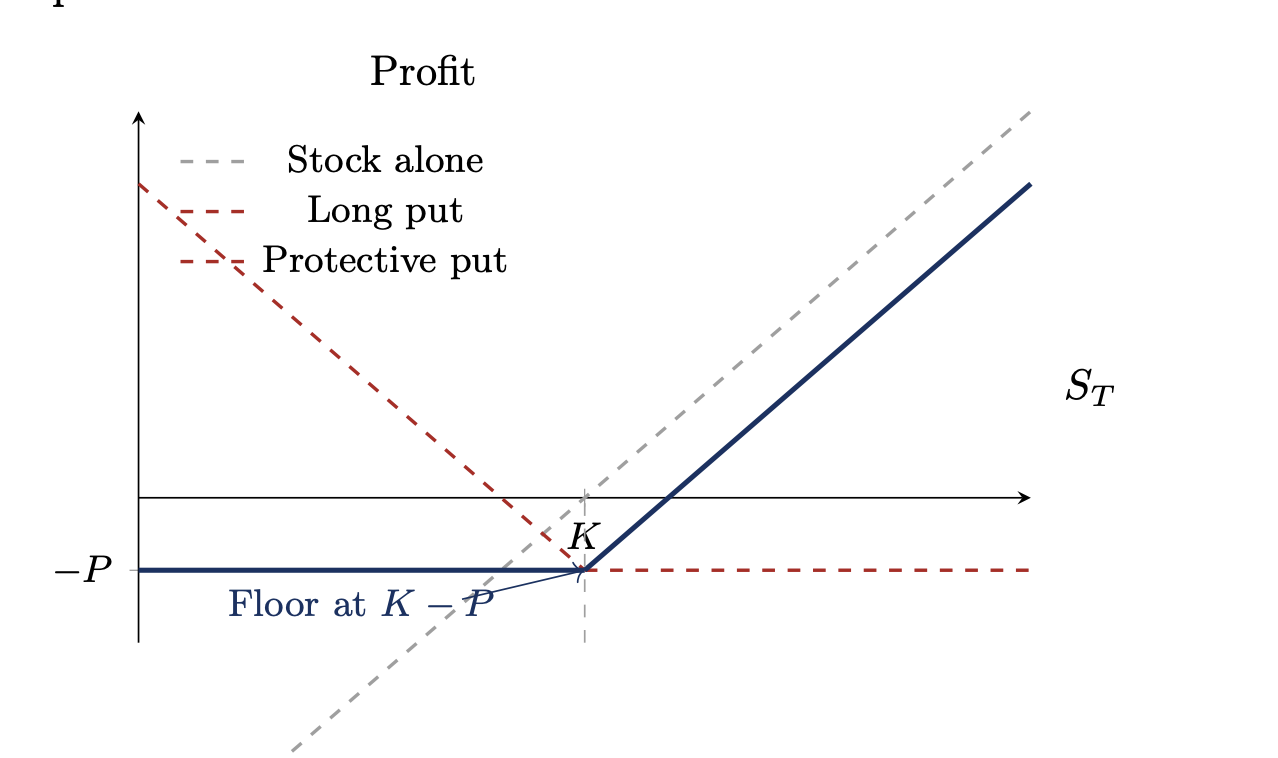

Option Strategies: The Protective Put (Buying Insurance)

A protective put is the combination of:

- a long position in the underlying

- a long put on the same underlying

The put acts as insurance if the asset falls below , the puts pays off and limits the loss. If the asset price rises, the put expires worthless the cost of the strategy is the put premium.

In corporate finance: a finance that owns a large equity stake in a partner company or a fund with equity exposure, may buy puts to protect the downside of its balance sheet without selling the asset_ the protective put is the simplest real-world option strategy (structurally identical to an insurance)

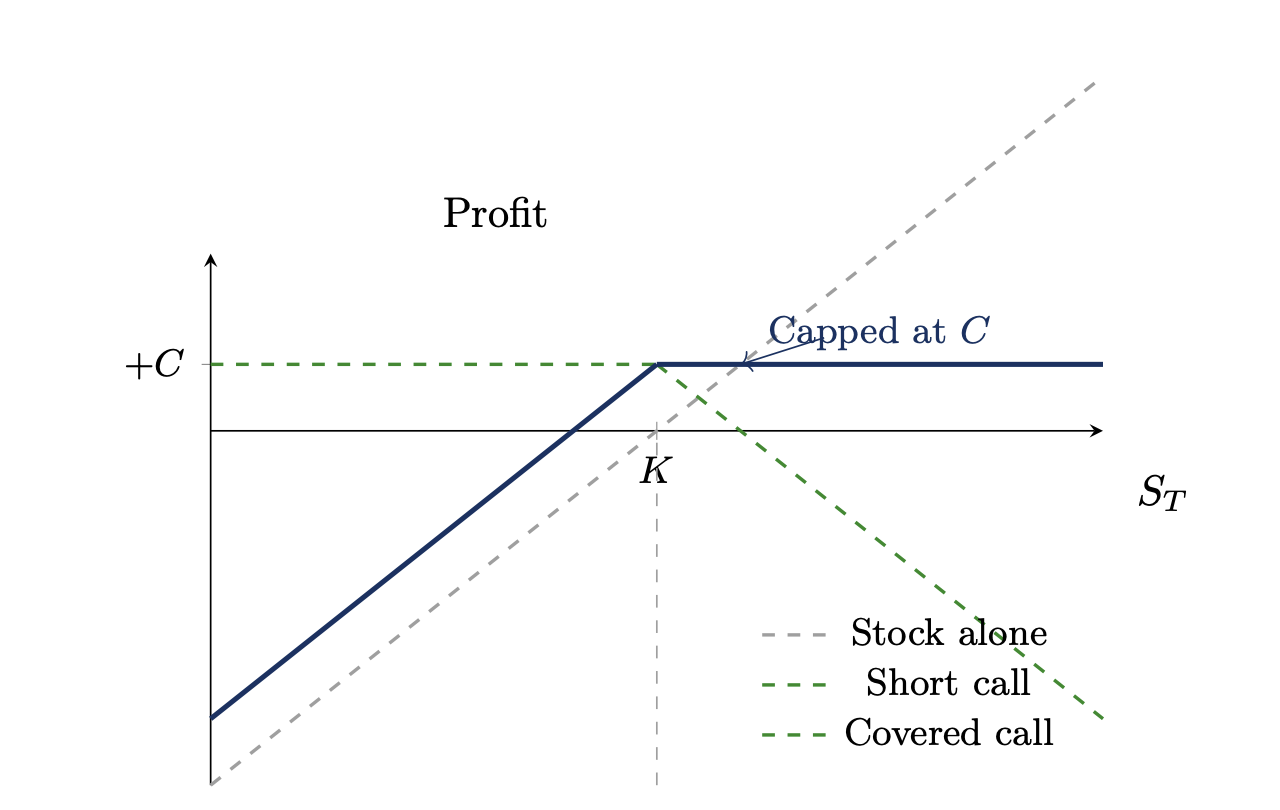

A covered call combines:

- a long position in the underlying

- a short call on the same underlying

By selling the call, the investor collects the premium immediately. In exchange, they give up any gains of the asset above :

- if the asset stays the investor keeps both the asset and the premium

- if the asset rises the investor sells at missing the upside

A firm that has agreed to sell an asset at a fixed future price has implicitly written a covered call.

The covered call structure also appears in a callable bond: the issuer holds the right to redeem early (a call on the bond) which caps the investor's upside in a falling-rate (favorable) environment.

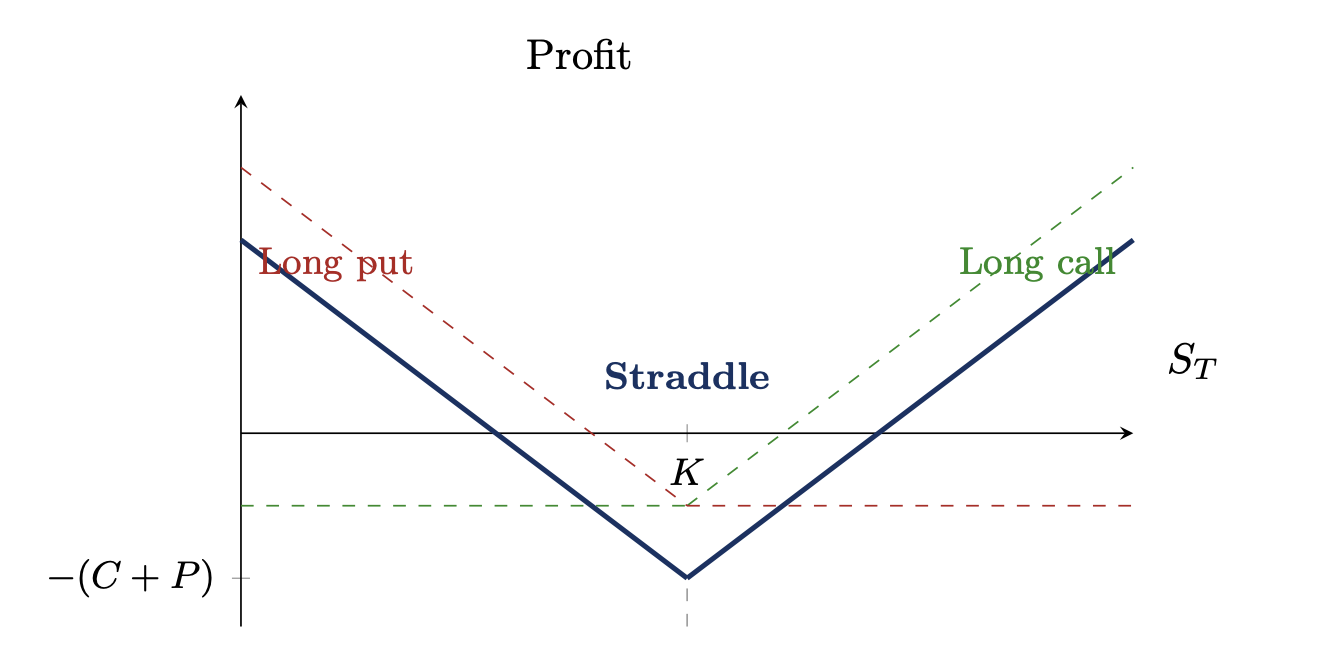

The straddle combines:

- a long call at strike

- a long put at strike with the same maturity

The strategy profits if the underlying moves significantly in either direction and loses if the underlying stays close to the investor is buying volatility.

A firm facing a binary regulation/merger/acquisition is in a similar situation: the outcome is highly uncertain, but the size of the move is predictable even if the direction is not.

Options can be replicated

The fundamental insight behind option pricing and hedging is that, at every moment, the risk of an option position can be offset by taking an appropriate position in the underlying. By continuously adjusting the hedge, the option seller can neutralise their exposure to movements, leaving them with only the time decay f the option, which they collect as a profit.

the option seller does not simply absorb the risk and hope for the best.

To build a replicating strategy, the central concept is Delta () that measures how much the option price changes when the underlying price changes by one unit:

For a call, .

- ATM call has

- ITM call has

- OTM call has

For a put. because the value decreases as the price of the underlying decreases:

- ATM call has

- ITM call has

- OTM call has

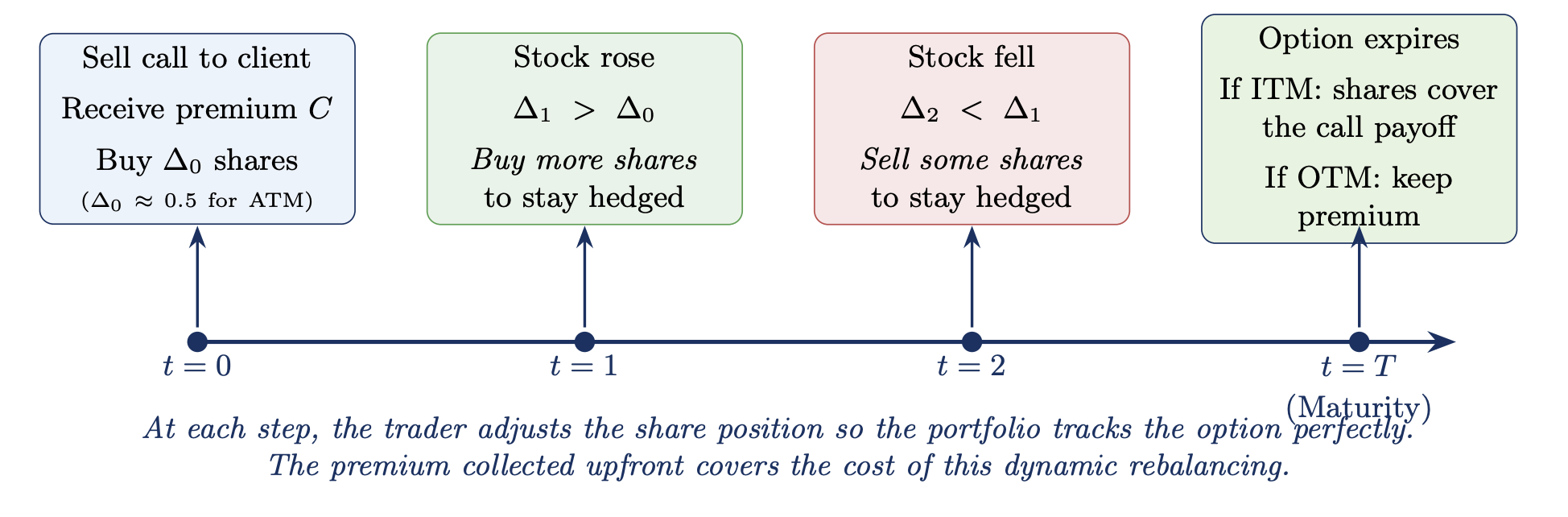

Delta Hedging

To understand how delta hedging works, let's consider a bank selling a call to a client the bank is short on the call (exposed to losses if the stock rises).

To hedge this, the bank buys shares of the underlying for each option sold.

For all the other cases, the logic is identical: for every option sold/purchases, the bank must buy shares of the underlying. However, note that is negative for a put and positive for a call, so the bank either shorts/goes long on the underlying.

At every moment, the bank is holding as many shares as needed to match the option's sensitivity.

Therefore, the option premium is the fair price of a dynamic hedging strategy.

Intuition: option sellers are not irrational, they run a "manufacturing business":

- they take in raw materials (premium)

- they run a production process (delta hedging strategy)

- they deliver a product (option payoff)

This also explains why volatility is so critical to option pricing: higher volatility higher frequency of rebalancing more expensive replication strategy higher premium regardless of the direction.

The limits of the hedge: Gamma riskDelta hedging works well if the trader can rebalance continuously. In practise, rebalancing occurs at discrete intervals, leaving the trader exposed to gamma risk, the risk that the stock jumps between rebalancing intervals and the delta estimation becomes wrong.

Therefore we say that a delta-hedged portfolio is delta-neutral, it doesn't gain or lose value from small moves in , but it still exposed to gamma (large moves), theta (time decay) and vega (volatility changes).

Example: Future and Options for Jack Mining Company

Jack Mining Company is worried about short-term volatility in revenues.

Gold currently sells for USD /ounce, but the price is volatile and could fall to or rise to in the next month. Jack will sell ounces to the market in the same period.

- If Jack remains unhedged (Market Exposure), he remains fully exposed to the "spot" price.

(Where is the spot price and is the quantity of 1,000 ounces)

- If Jack hedges his position with futures (Price Lock), he eliminates all uncertainty by pre-selling their gold at a fixed price, ensuring a guaranteed revenue regardless of the future price.

(Where is the locked-in futures price of $1,310)

- in this case, Jack enters a short position on futures (obligation to sell the ounces at a specified price).

- If Jack hedges with option, he has an "insurance" that sets a minimum sale price (strike ) while allowing them to benefit from higher market prices, but they must subtract the cost of the insurance (premium) from their total.

(Where is the strike price of and is the premium of $110 per ounce)

Generally speaking, a business has:

- Business risk affecting fixed and variable costs and revenues operating leverage

- Financial Risk due to IR, FX, commodity price changes etc...

The basic relationship between futures prices and spot prices for equities:

- : futures price on contract of length

- : spot price (today)

- : risk-free rate

- : dividend yield

For commodities, the basic relationship becomes:

- The net convenience yield is generally positive and future prices are generally below spot prices. _(This dynamic is called backwardation).

- Sometimes storage prices are high and there's plenty of commodities available, so future prices are above spot prices. _(This dynamic is called contango).

Note that the convenience yield is the implicit, non-monetary benefit of physically holding a commodity compared to owning a futures contract (example: avoiding shortages or ensuring production).

Consider also that the holder of a future contract misses out any dividend or interest payment from the underlying but he does not have to pay for storage costs.

Interest Rate Risk

A forward interest rate is a rate for a loan starting in the future. To price it, we use the following formula:

where is the current rate for a -year term and the same applies for .

Interest Rate Swaps

Some future cash flows are fixed, others may vary depending on the interest rates, rates of exchanges or prices of commodities. In a swap contract, one counterparty exchanges a fixed set of cash for a floating set of cash flow and the second counterparty takes the opposite position.

A swap uses a Notional Principal ().

This amount is never exchanged between parties; it is simply the "dummy number" to calculate interest.

- Fixed Rate Payer: Pays an agreed and constant interest rate. They are essentially "shorting" interest rates (betting they will go up).

- Floating Rate Payer: Pays a variable market rate (like SOFR). They are "long" interest rates (betting they will stay low).

In practice, only the difference between the two interest amounts is paid (this reduces credit risk for both parties).

- Scenario A (Market Rate < Fixed Rate): the Fixed Payer pays the difference.

- Scenario B (Market Rate > Fixed Rate): the Floating Payer pays the difference.

- Scenario C (Market Rate = Fixed Rate): no money moves ("Wash" scenario)

When a swap is created, its Net Present Value (NPV) is . The fixed rate is mathematically "calibrated" with discount factor so that the expected value of the floating payments equals the fixed payments today.

To calculate the current value value of an existing swap that changes to a new :

A swap curve (also called the "LIBOR curve/SOFR curve/EURIBOR curve) is the graphical representation of the relationship between swap rates and different maturities (tenors). It's a line that shows you the "fixed rate" the market expects to pay for a swap lasting different maturities.

Currency Swaps

A currency swap is a contract where two parties exchange cash flows in different currencies over time.

It can be decomposed in:

- a spot FX transaction today

- plus a series of interest payments

- plus a reverse FX transaction at maturity

Heding Interest Rate Risk

When a business receive cash flows that depends on interest rate, the firm can manage its risk by buying a bond and matching duration. In this way, exposure to small interest rate changes is zero.

In general, if we want to hedge against changes in the value of asset (oil) using an offsetting sale of asset (example: oil futures), we use the following formula:

- : sensitivity of to change in value of (hedge ratio)

- : unexpected drift/changes

7. International Financial Management

The Forward Premium/DiscountThe forward-premium measures whether the market expects a currency to be more expensive or cheaper in the future compared to right now. It is represented by the annualized rate, defined as:

- If the result is Positive (+): the currency is at a Forward Premium (It is expected to become more expensive).

- If the result is Negative (-): the currency is at a Forward Discount (It is expected to become cheaper).

In general, these relationships are known as the International Fisher Effect (IFE) and Interest Rate Parity (IRP), that describe the equilibrium between a home/domestic currency () and a foreign currency ().

The Fisher Effect represents the relationship between nominal interest rates () and expected inflation (). In an efficient market, the ratio of nominal interest rates equals the ratio of expected inflation:

The Interest Parity Equation shows that the difference between the Spot rate () and the Forward rate () should offset the difference in interest rates between the two countries to prevent arbitrage:

We can then add a final equation, the Purchasing Power Parity: it explains that the expected change in the exchange rate is driven by the difference in inflation rates between the two countries:

If combine them all, we get the the International Finance Linkages ("Four-Way Equivalence"):

The Cost of Capital for International Investments

When calculating the cost of capital in an international context, we need to adjust local valuation to account for foreign exchange risk, country risk, and differing inflation rates.

To obtain the required return for a project, the Capital Asset Pricing Model (CAPM) is often the starting point:

To discount the expected cash flows in another currency, we convert the cost of capital from to second currency _( in the following example)

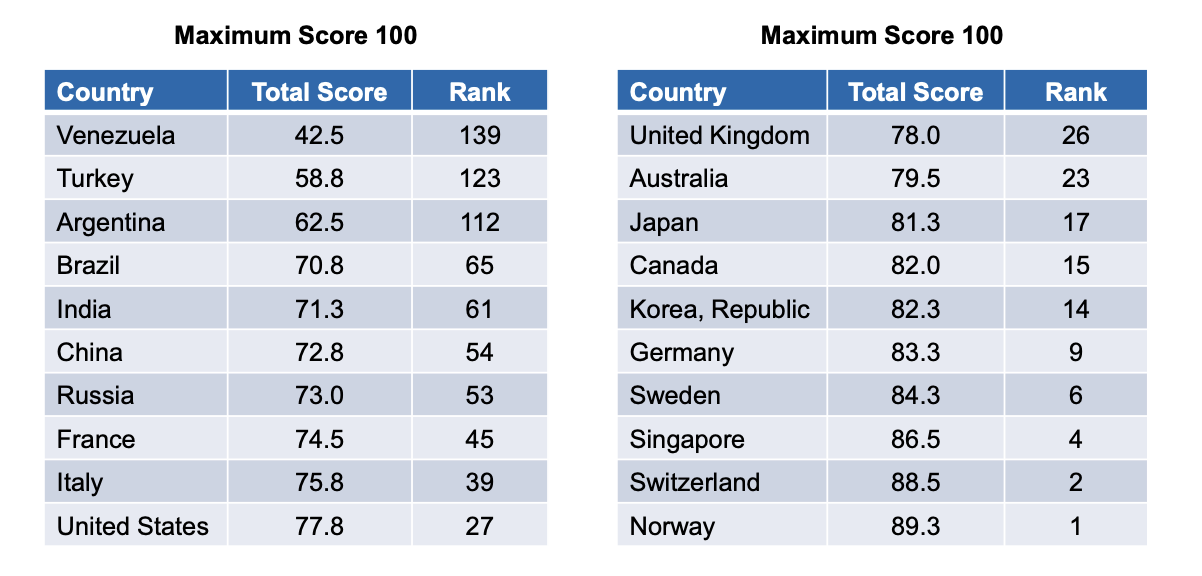

Note that this formula (or method) doesn't take into account business risk!(every country is exposed to risk, but some parts of the world are more vulnerable, see the below table).

8. Financial Analysis

The Balance Sheet- Assets are listed in declining order of liquidity

- Current assets are inventories of raw materials, WIP and finished goods

- Current liabilities include debts that are due to be repaid and payables

- Net Working Capital indicates a company has sufficient short-term assets to cover its debt, signaling financial stability.

The Income Statement

To measure revenues and earnings:

To measure margin:

To measure profit (net operating profit after tax) and cash flow:

Other relevant metrics:

Financial Metrics

The Total Market Capitalization is the total market of equity:

The Market Value Added (MVA) is the Market Cap minus the book value of equity:

The Market-to-Book Ratio summarizes the previous information:

The residual income is the net dollar return after deducting the cost of capital.

The Economic Value Added (EVA) is then defined as:

Accounting Rates of Return Measuring Efficiency

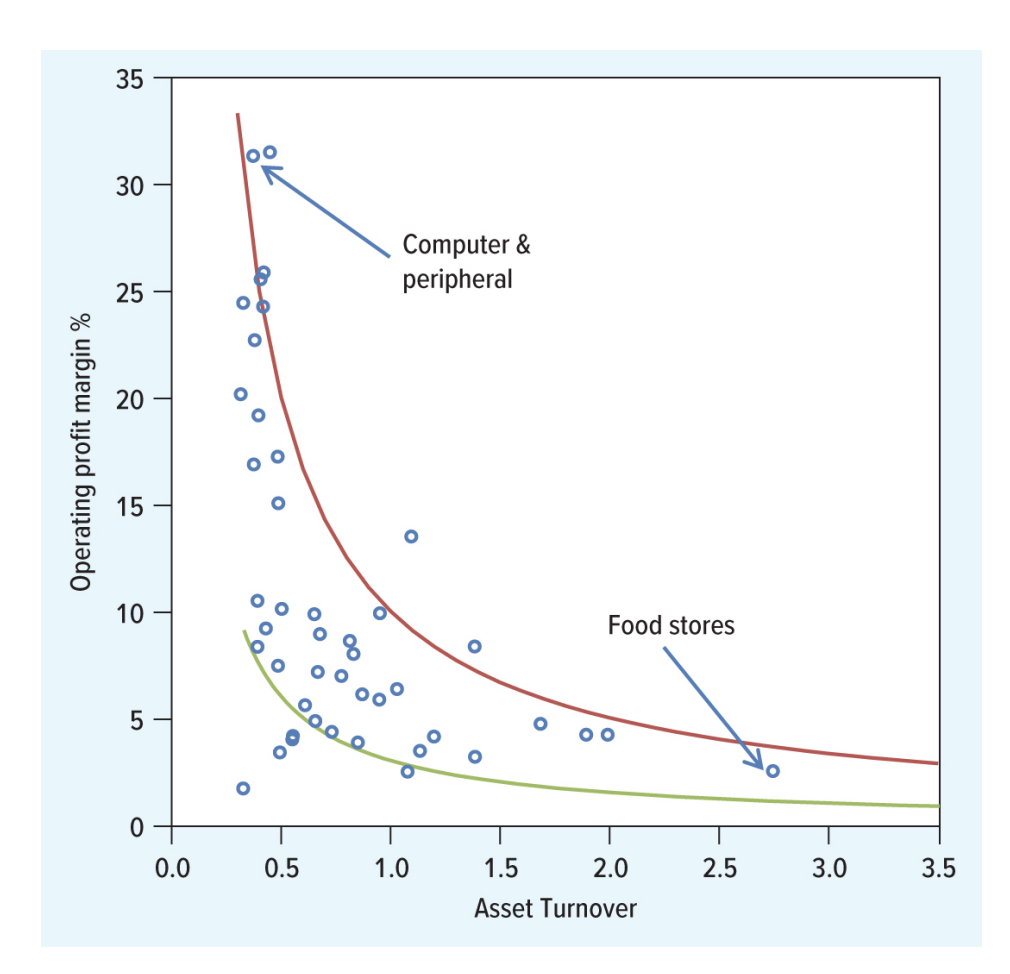

Note that ROE can be decomposed in Asset Turnover (measuring how efficiently a company uses its assets to generate profits) and Operating Profit Margin (measuring how much out of every dollar keeps in earnings) with the Du-Pont System:

However, unlike market-value based measures, these indices show the current performance and are not affected by future expectations. Moreover, in some industries (pharma, start-up etc...), and would be negative although the projects might be on track with a positive NPV.

Finally, book-equity is reduced when companies repurchase stocks and this can make nonsensical measures of of the book-rate of return.

Other relevant efficiency metrics are:

This ratio measures how many times a year a company sells and replaces its entire inventory, the following one translates this info into days:

The same logic can be applied to receivables (how many times per year a company collects its average accounts receivables):

Measuring Leverage

Total-debt ratio shows what percentage of the company's assets are financed by creditors (and not shareholders).

The following one shows how easily a company can pay its interest expenses out of its EBIT.

Since depreciation is a non-cash expense, this ratio adds it back to provide a more accurate picture of the available to pay interest.

Leverage and the Return on EquityMeasuring Liquidity

The NWC to Total-assets shows what percentage of the company's total resources is tied up in working capital.

The Current-ratio is the standard metric used to determine if a company can cover its short-term obligations.

The Quick Ratio (also known as ACID-TEST) includes only the most liquid assets: cash, short-term investments, and money owed by customers (receivables). It excludes inventory because selling products can take time and isn't guaranteed.

The Cash-ratio is the most conservative liquidity measure: it looks only at actual cash and marketable securities on hand.

9. Financial Planning, Working Capital Management

Capital requirements are very different depending on whether a company operates in the financial sector or not.

For most non-financial businesses, capital requirements refer to the total financial resources needed to operate and can be decomposed into:

- Fixed Capital: Money needed for long-term assets (like machinery, buildings, or vehicles ...)

- Working Capital: The cash needed for day-to-day operations (paying salaries, buying inventory, and covering rent ...)

- Statutory Minimum Capital: In many countries, you cannot legally register a "Limited" company without proving you have a certain amount of money in advance.

In contrast, for financial businesses, capital requirements represent a strict law. Regulators (the Federal Reserve or the ECB) mandate that banks hold a specific percentage of their assets as "capital" (equity) rather than debt.

Financial ForecastingWe start with the distinction between profit and cash:

- accrual accounting recognizes revenue when earned and expenses when incurred, it represents profitability.

- cash flow accounting tracks the actual money flow, it represents liquidity.

Any financial manager must ensure that the company has enough cash to support its operations:

Cash can be affected by:

- Sources: net income, depreciation (since it is a non cash-expense, is usually subtracted to the revenues to calculate net income even if there was no actual cash outflow), new debt, sale of assets, increase in payables (meaning that the company is still keeping cash/delaying the payments).

- Uses: dividends, CAPEX, stock repurchase, increase in inventory/receivables

Note that a company with positive net income can need cash due to rapid expansion and inventory needs.

Generally speaking, there are 4 steps to build a robust cash budget:

- forecast sources

- forecast uses

- calculate the net flow

- evaluate and adjust.

Short-term Financing and Tactical Liquidity

After identifying when a company needs money, it has to understand where to get it.

We start by analyzing two specific mechanisms for short-term financing:

- bank loans: very accessible and regulated for stable firms.

- stretching payables (delaying payments to suppliers with an interest cost).

Note that stretching payments is rarely free. It can solve immediate liquidity crisis, but it carries a high implicit cost, making it more expensive than a bank loan and risking to damage the company's creditworthiness with suppliers.

On the other side, the riskiness of debt financing is given by its average maturity the longer the average maturity, the lower the refinancing risk since the company _"locks in" the money for a longer period. With shorter maturities, a company is more exposed to tiny changes in the interest rate,

Short maturities also imply that a company will have to repay back its debt sooner or more frequently, resulting bigger cash outflows/inflows.

Therefore, lengthening the maturity profile in low interest rate periods reduces interest rate expenses in high interest periods. However, long maturities are not always available in the market (especially for lower rated companies).

Once a plan is drafted, it is usually stressed using financial ratios with two important metrics:

- Current Ratio: , measuring the company's ability to pay off all its short-term liabilities using short-term assets.

- Quick Ratio: , measuring the "quickest" assets that can be turned into cash almost instantly.

Company valuation

Cash flow is also very useful to determine how much a company is worth (now and in the future), discounting its free cash flows.

However, when discounting, note that models are only as good as their assumptions:

- many models assume costs always stay at a fixed % of sales, in reality fixed costs may also vary independently of sales volume

- most models generate accounting numbers (net income) but investors care more about cash flows.

- including too many (and unnecessary) info can distract from the important decisions.

Working Capital and Treasury Optimization

Net Working Capital is the difference between current assets and liabilities, it represents the cushion of liquidity a firm needs to stay operational (it varies depending on the industry: Pharmaceutical also show very high NWC %, utilities very low %).

Similarly, the Operating Cycle defined the time from the purchase of raw materials to the collection of cash from the sale of finished goods.

And, lastly, Cash cycle represents the time during which the company's cash is actually tied up:

Example: U.S. manufacturing firms in 2023 had an average cash cycle of 65 days they had to wait over 9 weeks to get their money back after paying for materials.

On the other hand, for retail and grocery industries the typical cash cycle is short or negative, since companies use negative working capital as a source of free financing by selling inventory before paying suppliers.

To shorten the cash cycle, a firm should:

- balance the cost of holding inventory (carrying costs) against the cost of ordering more frequently

- define clear Terms of Sale to manage receivables credits.

- (Example: 2/10 net 30 means that the customer gets a 2% discount if they pay within 10 days, otherwise the full amount due in 30 days)

- In case of the need of immediate cash, a firm can sell its account receivables to a financial institution (a "factor") that collects the debt for a fee.

Furthermore, note that cash earns zero interest, therefore treasury managers use "sweep" programs to move excess cash into Money Market Investments to earn a return while still maintaining liquidity.

Some common investments vehicles are:

- Commercial Paper (CP): unsecured short-term promissory notes issued by large firms

- Repurchase agreements (Repos): selling securities with an agreement to buy them back in order to receive cash

- Banker's acceptance (BAs): a "demand to pay" that has been guaranteed by a bank.

11. The Art of M&A: Investment banking at UBS

The following chapters comes from the UBS Guest Lecture - Advanced Finance ETH Course, Spring 2026

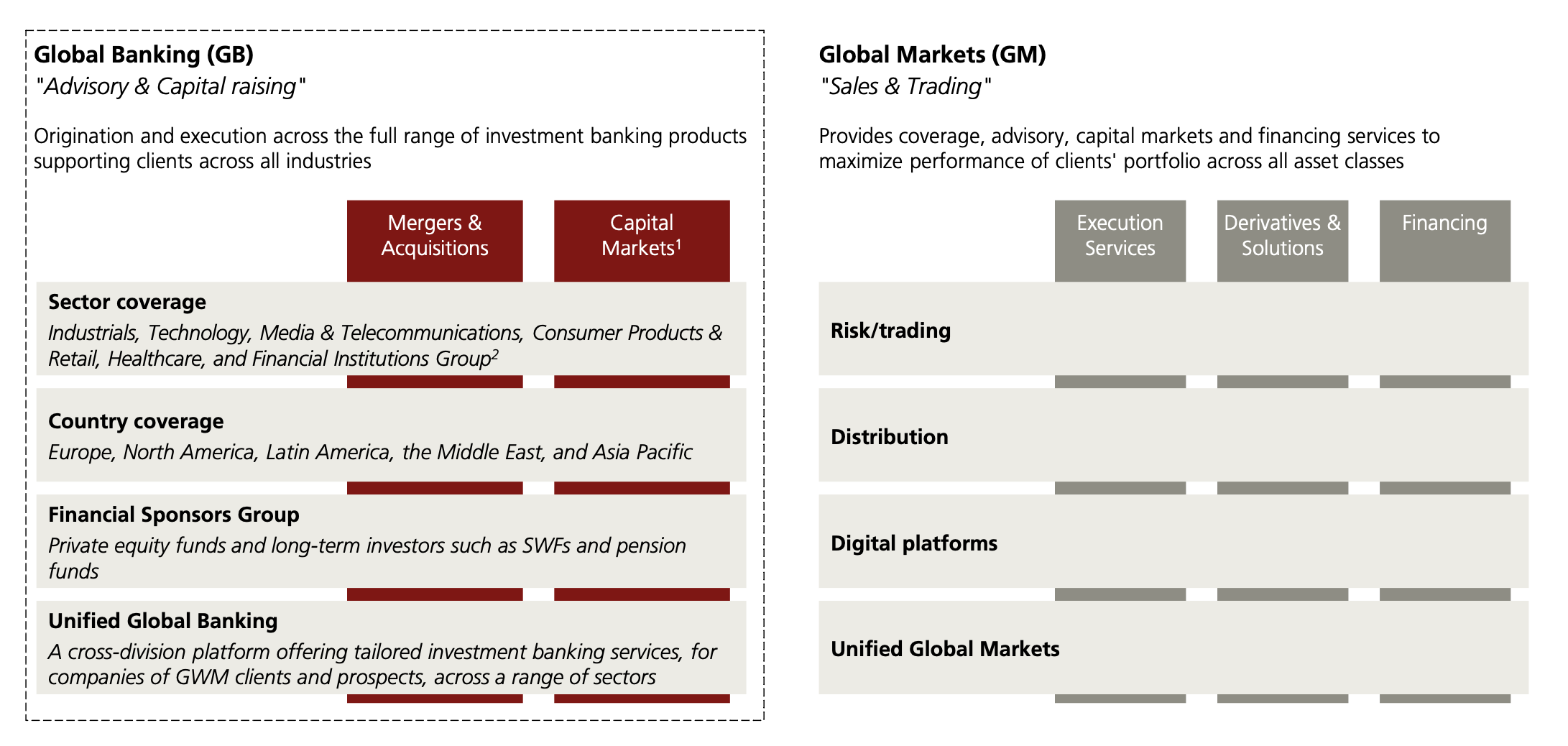

Modern Investment BankingThe investment bank is today split into two main divisions:

- Global Markets (GM): often referred as Sales and Trading, focusing on the execution of trades, risk management and providing liquidity across various asset classes.

- Global Banking (GB): often referred as Advisory and Capital raising, focusing the strategic side of finance, including M&A advisory and helping companies raise money in the capital markets

Some number about UBS:

- 2000+ bankers employed worldwide

- 8000+ clients

- 83 countries with bankers in 40 cities

- strategic operations centered in major financial hubs (New York, London and Hong Kong)

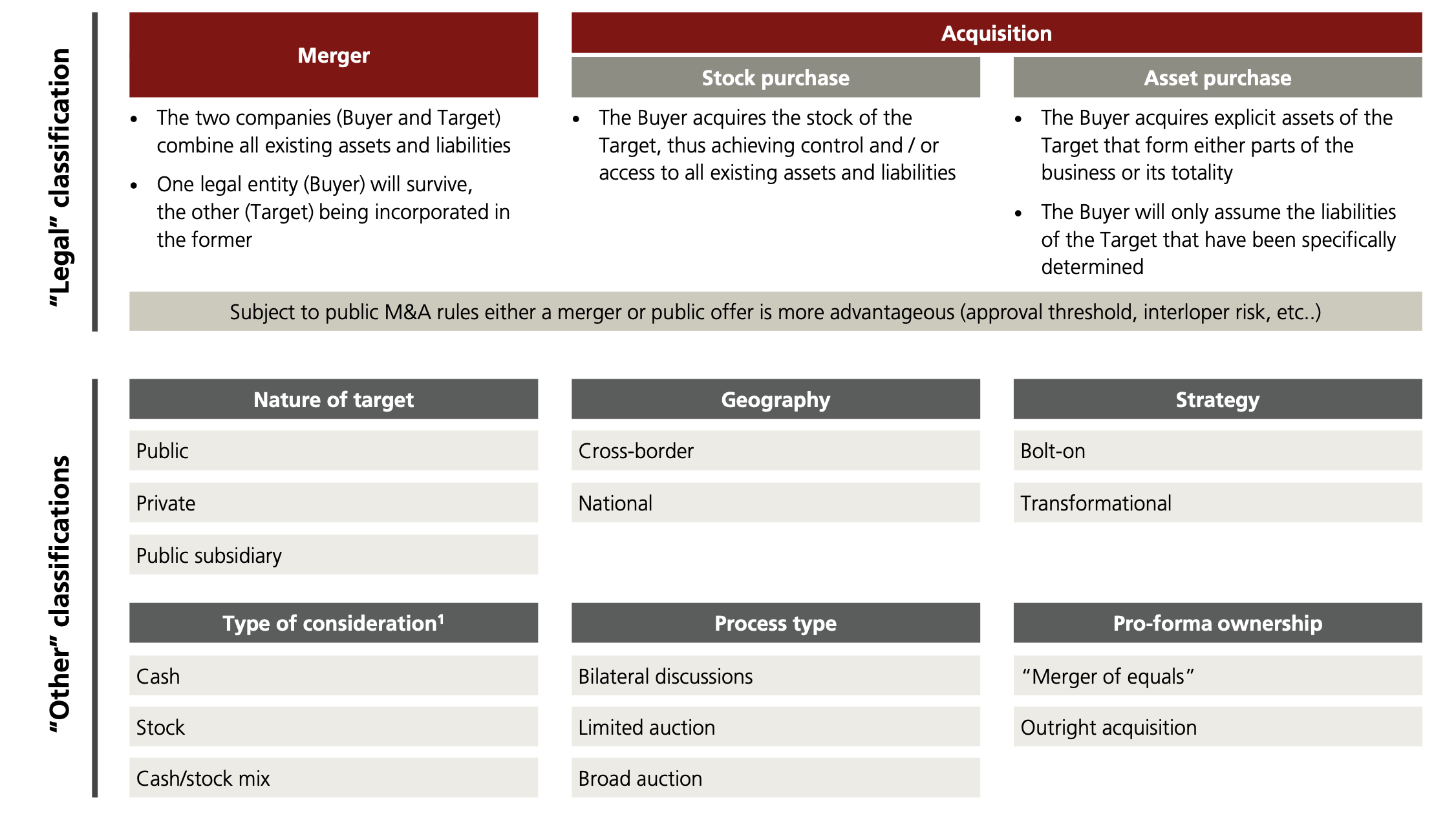

How can business combination be classified?

- Preparation (informal, pre-launch): it involves reviewing strategic rationale for scale, prepare internal financial and equity story, set-up an internal project team and external advisors, identify potential buyers and sign all the confidentiality agreement required

- Phase 1: distribute information memorandum, management presentation, initial valuation framing and buyer positioning first round bid

- Phase 2: full virtual data room access, vendor due diligence, written Q&A, site visits if applicable binding offer, binding financing commitments

- Negotiation and signing: shortlist to 2-3 bidders, review of any black-box information, final price Final SPA (sales and purchase agreement)

How to value a company

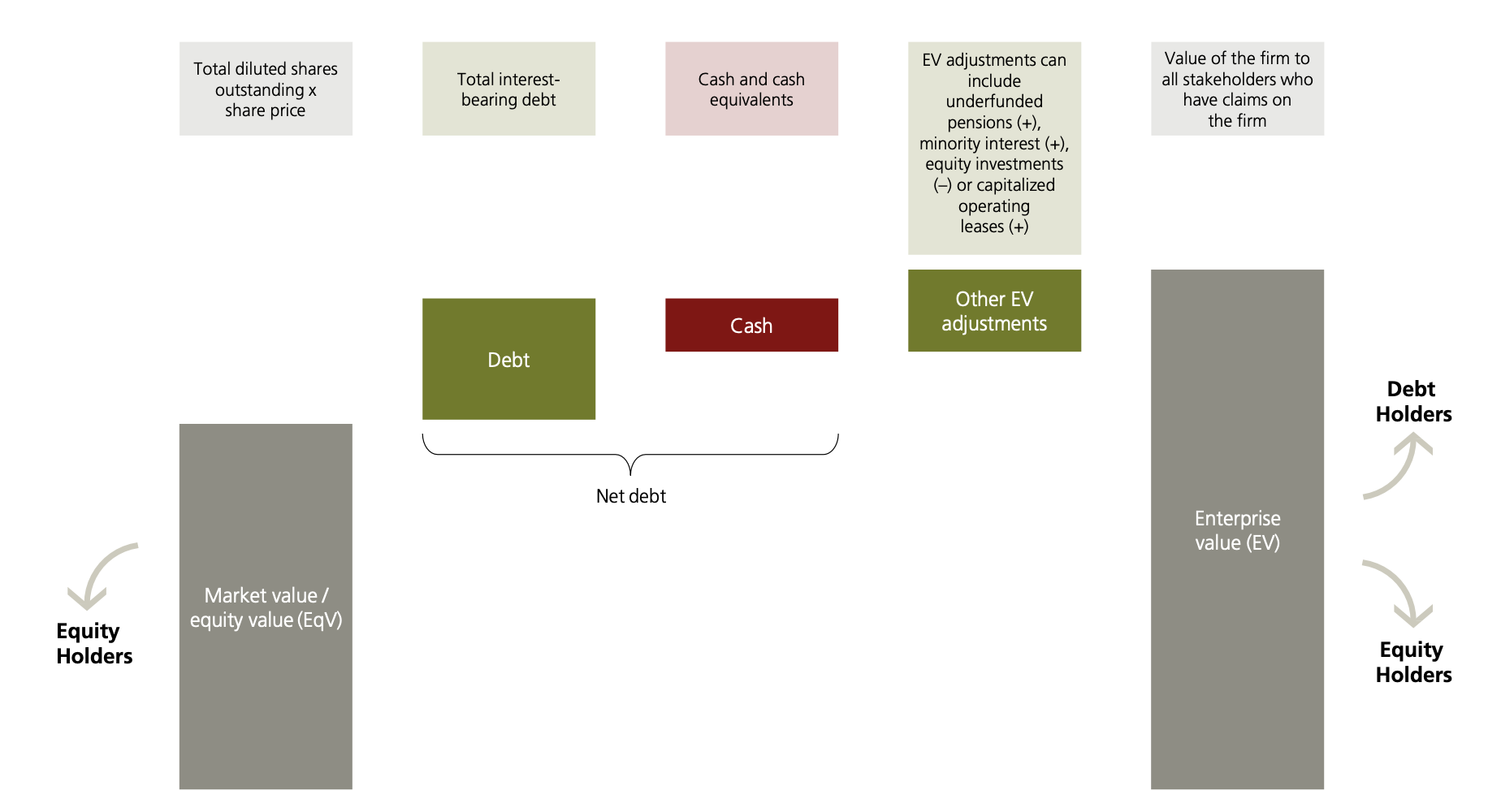

Market value and enterprise value relate returns to different stakeholders or, in other terms:

- Market value: it measures the equity value, excludes debt, cash and other financial obligation, most common in stock valuation

- Enterprise value: it measures a company's total value, including both equity and debt, minus cash. It represents the theoretical cost to acquire the entire company.

| Valuation Methodology | Comparable Companies | Comparable Acquisitions | Discounted Cash Flows (DCF) |

|---|---|---|---|

| Method | Key multiples of operating figures (e.g., Sales, EBITDA, EBIT, Net Income) for comparable traded companies. | Key multiples of operating figures (e.g., EBITDA, EBIT, Net Income) for comparable M&A transactions. | Present value of projected free cash flows using WACC as discount rate; terminal value based on perpetual growth or exit multiple. |

| Rationale | Generates theoretical current market value; provides market-based check for DCF valuation. | Reflects strategic value, including premiums paid for control. | Generates intrinsic enterprise value; allows sensitivity analysis; provides operating figures for other methods. |

| Issues | Limited comparable companies; valuations influenced by market conditions; small-cap stocks may not reflect fundamental value. | Limited comparable transactions; deal-specific factors (e.g., synergies) cause wide valuation ranges. | Requires detailed understanding of business model; prone to optimistic assumptions; highly sensitive to inputs. |

Discounted Cash Flow (DCF) analysis

Major steps:

- Due diligence: analysis of the business and the business environment coming up with assumptions

- Financial modelling: link all the assumptions and the data collected in some actual financial numbers

- Project free cash flows at the end of the period

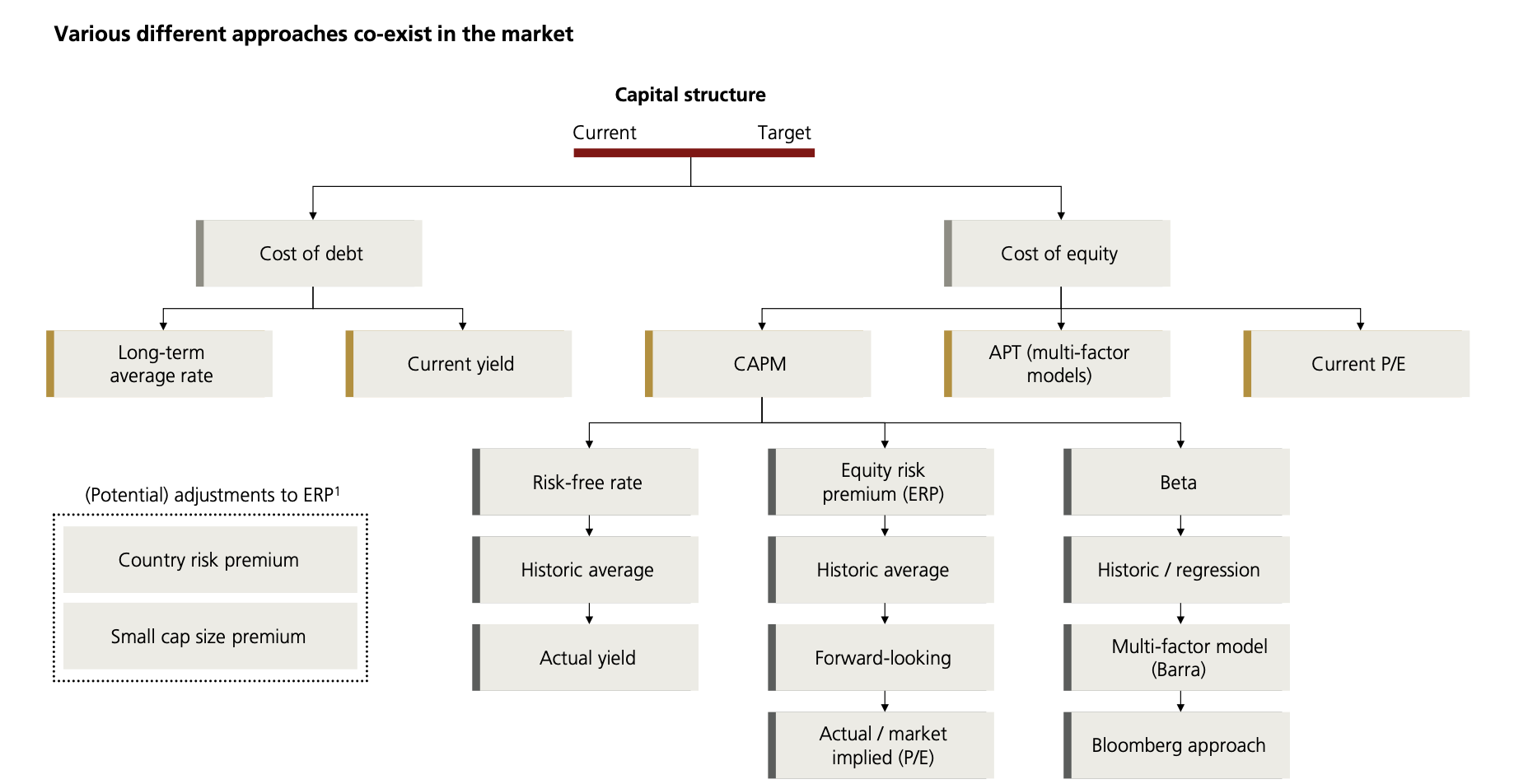

- Estimate the discount rate, usually using the WACC (weighted average cost of capital) as the opportunity cost of FCFs

- Discount and calculate the present value of FCFs and the terminal value (fair value of the assets that generate the FCFs)

- Make adjustments and calculate the Enterprise value by adding or subtracting assets and liabilities omitted in FCFs.

Note that the most critical part is often estimating the discount rate:

| Multiple | Pros | Cons |

|---|---|---|

| EV/EBITDA | Independent of leverage and capital structure. Good ratio in cyclical industries. | Distorted by differences in capex levels. |

| EV/cash flow or EV/(EBITDA – capex) | Accounts for high capital intensity, corrects for different depreciation policies. Ideal for cyclical companies. | Inconsistent definition of cash flow across firms. Requires most information. |

| Price/earnings (P/E) | Widely used by investors and P/E. | Distorted by different accounting habits (particularly depreciation). Sensitive in cyclical companies. Can be distorted by leverage. |

| EV/EBIT | Independent of leverage and capital structure. Well-understood metric. | Distorted by different depreciation/accounting policies. EV/EBITDA is usually preferable. |

| Equity FCF yield | Cash-based and forward-looking. Comparable across capital structures and business models. | Sensitive to forecasts and assumptions. Can misrepresent cyclicality as cashflow generation. |

| Price/book value | Used primarily for financial institutions. Reflects long-term profitability. | Distorted by accounting differences. Need profitability check. |

| EV/sales | Used primarily for high-growth/tech companies not yet in a EBITDA-positive stage. | Highly dependent on profitability. Requires similar path to profitability. |

| Growth-adjusted multiples | Typically used in the valuation of early-stage businesses. | Relies on the assumption that growth is the key value driver. |

12. Corporate Restructuring

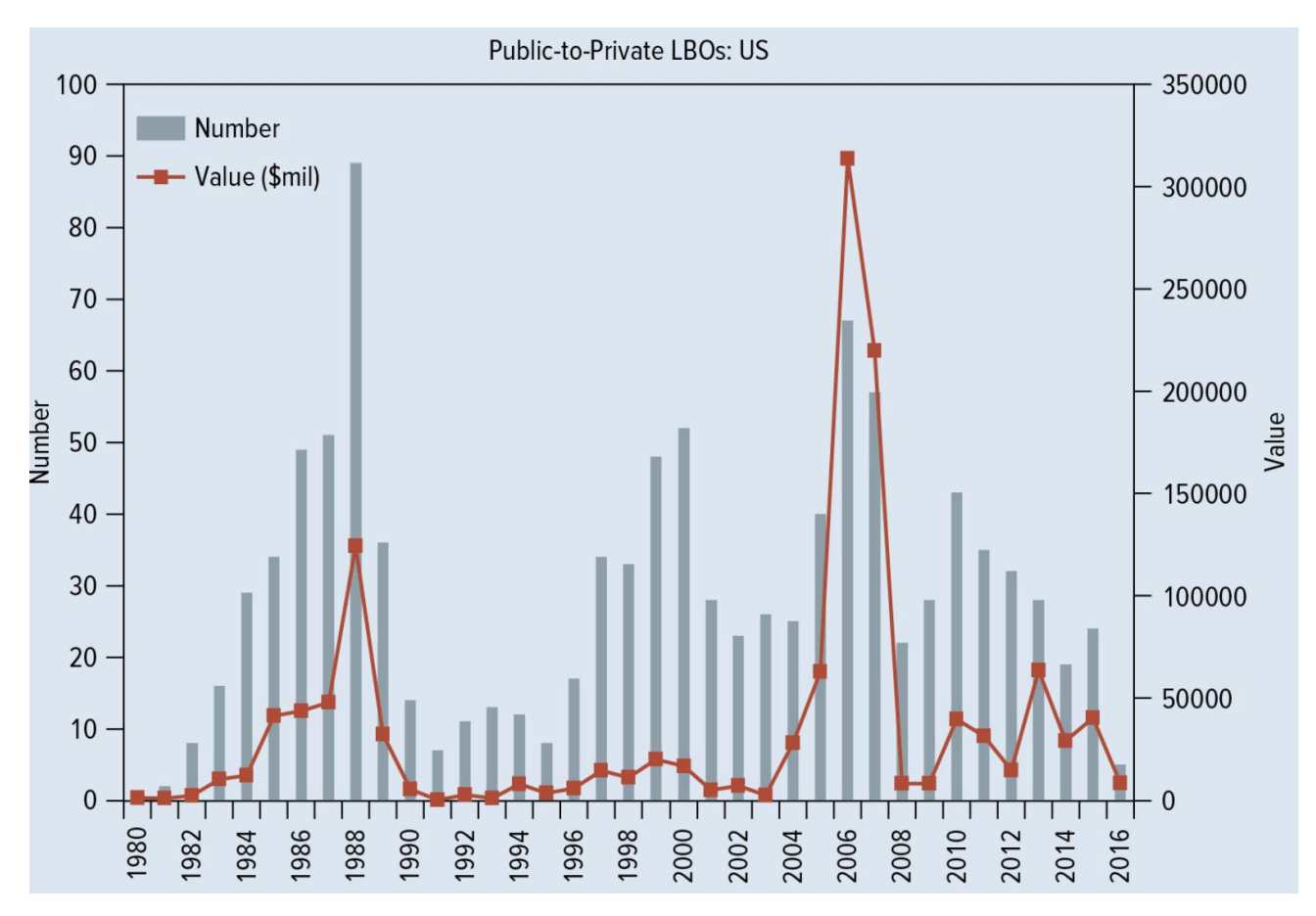

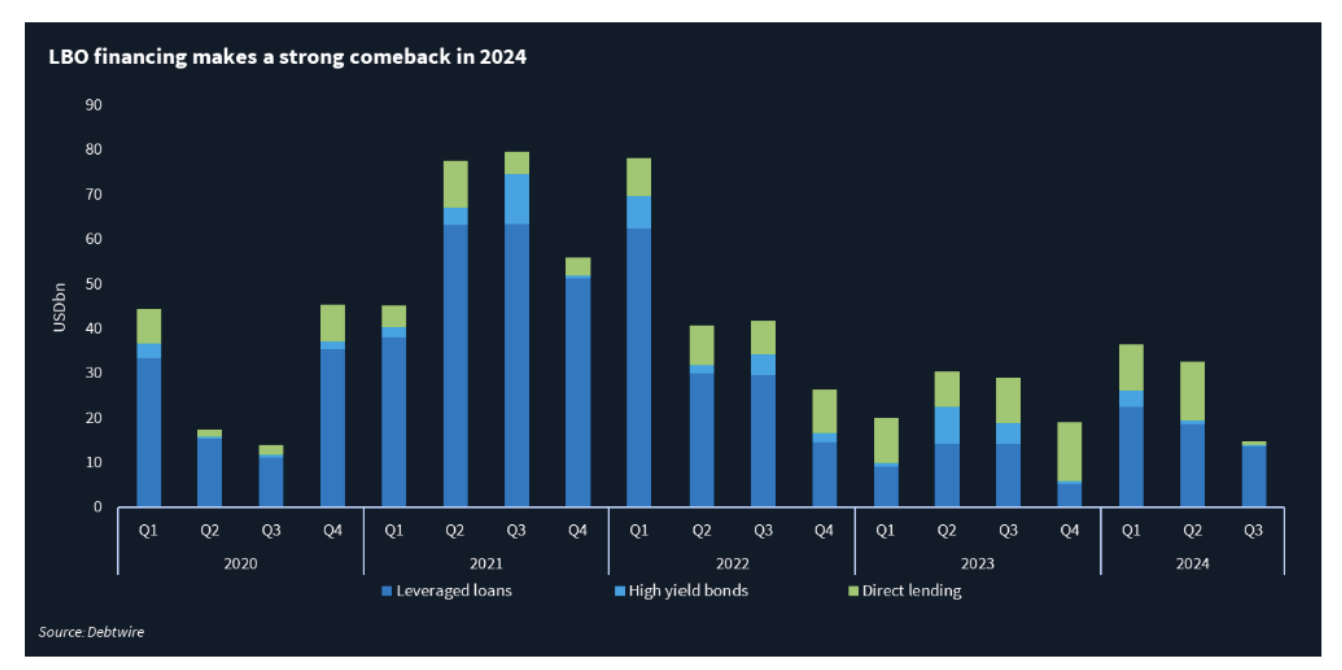

Leverage BuyoutLeverage buyouts (LBO) are characterized by the fact that large portion of the buyout is financed by debt shares of the LBO no longer trade on the open market.

Consider also the special case: a management buyout is a buyout led by the existing managers.

Consider also that leveraged loans volumes have rebounded in 2024, mirroring the increase in LBo activity.

In Europe, leveraged finance is increasing in 2025: interest rate cuts in 2024 created a more favorable condition for the syndicated loan high yield bond markets, while the competition between public and private lenders is reshaping the financing industry.

Leverage RestructuringThe difference between LBO and ordinary acquisitions lies in the following:

- a large fraction of the purchase is debt financed, usually with junk bonds

- the LBO goes private

- sometimes, after the terminal period of the LBO, a spin-off or a carve-out (like a spin-off, but the new business is sold in a public offering) can happen.

we can summarize then the 4 main characteristics of LBOs:

- high debt

- incentives

- private ownership

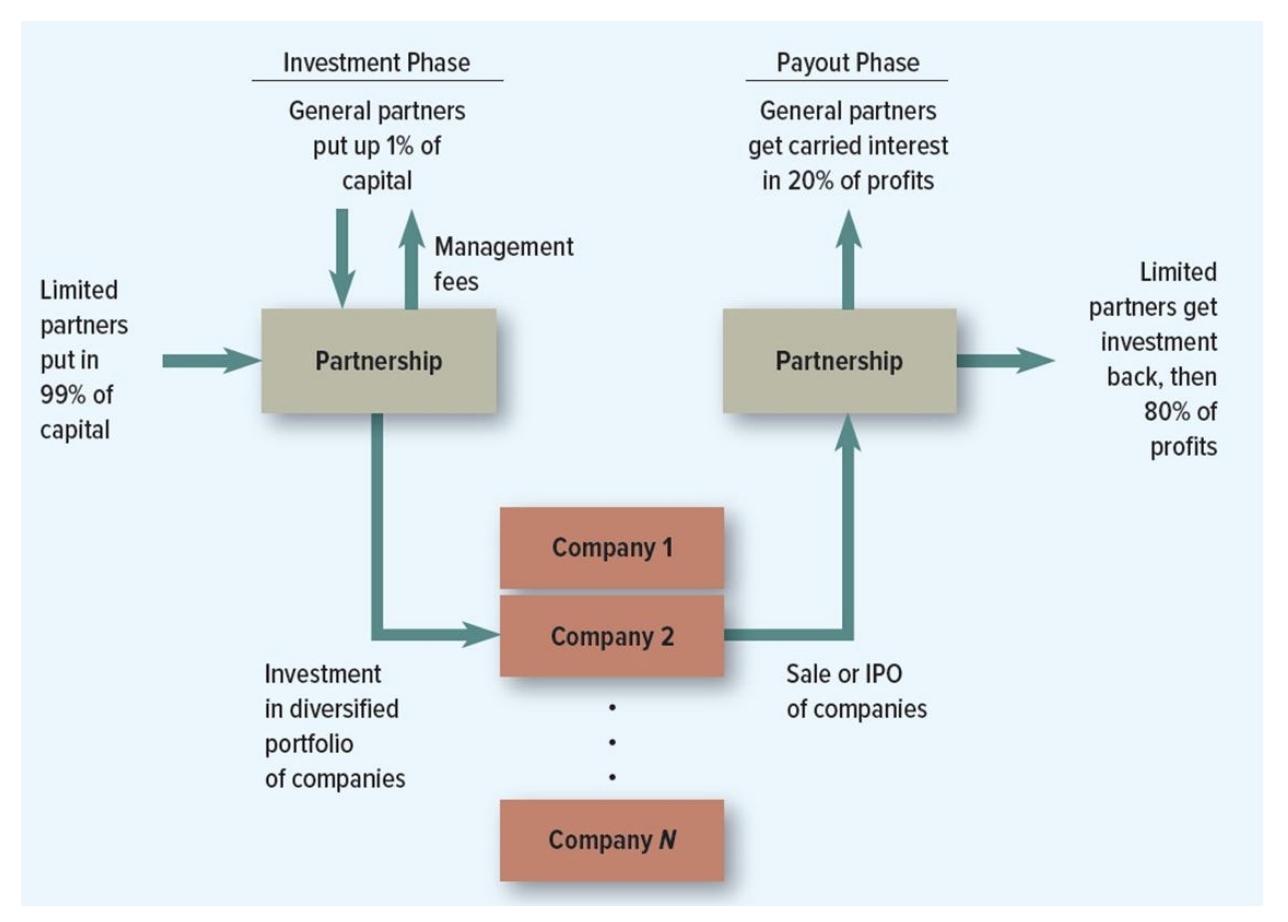

Overview of Private Equity

Even if PE funds can be similar to public conglomerate, they show some differences:

| Private–Equity Fund | Public Conglomerate |

|---|---|

| Widely diversified, investment in unrelated industries | Widely diversified, investment in unrelated industries |

| Limited-life partnership forces sale of portfolio companies | Public corporations designed to operate divisions for the long run |

| No financial links or transfers between portfolio companies | Internal capital market |

| General partners "do the deal," then monitor; lenders also monitor | Hierarchy of corporate staff evaluates divisions’ plans and performance |

| Managers’ compensation depends on exit value of company | Divisional managers’ compensation depends mostly on earnings |

13. Financial Crises and Regulatory

Why regulate the banks?Banks play a special role in the economy (combination of payments, lending, deposit taking etc...), so the impact of banking crises can be huge and lead to permanent GDP losses. For this reason, there's a lot of support from the public sector to promote financial stability (deposit insurance, lender of last resort).

The primary metric is of course capital.

We define the common equity (net assets) of any company as the difference between its assets and liabilities. Common equity can be understood as the shareholders's residual claim on the assets the company, after taking account of the claims of other funders.

With positive common equity, depositors and other funders can be comfortable that assets are sufficient to cover their claims and "will be happy" to continue funding the bank.

Common equity is also considered the first form of funding to bear a loss, as it does it instantaneously.

Subordinated debt (subordinated loan, subordinated bond, or junior debt) is a type of debt that ranks below other debts in terms of claims on a company's assets.

In the event of a liquidation or bankruptcy, subordinated debt holders are paid only after the senior debt holders have been fully repaid.

Hybrid capital is a form of subordinate debt that shares some features of common share:

- it is usually perpetual (no maturity date)

- it enables the bank to cancel interest payments (similar to cancelling dividend payments on common shares)

Liquidity (funding liquidity) can be defined as having cash when you need it to meet repayments or to provide business to clients:

- can be generated from the asset side of the balance sheet by selling assets

- can be generated from the liability side by raising funds through additional borrowing (it does not change the size of the balance sheet)

An asset is considered liquid if it can be rapidly converted into cash with no loss of value it means typically that there's a deep and active market where the asset can be traded.

Regulatory metrics: Capital

There are two key metrics for capital:

The leverage ratio exposure is a measure of the bank size (= total assets + off-balance sheet items converted into on-balance sheet equivalents) but it doesn't discriminate between the riskiness of assets.

Risk-weighted assets (RWA) are the nominal exposure converted into risk-weighted exposure using standardised risk-weights set by regulations or banks' internal models.

Optimal Capital Requirements| Study | LEI (2010) | Miles et al (2013) | Yan et al (2012) | Martinez-Miera and Suarez (2014) | Nguyen (2014) | Mendicino et al (2015) |

|---|---|---|---|---|---|---|

| Definition of capital | Tier 1 | Tier 1 | CET1 | Tier 1 | Tier 1 | Total capital ratio |

| Optimal capital requirement (% of RWAs) | 13 | 16–20 | 10 | 14 | 8 | 12–16 |

Regulatory metrics: Liquidity

There are two metrics for liquidity:

- Liquidity Coverage Ratio (LCR):

- Net Stable Funding Requirement (NSFR):

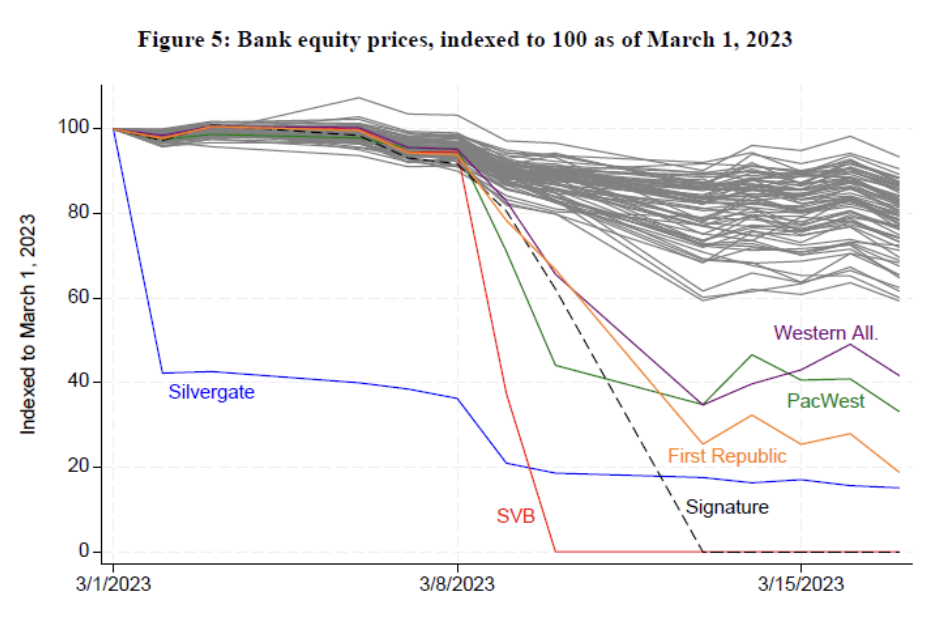

The 2023 Banking Turmoil: a recap

It was the most significant system-wide banking stress since the Great Financial Crisis 5 banks with total assets of trillion failed, merged or liquidated.

In general, it was a broader crisis of confidence that needed extensive public support measures.

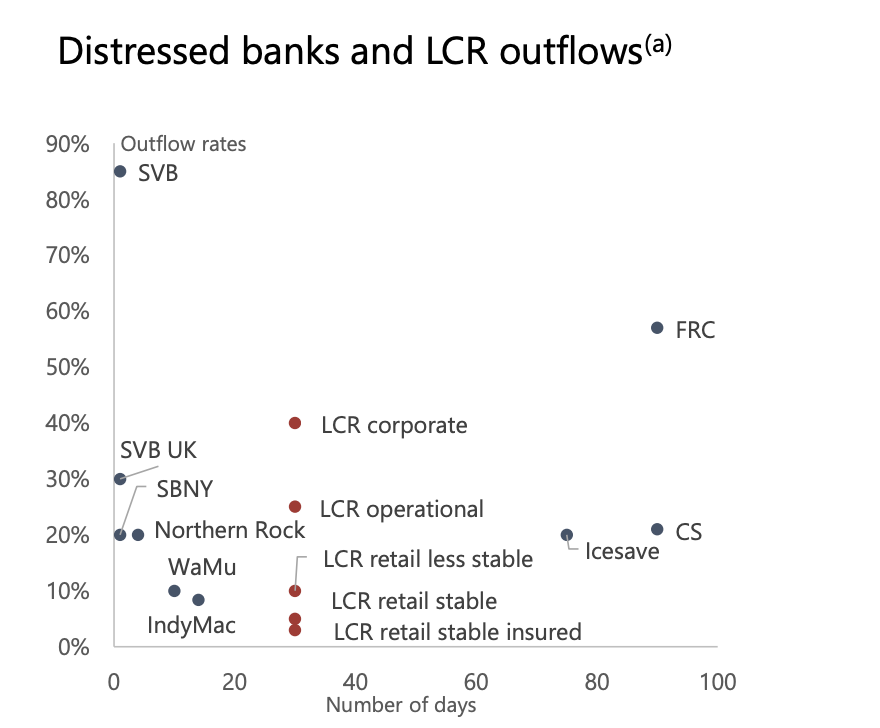

The following plot shows the LR outflows from distressed banks

Some takeaways from this crisis:

- outflows of some deposits were larger and faster than assumed in the LCR and NSFR

- additional liquidity needs not covered by the LCR can be material

Debt Restructuring

Financial distress is one of the most misunderstood concepts in corporate finance since the instinct it to treat a distressed firm as a failing business.

The first and most important analysis in any restructuring situation is to distinguish between two fundamentally different conditions:

- economic distress: occurs when a firm's business model is broken and the firm cannot generate enough cash from operations to cover its cost, regardless of how its balance sheet is structured.

- financial distress: occurs when a good business is burdened by a inefficient capital structure, often cashflows are positive or recoverable, but the firm cannot meet its debt obligations.

| Dimension | Economic Distress | Financial Distress |

|---|---|---|

| Root cause | Business model, competition, technology | Excessive leverage, liquidity shock, covenant breach |

| Operating cash flow | Insufficient or negative | Positive or recoverable |

| Going-concern value | Below liquidation value | Above liquidation value |

| Appropriate response | Liquidation or radical operational restructuring | Financial restructuring (debt renegotiation) |

| Role of new money | Unlikely to help | Essential to regain stability |

The second crucial distinction is between:

- illiquid firm if the firm cannot meet short-term obligations even if the long-run assets are correctly valued and exceed liabilities.

- insolvent firm: if the economic value of its assets is below the face value of its liabilities

Costs of financial distress and Optimal leverage

Costs of distress can be separated in direct costs (lawyers, restructuring advisors, investment bankers, accountants etc...) and indirect costs (customer defection, suppliers, employee leave, management distraction, loss of competitive competition)

This brings the fundamental economic rationale for why firms do not borrow as much as possible. The trade-off theory of capital structure indeed says:

The Merton model of a firm

The Merton model establishes that:

- equity is a call option on a firm assets:

- if the firm ha asset value and debt face value , then:

- equity gets (equity has the same pauyoff of a call option on the assets with strike price if assets are worth more, shareholders keep the upside, otherwise they walk away and lose only their equity)

- risky-debt embeds a short put (the bondholder is not holding a clean risk-free, becuase oin case of default they don't receive the promided ):

- debt gets

The Agency Problems in distress: 3 conflicts

- Risk Shifting (asset substitution): when a firm is near insolvency, shareholders hold a deep OTM call since the equity has minimal intrinsic value. In this case, may prefer a negative-NPM risky projects over positive-NPM safe projects, because the option structure give them upside of the risky bet (while creditors bear the downside)

- Debt Overhang and underinvestment: a firm burdene with excessive debt may reject positive-NPM investments because the gains accrue primarily to creditors thatn shareholders. When a firm is insolvent, any new investment essentially services the existing debt first if shareholders must contribute to the investment capital but creditors get most of the returns, shareholders will refuse, even when the investment has positive NPV and would benefit everyone in aggregate.

- Reluctance to recapitalise (debt dilution): when a distressed firm needs new equity to survive existing shareholders are reluctant to contribute because new equity injection primarily benefits exiting creditors rather than new equity providers New equity providers are implicitly subsidising old creditors. They will only contribute if existing debt is written down first.

Valuation in distress and the Fulcrum Security

The central valuation question in any restructuring is: "is the firm worth more alive or dead?"

To understand this, we firstly define:

- going-convern value (GCV): the present value of the firm's future cash flows on operating business assuming a successful restructuring.

- liquidation value (LV): the net proceeds from selling assets immediately, typically at a forced-sale discount.

Generally speaking, if : restructure.

The excess () is the restructuring premium.

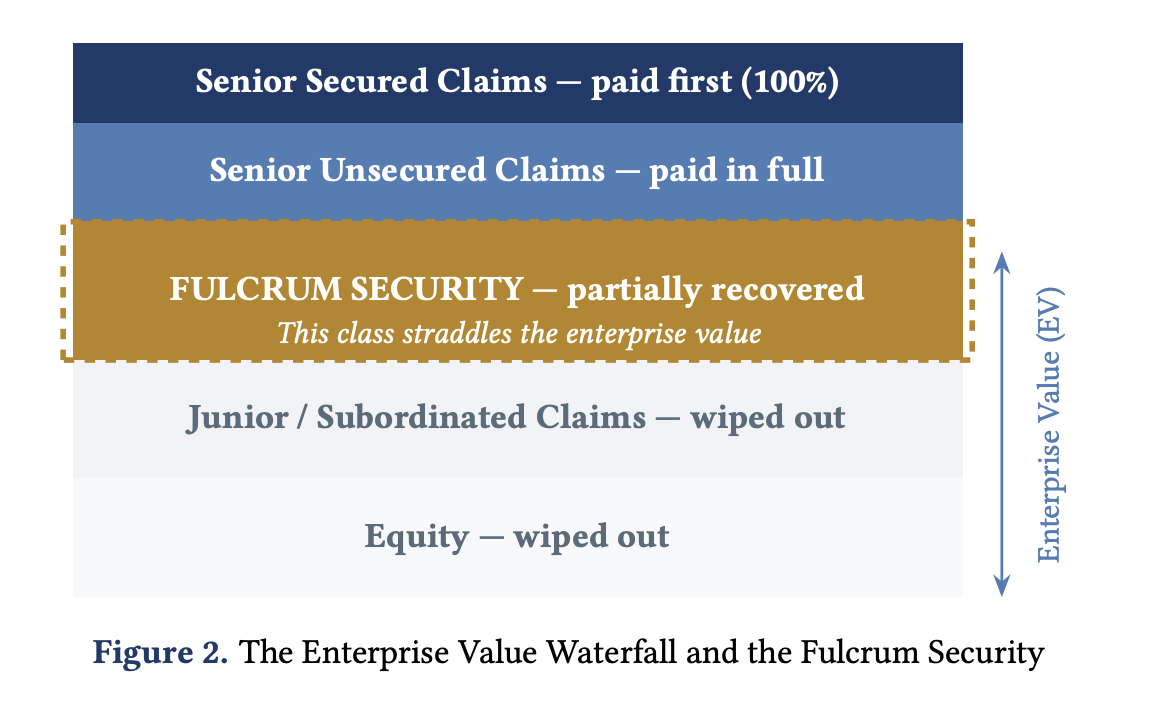

Once the going-concern enterprise value (EV) is estimated, it is distributed to claimants according to the priority waterfall:

The fulcrum security is then identified as the class of debt (or, rarely, equity) that is only partially recovered in the restructuring. It is the pivot point of the enterprise value waterfall: all senior claims are paid in full, all junior claims receive nothing, the fulcrum class is partially recovered.

- the fulcrum holders are the only class whose vote genuinely matters

- the fulcrum holders typically receive equity in the restructured firm.

- all negotiation effectively converges on what the fulcrum class receives and on what terms.

Restructuring instruments: Debt-for-equity Swaps

A debt-for-equity swap is an exchange in which creditors give up their debt claims in return for an equity stake in the restructured firm the creditors's role shifts from fixed-income to residua-claim ownner.

Let denote the debt characteristics (principal, coupon maturity). The share price before restructuring is . Creditors hold debt with bankruptcy value .

If the offer is rejected:

- Credit holders get:

- Equity holders get

If the offer is accdepted:

- Credit holders get:

- Equity holders get

Creditors accept the swap if and only if:

where is the equity fraction should compensate the creditors for the forward value of lost cashflows.

Restructuring instruments: Warrants

Warrants serve as sweetener: creditors accept worse debt terms in exchange of warrants that provie conditional upside exposure if the restructured firm recover. Warrants are particularly useful when:

- the firm is in moderate distress

- creditors believe in the upside story but are reluctant to become equity holders immediately

- management wants to keep control of the company while still compensating creditors for accepting reduced claims

- the tax shield on remaining debt is valuable and should be preserved.

To design a warrant, we consider the following parameters::

- strike price, set above the current distressed price

- : number of warrants (More warrants means more potential upside transferred to creditors, but also more dilution for existing shareholders if exercised)

- Coverage ratio: warrants issued per unit of face value surrendered in the haircut (it links concession to compensation: bigger haircut usually requires higher coverage)

- expiration

- Exercise style: usually European (only at expiration) to simplify administration

A warrant is then modelled as a call on news shares, so the dilution effect must be incorporated, we consider:

- current share price

- strike

- expiry date

- equity volatility

- £r$ risk-free rate

- existing shares outstanding

- warrants to be issued

The diluition factor is:

and the diluition-adjusted warrant price is:

where is the standard Black-Scholes call price formula.

Restructuring instruments: HaircutsA haircut is a restructuring tool in which creditors accept a reduction in the face value, coupon, or present value of their claims to restore debt sustainability. It is typically negotiated when the going-concern value is above liquidation value: creditors take an immediate loss, but improve expected recovery by keeping the firm.

In simple terms, if original claim is , the new claim is and the haircut is:

Restructuring instruments: PIK NotesPIK notes (Payment-in-Kind notes) allow a distressed firm to preserve near-term cash by paying interest with additional debt securities instead of cash coupons.

They can stabilize liquidity during a turnaround, but they also compound leverage over time, so they are usually negotiated with higher pricing and used only when there is a credible path to future deleveraging or refinancing.

Comparison of restructuring instruments

| Feature | Haircut | Debt-for-Equity Swap | Warrants (sweetener) | PIK Notes |

|---|---|---|---|---|

| Leverage impact | Reduced | Strongly reduced | Unchanged | Increased |

| Creditor claim | Reduced debt | Equity | Option on equity | Accruing debt |

| Upside for creditor | None | Full (as equity) | Conditional | None |

| Tax shield | Reduced | Lost | Maintained | Maintained |

| Existing equity dilution | None | Significant | Moderate (on exercise) | None |

| Complexity | Low | High | Medium | Low |

| Debt overhang resolved | Partially | Fully | No | No |

| Typical use case | Any distress | Deep insolvency | Mild distress / sweetener | Cash preservation |